TOO MUCH DISINFLATION

EDU DDA July 11, 2024

Summary: The June 2024 CPI data didn’t just produce solid disinflation, it actually showed an alarming amount. For the second straight month, the core CPI dipped sharply and in a way we’ve rarely seen before. It doesn’t matter it wasn’t negative, it has clearly been pushed outside of its usual range and pattern. Examining its history especially during the worst recessions shows just how unusual and what it must take to create these abrupt and sharp changes to price conditions. The fact these are perfectly consistent with everything we’ve been getting only makes a strongly compelling case even more so.

Today’s release of the June 2024 CPI results was a lot more than expected. While it wasn’t actually the first negative monthly print, it was the first deep enough under zero not to be rounded off. Gasoline prices played a substantial part, as expected, but it was much broader than that. So broad and so deep, the consumer price estimates were a lot more concerning than many are taking them.

That isn’t to say mainstream observers aren’t scrambling to beg the Federal Reserve for rate cuts, they are. And the primary reason they are is simply because the price estimates mesh only too well with everything about the economy coming in. Most observers can now more clearly see just how dicey the situation is already.

June’s price data actually shows the risks are a lot more serious. It’s easy to brush it off as little more than a slightly higher chance of recession. This kind of price behavior is highly unusual and goes well past that.

The consistency with, first, rising unemployment over the past four months already makes the beginning of a strong case. US consumers had been hit with price changes and lost purchasing power for years, but now in 2024 there’s no savings left and fewer transfers coming from the government (there are still a lot of jobs, though it’s not nearly enough of them). Worse, oil and gasoline prices jumped as did insurance costs to pummel everyone one more time.

Many were quick to claim those as the start of resurgent inflation pressures. That was never really any risk, the consequences could only have been tied to the opposite – which is what we’re getting right now. Weakened consumers left with fewer options and then a labor market turned against them and the economy (no matter how much mainstream talking points ignored the warnings and the economics – small “e” - in favor of Jay Powell’s Economics slogan of “strong and resilient”).

We knew it was getting bad because Corporate America kept telling us. Every time anyone tuned into financial media or accessed X/Twitter, there was some mega-cap consumer-focused business announcing price cuts after admitting their customers were completely tapped out.

Just today, food behemoth Pepsi proved to be yet another one. In its latest earnings, the company warned along those same lines. On its earnings call, CEO Ramon Laguarta said, “In the US, there is clearly a consumer that is more challenged.” That’s the most charitable way to say what I wrote in the paragraph above.

The results plagued Pepsi across all its various brands. Laguarta even noted how Frito-Lay was suffering because of its higher-priced products, and not due to the “miracle” weight loss drug Ozempic. We all know Americans would be buying even more unhealthy snacks if they believed they could be immunized against the weight they’d otherwise gain, but they simply can’t afford to right now.

While gasoline did a lot of the work on the June CPI turning it negative, the disinflation was indeed widespread; in fact, it proved to be too broad-based and too much. If you want the set of numbers from the report, here’s today’s Daily Briefing with them (for those not subscribed).

They included shelter prices which finally broke down in a big way, too.

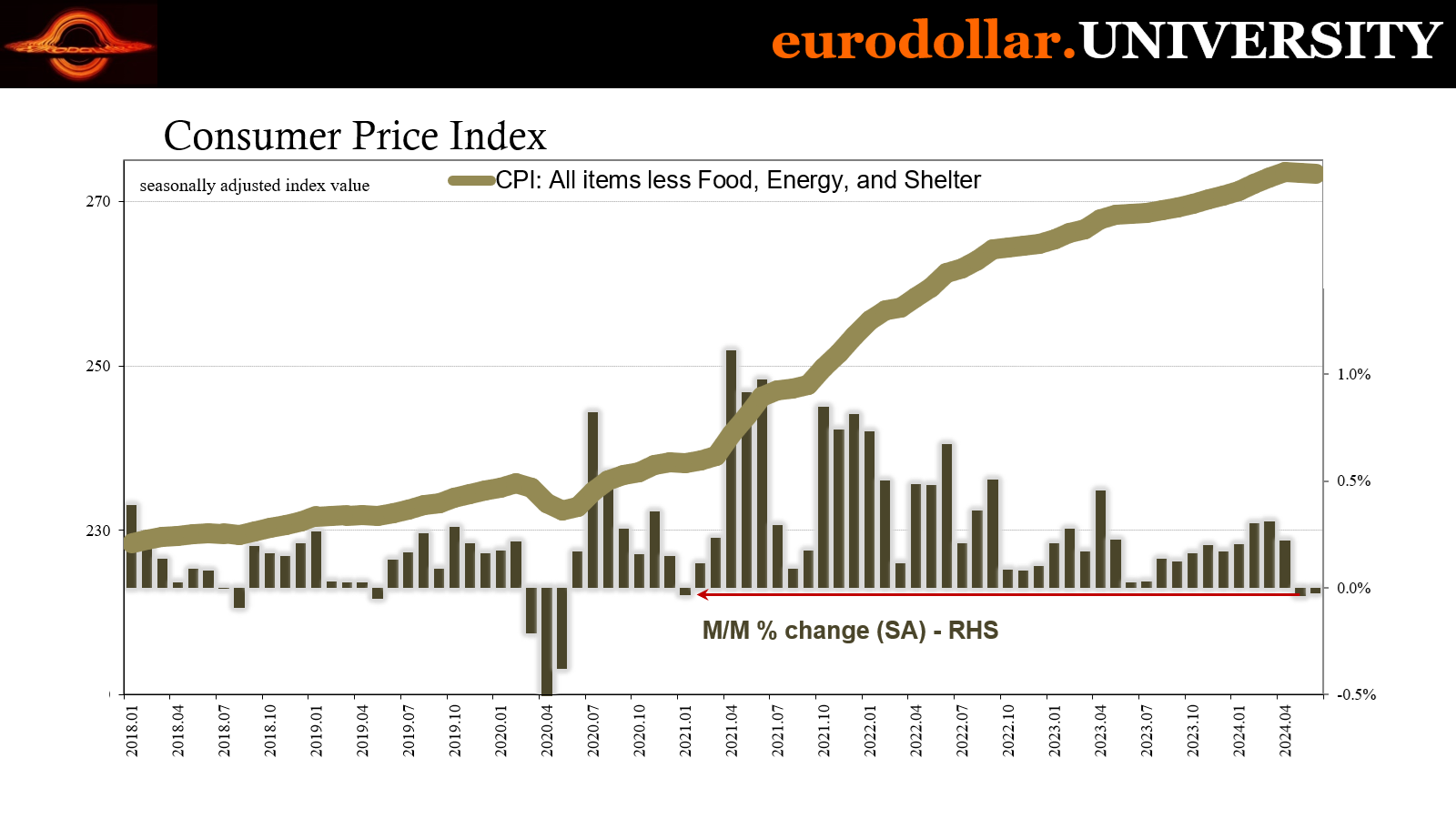

It’s the rest of the consumer bucket that we’re interested in, where Target and Walmart have been cutting back prices in response to the negative turn to the economy. In fact, the drop in the rate of change for the CPI’s core index is astonishing. While it doesn’t include Pepsi (that’s in the food index under Food Away from Home), the core takes out gasoline and food to leave us with an otherwise relatively stable price index.

This is the primary reason the thing exists in the first place. Left to an actually resilient or even weakening economy, these non-volatile prices will continue to rise in a rather tight range consistently month after month, year after year so long as they aren’t disturbed by a very big, well, disturbance. Core prices instead rarely break down in the way they have over the past few months, and when they have only because of some of the worst cases.

It truly takes a lot to suppress prices of what remains in the core CPI.

To begin with, its monthly rate in June was already nearly zero, just 0.06% which itself follows a minimal gain of 0.16% in May. You can clearly see on the chart just how abrupt and weighty this deceleration has been. The index further removing shelter was outright negative each of the past two months.

Combine those with the warnings from retailers and clothiers who are cutting prices, what this shows is a complete picture where the core CPI is capturing and corroborating not just the price activity more importantly where it’s coming from: that macro weakness they’re all referencing under their buzzwords.

To see exactly why this is unusual therefore of primary concern, we’ll look back through previous cycles to see how the core CPI and the core excluding shelter have both performed during them (even though I already spoiled it).

First up, the last supply shock 2010-12. Prices surged largely on oil rebounding though the acceleration was extensive reaching nearly every part of the price bucket including the core. Shellshocked businesses just were not able to respond to the initial recovery period nearly fast enough causing prices to adjust upward even as activity continued to be grim; the increase in gasoline was particularly unhelpful.

NOTE: I’m using the same scale for the monthly change in every one of these so you can easily visualize the comparisons between cycles.

There was a noticeable weakening in core CPI prices from late in 2009 (a particularly bad sign for the nascent recovery) then slowly yet persistently accelerating prices throughout the remainder of 2010 into 2011. Following the peak in August that year, price changes on the downside of that supply shock only ever decreased in the same fashion they had increased: slow and steady.

Excluding shelter, there was only one month – February 2012 – when that index dropped and only to zero (monthly change). Apart from that single occurrence, prices generally kept moving forward at a relatively consistent rate within their modestly slowing range.

During the Great not-Recession, there was only one other period apart from late 2009 which looks like what we have hear in 2024. The core CPI after July 2008 broke down and would eventually fall by 0.11% m/m that December. Before then, there were at most the two months before and after Bear Stearns (March ’08) when core prices were somewhat noticeably weaker; instead, it was summer and fall 2008 during the thick of the non-financial crisis.

The core less shelter is even more striking during that time. There was a modest weak month in February 2008 though, again, the real shift came after July through to the end of the year when the final three months (October, November, December) turned negative – and appear the closest comparison to the past three months of 2024.

Further back, during 2001’s dot-com cycle, the core CPI barely even noticed it. The contraction was mild enough to begin with, and the monthly changes only moderated a small amount toward the end when it was at its relative worst. There was more of a noticeable interruption when excluding rents/shelter, though even then the recession didn’t create the unmistakable, abrupt shakeup like late ’08 or middle ’24.

Going back another decade to the S&L recession at the start of the nineties, once again you don’t see much or any impression on the core CPI or the version without shelter. There was a notable though minor slowing in both, yet never anything more substantial than that.

There were no big recession slowdowns in either index during the various Great Inflation cycles. Underlying legit inflation shows up in the core parts of the consumer bucket consistently, so even the nastier and the nastiest parts of the four downturns (1969-70, 1973-75, 1980, 1981-82) you don’t get any kind of major break in the core CPI apart from the last stage of the last one later in 1982.

Unfortunately, we can’t go any further back at least not on a monthly basis since the BLS didn’t produce anything other than quarterly estimates for the core CPI before 1967 and the series itself only goes to 1957.

That leaves us with exceptionally few instances where core prices (and ex-shelter) suddenly and steeply decelerate in similar fashion to what we have right now. There’s late ’82 in what was the worst recession since the Great Depression up to that time, then either the second half of 2008 or latter 2009 after the worst of the massive destruction though with layoffs still happening.

I certainly don’t want to make too much of those comparisons, particularly the 2008 and 2009 ones, as that’s not my purpose nor my point in making these. The CPI or any part of it is nowhere near enough evidence all on its own, just one small if at times substantial piece to the macro puzzle.

For the Great not-Recession, there were far and away worse overall circumstances at that time than anything we observe right now, from major insolvency in the biggest global banks to the absolutely stunning degree of worldwide monetary difficulties then the mass waves of layoffs sweeping through the US by the summertime (summer is the time for recession) associated with all that.

We find little to suggest that much economic trouble developing here in 2024.

With that caveat out of the way, the point I am making is that the core CPI’s behavior points to far more negative possibilities than just a modest slowdown or even the small possibility of recession some of the more reasonable mainstream voices are now genuinely considering for the first time. It’s a little more advanced and serious than that; while it may not be to the same degree as the worst of the worst cases, the comparison does indicate trouble nonetheless.

It's all the more compelling because of how easy it is to connect the dots. Broad-based price actions announced by an entire array of big businesses (with likely smaller businesses doing the same, they just don’t rate the same coverage) picked up in the usually very steady core part of the CPI pushing it well past the point of benign disinflation while being told by those same companies why that is.

All of that entirely consistent with the growing majority of recent macro statistics.

What made 2008 so harsh was the level of job losses which came on all at once, beginning in the months even before Lehman and the full crisis. In 2024, it’s not so much the job losses up to now as it is lost incomes and purchasing power pushed to the brink by a softer employment situation than anyone cares to admit plus gasoline and insurance inconveniently piling on earlier this year. In both cases, the economy was sapped of a tremendous amount of potential in a relatively short amount of time.

Prices had to adjust to those fundamentals.

The next critical question is how it all evolves from here. Can the economy find a sustainable settled state that doesn’t involve a lot more unemployment? That seems a difficult challenge given what where everything stands. Nothing is impossible.

What the core CPI has done over the past few months is summarize and put a measure on everything we’ve been getting in the US economy recently. The fact similar results are rarely found outside of periods with major problems doesn’t mean we’re totally screwed, though it does soundly suggest the chances of a soft landing are indeed minimal while the probability of adverse cases (which could mean a lot of different outcomes, though just various degrees of bad) has gotten to be way too high.