ANOTHER MEASURE OF ALTITUDE

EDU DDA Mar. 24, 2025

Summary: GDPNow abruptly turned deeply negative at the end of last month. It was blamed on Swiss gold. While that part explains the depth of the negative, it doesn’t account for the full loss of GDP altitude. If anything, that loss is showing up in a wide variety of recession calls (rising probabilities) and downgraded growth expectations. Those downgrades seem relatively tame, from historical perspective if they hold true we will have experienced a full, traditional recession. There is no ambiguity in the data. Instead, this the GDP version of the Beveridge Curve - stall speed.

WE MAY NOT HAVE A HARD-SCIENCE WAY OF DEPENDABLY MEASURING AN ECONOMY’S ALTITUDE, BUT WE DO HAVE A COUPLE OF USEFUL METHODS.

The Atlanta Fed’s more infamous GDPNow tracker created a shock a month ago when the Census Bureau’s import estimates caused the model to collapse its Q1 estimate. It had been humming along at a decent pace following Q4’s slightly weaker-than-hoped 2.3% with what was shaping up at the time to be a repeat.

While most have accepted that kind of growth rate, or anything close to it, as “solid”, that’s missing the overall context. There is more than a semantical argument over “forgot how to grow” and it is indeed playing a role in the weakness which is now being more widely cited – if attributed to tariff policies.

That’s the thing: from most peoples’ perspectives, the economy was just fine yesterday, booming even, and now seemingly all of a sudden R-word almost everywhere. What changed? Trade wars appear to be the answer.

Understanding, instead, the economic struggles go much farther back well into the “vibecession” and before, the risks have only been rising this entire time. The forgot-how-to-grow risked forgetting a good bit more the longer the amnesia was maintained. At 2.3% in Q4, that really wasn’t a good sign particularly given how much of that was supported by the tariff effect which had pulled forward demand at the expense of early this year.

Any GDP growth rate below 4.5%, at minimum, is an economy being left behind. Payrolls should be rising at 450,000 not 150,000, generating a significant and sustained surge in hours. We don’t have anything close to that anywhere. The trouble didn’t show up in the middle of last month.

What did was most peoples’ awareness.

America’s economy may not even have 2.3% going for it, either. By February 28, the GDPNow model was forced from +2.3% to -1.5% in a single update by the massive jump in the value of imports, particularly bullion. Gold dealers all over America were pulling in huge quantities fearing imported gold would be hit with large tariffs, too. Obviously, there isn’t enough physical metal domestically to satisfy all buying scenarios (not that we didn’t know this; the gold market, like any other, has a supply chain which makes it more efficient rather than everyone everywhere hanging on to their own sizable physical reserve and this episode is a solid demonstration of what happens when that chain is potentially disrupted).

A few days later, the Q1 nowcast slipped even more, all the way to -2.8% after digesting the monthly personal income and spending estimates provided by the BEA, the GDP agency. Spending was way down in January (blamed on cold weather, of course) and aligned with retail sales. It was enough to force GDPNow’s forecast for PCE (personal consumption expenditures) down from +0.87 pts (contribution to topline GDP growth) to essentially zero (+0.01 pts).

Other data reports at the same time trimmed forecasts for residential and non-residential investments, together with personal spending accounting for the second big decline in a week.

The shocking developments made headlines around the financial media, as strong and resilient took a backseat to the growing sense of this loss of momentum. It had been apparent in sentiment data, only here was some hard-ish data estimates to give that loss more clarity (rather than uncertainty). GDPNow is hardly definitive about anything, including the next GDP estimate from the BEA, still the bigtime drop was difficult to ignore especially since many had been touting its early 2025 “resilience.”

As if to prove that one point about its reliability, Economists with the Atlanta Fed hastily put together and issued a statement which said the models were, indeed, getting something big wrong. The BEA doesn’t consider imports of non-monetary gold to be of economic value therefore doesn’t include them in its actual GDP calculations. Since the Georgia researchers figure there was around $20 billion in gold in the trade data, this was a major discrepancy.

The upshot of their work was to say the “real” GDPNow forecast, as of March 18, should have been +0.4% not -2.8% or -1.5%, the latter having been the last update to the model prior to the FOMC meeting blackout. The “fixed” calculation taking account of gold will be released on Wednesday.

Lost in the distraction over airplane-loads of the lustrous yellow metal, had it never happened we’d still be left with a nowcast of +0.4%. That only looks better by comparison to the import-inflicted -2.8% which showed up first. In other words, had there not been Swiss gold shipped here in such massive quantities, the reaction to GDP going from +2.3% at the end of February just to +0.4% by mid-March likely would have struck the world more than it did.

Human nature and public perception being what they are (the same as why companies guide their earnings lower and then beat them by a penny or two).

Take away the gold, as it currently stands even the Atlanta Fed is saying the economy has lost maybe too much altitude. And this is just Q1.

If it was only GDPNow, I certainty wouldn’t be bringing this up here. Nowcast models are notoriously unreliable even for what they purport to do. Rather, what’s noteworthy is how those picking up this loss of momentum only begin with the Fed’s Atlanta branch.

Like data, analysis begins with a broad survey of surveys and opinions (in many respects, the nowcast falls under the latter category). They have been changing and rolling in with breathtaking speed, becoming a consistent drumbeat of growing concerns over, first, momentum, and then the possible second and third order effects which might following from it.

Only last Thursday, DoubleLine’s “bond king” Jeff Gundlach told CNBC, “I believe that investors should have already upgraded their portfolios … I think that we’re going to have another bout of risk.” He then added, “I do think the chance of recession is higher than most people believe. I actually think it’s higher than 50% coming in the next few quarters.”

Doubling up on DoubleLine’s forecast, Deutsche Bank released the results of its market survey. According to them, taken from a panel of 400 participants, the purported chances of a recession over the next year have risen to 43%. Meanwhile, Morgan Stanley cut its own GDP forecast to 0.7%, and that’s for all of 2025 not just Q1.

They, of course, then added this only counts as “modest slowing.”

And that, of course, is not true.

Annual growth rates that are less than a threshold as high as 1.5% are into recession territory. I made this point last week when the FOMC’s SEP was trimmed to a “central tendency” range of 1.5% to 1.9%. That bottom limit is right there even if it might not sound or seem that way, and it sure isn’t how the estimates will be characterized.

Officials would say 1.5%, or thereabouts, is nothing more than a slowdown especially if Morgan Stanely can get away with classifying +0.7% the same way.

The evidence, however, leaves no room for that interpretation. In nearly 80 years of GDP figures, the numbers are beyond doubt.

For our purposes here, I’m using the Q4/Q4 method of computing annual rates (taking the final real GDP tally for any year and comparing it to the final GDP tally from the year prior). We could also use the average GDP method, where you average the four quarterly annual rates and compare it to the average of the previous year’s four rates, but the Q4 method is a superior and more widely accepted comparison, though there aren’t really too many differences.

Starting with the 21st century, there have been only five years out of the twenty-five (counting Year 2000) thus far when annual output growth rates (real GDP) have been below 1.5%. Of those, four are outright traditional recessions: 2000, 2008, 2009, and 2020. The fifth, 2022, did have a “technical recession” in its first half (which has been revised since to a contraction in Q1 ’22 followed by a very small positive in Q2), and also, most importantly, kicked off the “forgot how to grow” pattern.

It was also the highest of those annual comparisons, coming in at 1.3% therefore closest to the threshold.

Part of the matter when interpreting full-year estimates is that small positives do sound like nothing worse than a slowdown. As with Morgan Stanley’s forecast for +0.7% in 2025, while it may not come off as great or even good, that level isn’t immediately threatening, either. We think of negative numbers, deeply negative, as consistent with recession not mildly positive.

Take 2009, for example, when the contraction ravaging throughout the first half of that year was the biggest one since the Great Depression. The effects on the labor market were astonishing, permanently disruptive. Millions upon millions of jobs lost, with layoffs continuing right on through into 2010.

Given the severity and persistence of the economic disaster, you’d think full-year GDP (Q4 to Q4) must’ve been sharply negative. How could it not be?

But it isn’t. According to the BEA’s estimates, real GDP in calendar year 2009 was the smallest positive at +0.1%.

Eight years earlier, 2001’s dot-com recession was clearly – and “officially” – a recession but GDP for the year was also positive at +0.2%.

Going back into the 1950s, we find the exact same all throughout GDP history. The S&L recession which began in 1990 only brought the full-year estimate down to +0.6%. The following year, 1991, part recession and part jobless recovery, still managed +1.2%. The late fifties double-dip, which began in 1957, both years when the contractions were at their worst still put up positive full-year GDP growth rates: +0.4% in 1957 and +0.9% in 1960.

Morgan Stanley’s 2025 number is easily within range of each of those up to and including 2001’s dot-com contraction.

As for the Federal Reserve’s +1.5%, of the 77 years in data going back to 1947 (yearly change starting with 1948), there have only been two occasions when CY real GDP growth was less than 1.5% and there was no official NBER-declared business cycle within that year. One of those was 2022, as noted above, the other was 1979 (+1.3%) which missed by a single month (the start date was January 1980).

In every other instance when full-year GDP has been less than 1.5%, there has been a called cycle peak. If we exclude 1979 and 2022, then the threshold need only be below +1.3% to be recession-like.

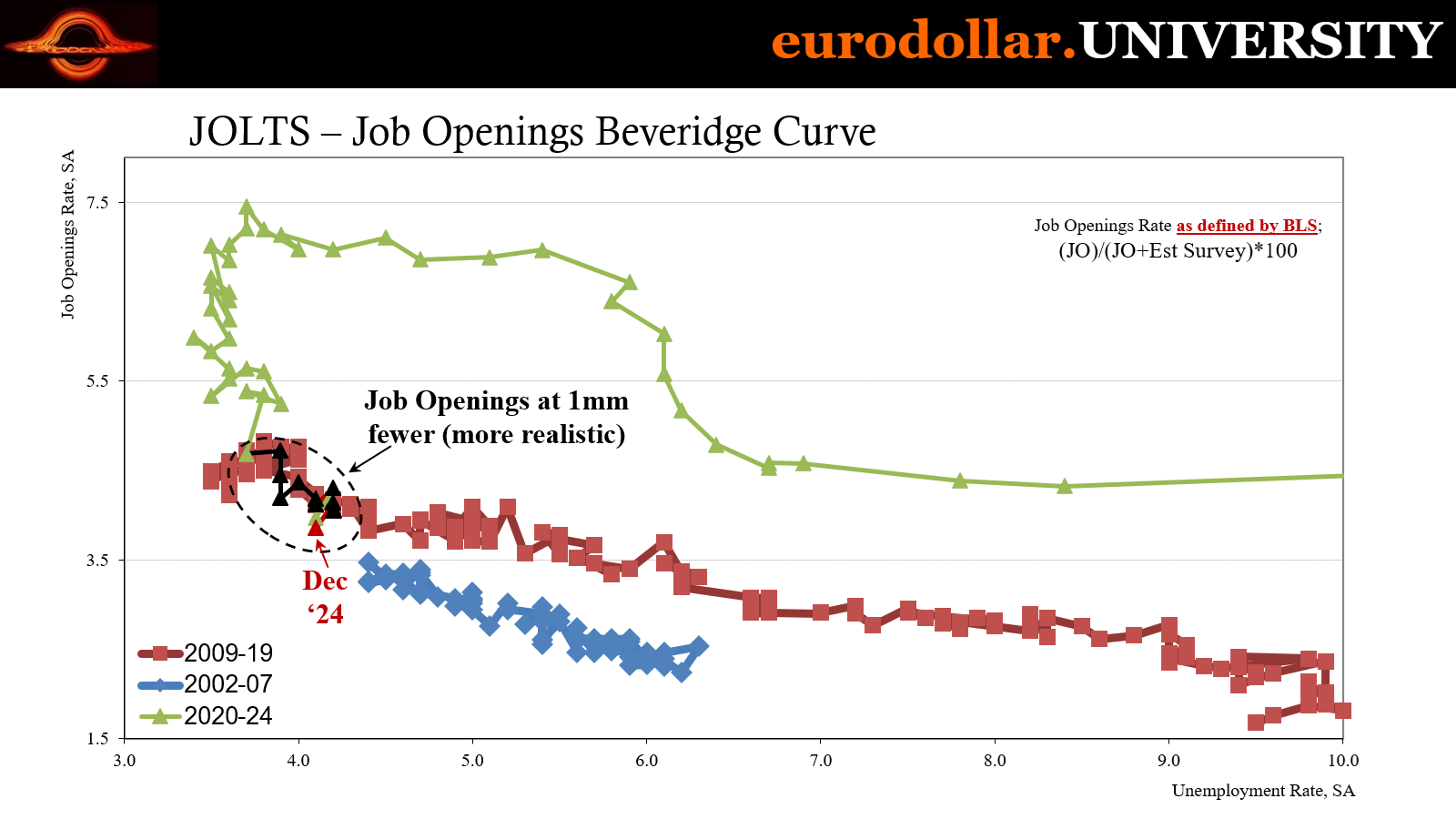

The reason why this threshold seems so high is momentum; lose it and everything is lost. This is simply the GDP version of the Beveridge Curve from the labor market. The latter uses the unemployment rate measured against job openings (or some better metric covering labor demand) to gauge when demand for workers has dropped so low we should expect layoffs and more widespread unemployment to result.

The transition to the “flat part” of Beveridge is where the employment situation has deteriorated enough employers are no longer content to cut costs by lowering hours and hiring fewer new workers (or replacing some that leave via attrition). It’s the spot when firms become more proactive about labor costs since the economy has fallen off too much.

In GDP terms, the full-year rate under 1.5%, and especially under 1.3%, is the same. This is when economic conditions have already gone too far, the slowdown slowed down too much the economy is no longer stable. Bad things don’t just happen from there, they snowball. This is where the vicious cycle gets fully going.

Like Beveridge, a GDP threshold is not some forward-looking signal, either, instead a lagging indicator confirming what had already happened.

GDP forecasting only moves the signal up in time, without the benefit of confirmation. Since we are all basically guessing, we’re essentially trying to estimate probabilities, either formally, like Morgan Stanley, or qualitatively as we’re doing here (I find quantitative measures exceptionally lacking, and so do their practitioners at least in private discussions).

From this point of view, if we find enough converging data, anecdotes, market pricing, etc., which altogether seem to raise the chances of GDP “growth” falling below 1.5% in any year, there is very real danger in a very real sense to the real economy no matter how any Economist or policymaker (same thing) might choose to lie about this.

The numbers here in 2025 are adding up, markets are behaving more the same way, King Dollar, not to mention, just as important, plain common sense. Plus, forgot how to grow recession as the starting point.

We’ve already had the Beveridge Curve warn about mostly the same factors, loss of momentum, etc. GDP going under 1.5% is the equivalent warning. Much of the world is beginning to come around to seeing it, too, if not quite able to grasp the gravity not to mention how all of this just fits with forgot how to grow and market signals from all the way back in 2022’s singular non-recession sendoff.