Daily Briefing 3/28/25

Personal Income/Spending (BEA)

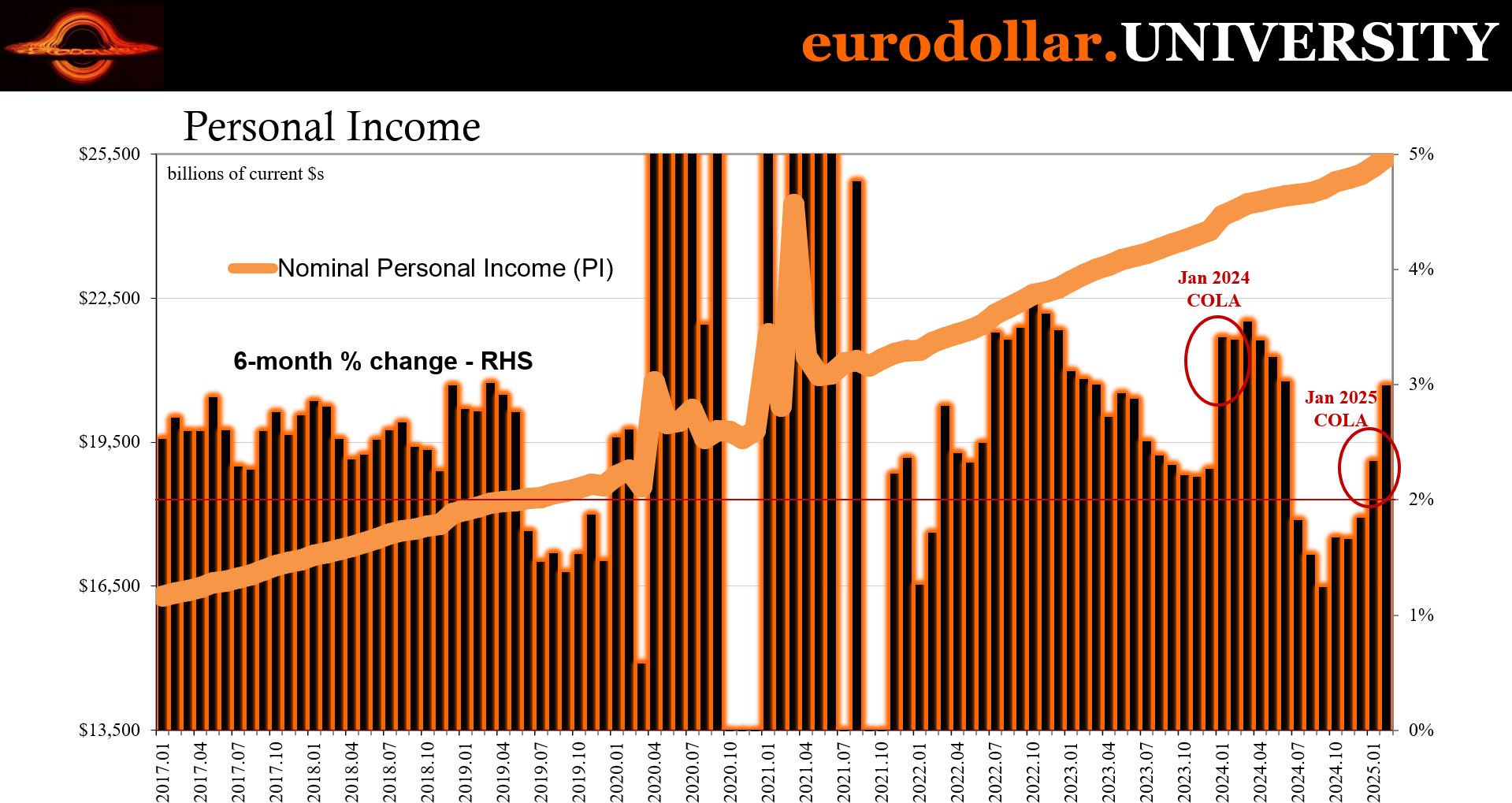

Personal income rose by $194.7 billion (0.8%) in February, with disposable personal income (DPI) up $191.6 billion (0.9%). Personal consumption expenditures (PCE) increased by $87.8 billion (0.4%). Personal outlays rose by $118.4 billion, while the personal saving rate stood at 4.6%. The increase in income was primarily driven by higher personal current transfer receipts and compensation. Government social benefits contributed through premium tax credits for health insurance, while business payments to individuals - stemming from legal settlements - also played a role. Compensation gains were led by private-sector wages, with services-producing industries adding $35.7 billion and goods-producing industries $12.7 billion.

Interpretation

At first glance, February’s income growth appears solid, marking the second consecutive monthly increase. However, a closer look at the details suggests that the rise was largely due to one-off factors rather than broad labor market strength. The biggest contributors were government social benefits, particularly health insurance premium tax credits, and business payments linked to settlements. These temporary boosts distort the underlying trend, making it unlikely that income growth at this pace will persist in the coming months.

Wage gains did contribute to the increase, but the numbers are not extraordinary. Private-sector wages rose in both services and goods-producing industries, but there’s little indication that earnings surged beyond what’s been typical in recent months. This further reinforces the idea that February’s income growth was not a signal of sustained labor market strength but rather a statistical blip due to transfers, consistent with other employment sources showing distress rather than income strength.

Incomes in real terms were nearly flat, particularly excluding those transfers. Real Personal Income excluding Transfer Receipts was up just 0.11% in February and only increased 0.2% in the three months since November. That better explains the pullback in consumer spending, aligned with souring confidence and growing concerns of future labor conditions.

On the spending side, consumer demand remained weak. While PCE increased in February, it only partially offset January’s downward revision. Taken together, the January-February period suggests that consumer spending is losing momentum – if not lost already - reinforcing signs of a broader pullback in demand. This aligns with recent data pointing to weaker retail activity and softening economic sentiment.

Supporting this argument is the personal savings rate, which rose to 4.6%, reflecting a combination of higher incomes and lower spending. This suggests that consumers are being cautious and saving more due to economic uncertainties. However, the overall savings rate is still relatively low compared to historical averages, showing that consumers are continuing to adjust to changing economic conditions.

In sum, income gains in February were inflated by one-off factors, while consumer spending remains soft. The data suggests that underlying economic strength is weaker than headline numbers imply, reinforcing concerns about the sustainability of demand and the broader trajectory of the economy.