MELTDOWNS AND LIQUIDATIONS

EDU DDA Apr. 4, 2025

Summary: Meltdowns coming in from everywhere. Strong indications of liquidations, including those tied to Japan’s carry trade. Stocks served margin calls and risky credit getting pummeled therefore collateral calls. Yields falling sharply, as are forward rates in spite of Chair Powell’s latest attempt to portray calm and even the same inflation bias. And the “experts” have the dollar all wrong. Again.

BASICALLY HOW EVERYONE FEELS - AND MORE THAN A FEW LOOK - AFTER THE PAST TWO DAYS.

Two terrible days to end this week. Liquidations weren’t just slamming the stock market, they’re hitting all corners. Oil prices, for example, down huge dropping WTI to its lowest per-barrel price since March 2021. Not only is the selling indiscriminate, it’s global.

Financial conditions are getting pounding with what look to be forced selling, zeroing in on monetary and funding difficulties. We see Japan present in a lot of this, a key sign. Because of that, the market is betting stronger and stronger against the Fed, on the curve as well as in forward rates where those contracts made a break, too.

Equities along with energy are getting the worst of it at the moment. Why? Everything was and maybe now is in place for how the world is taught to see recession. The precursor state is already there, an economy that has shown consistent signs of weakness and slowing. Starting from there, not strong and resilient, all it takes according to standard theory is some shock. As I pointed out for my last webinar, recession is widely believed to be triggered by an external event.

Tariffs and retaliation would fit the bill for that event for many people.

Markets had already been pricing weakness for a long time. Even within stocks, parts of the marketplace were worried over cyclical dangers from as far back as last July. The Philly Semiconductor index (SOX), as I’ve been pointing to ever since then, has been one of those consistently pricing the first part of the recession equation.

Selling off more than 15% Thursday and Friday alone, SOX is down nearly 30% since mid-January and just shy of 40% from its high last July. Weak economy plus shock equals the R-word.

This explains why stocks are taking the past few days so harshly, along with real commodities, too. As to the former, shareholders know to exit their positions once the recession (traditional) chances get to be too much. They can’t sit around and wait for confirmation. In other words, for stocks the world has just crossed the first threshold, the point beyond which the recession question has become far too much of one to be anything other than taken very seriously.

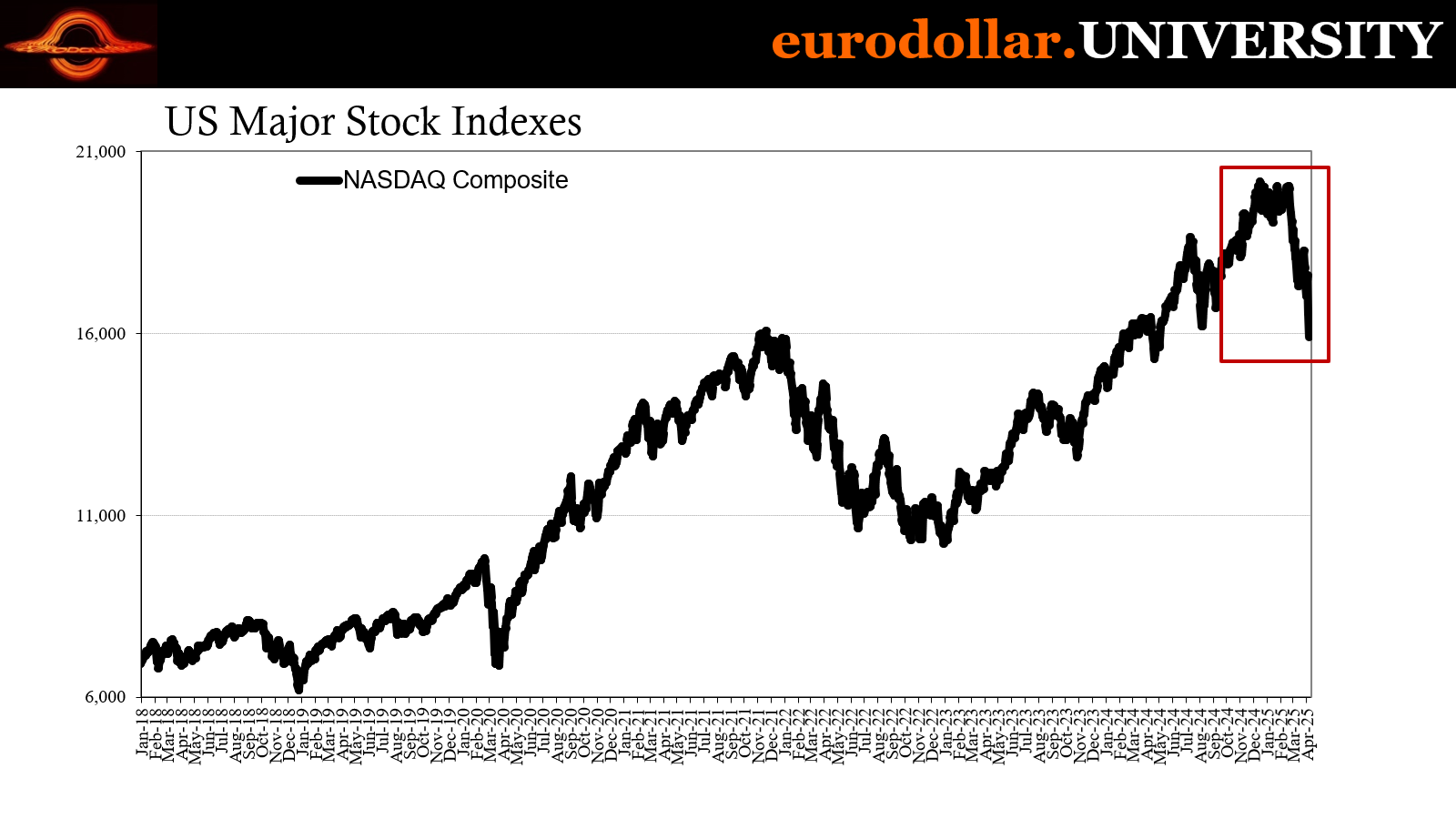

Major indexes like the NASDAQ and S&P500 skipped way past technical correction to now edge the dreaded bear markets. NASDAQ has already breached the 20% decline mark, with S&P not too far behind at -16% from its last high.

The extreme moves of the past several days point to margin calls and liquidations, the factors which lead to self-reinforcing declines like we’re seeing here, further calling into question financial “liquidity”, broadly speaking.

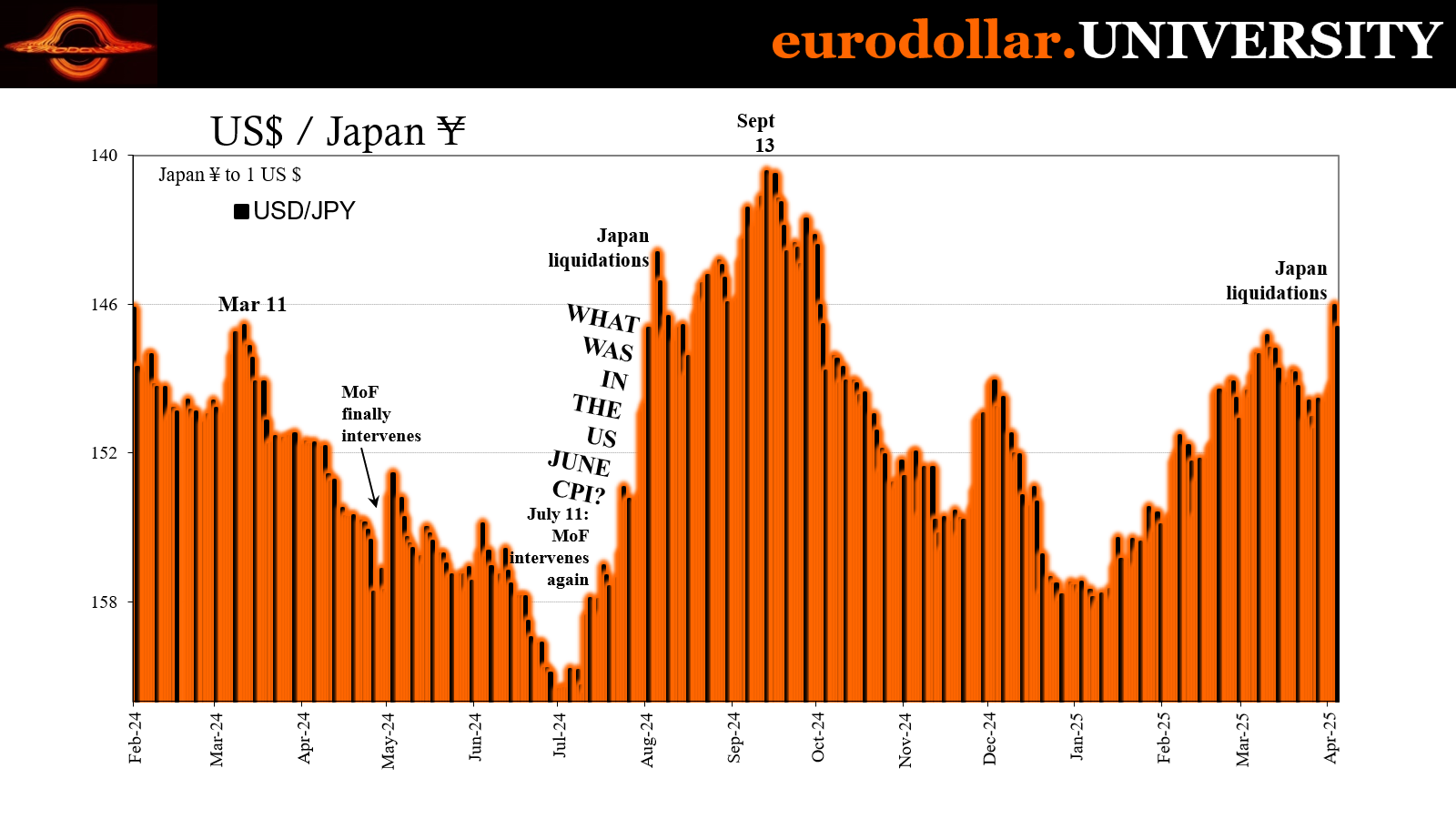

Japan is a key one of those signals, producing or reproducing here more than a little taste of August. The Nikkei has been utterly pummeled, in tandem with the SOX if with more noticeable emphasis over the past week. The official close for the 225 has the index at 33,780, while futures and after-hours currently put it 32,530 for a 6.4% loss today alone. This works out to a 16% drop from late January and 20% off its last-July high, too. In fact, its currently-indicated value is less than a hundred points from its August 5 low.

That earlier carry trade reverse began on Japanese overseas positions forced into liquidations by deterioration in funding and credit markets which arose over fears the risks of a traditional recession in the US had gotten to be too high. All that was missing from it was the final shock to push it over the edge, which may have now been provided.

Credit liquidations were created from margin calls that also spread to Tokyo shares, what’s known as a VaR shock. Since junk credit and equities are highly correlated, recession fears spooking junk credit investors leading to selling among them push volatility calculations up around the financial system. Volatility is the leverage killer.

As prices on riskier credit suddenly fall, implied volatility soars for any related asset classes. Higher volatility, broadly speaking, means there is a heightened chance values in those classes can take a significant hit. Lenders providing leverage in those markets see higher implied volatility as a greater probability of loss to the lender since lower asset prices mean less protection in case of default.

Lenders pull back funding – the margin call – or demand the borrower put up more or better collateral – the collateral call – which often enough triggers forced liquidations since most highly-leveraged counterparties don’t have the spare funds or collateral to meet these demands from funding providers.

Japanese carry traders happen to be the most overexposed since the Tokyo equity market’s incredible recent run (to March last year) had brought in so many parties on leveraged bets. Volatility in dollar credit spills over into Japanese stocks, with two kinds of carry trading in the middle of each.

Not only is the Nikkei down sharply this week, the Japanese yen has jumped higher, too, yet another strong signal for carry trade (the first type) reversal. Some of those liquidating (involuntary or otherwise) will repatriate funds to Japan, raising demand for yen in the short run relative to any other currency. Thus, while the dollar is rising (not falling, as many are claiming; more on this below) against others, it is “weaker” relatively to JPY.

Over the last week, the yen has moved up from around 150 to the dollar to 146/147. Those are its highest values against the greenback since last September, the final major carry trade reverse of that earlier episode.

Credit spreads have indeed skyrocketed the past few days, over and above the leap they had made from their lows in mid-February and with most of the move coming after the middle of March. The Morningstar LSTA Leveraged Loan 100, which tracks the most “liquid” and transacted leveraged loan products, certainly busted below 96 (index price) today. It was at 96.60 yesterday having dropped from 97.33 the day before.

That will put the index below August, a new lower low and likely a trigger for margin/collateral calls in the space.

Other credit spreads widened massively yesterday – we won’t have the numbers for today until next week – starting with the riskiest pieces. ICE BofA’s CCC index, the lowest tier, saw its calculated spread (index) soar to 1018 bps from 888 bps last Friday. Add in another ~100 bps from the blowup today, that’s a good indication of not just panicky selling more importantly forced liquidations from margin calls where funding providers are pulling back, effectively tightening financial money available.

Some of the higher tiers of junk also made similar moves, meaning more widespread difficulties not specifically aimed at the worst of the worst. ICE BofA’s Master II option-adjusted spread spiked to 401 bps yesterday, an almost-seventy-point jump since last Friday that likely shoots well over 100 bps when today’s numbers are released. And the low from February was 262 bps, meaning overall a substantial rise in a relatively short period of time.

This is also well above the previous high from the carry trade blowup last summer, representing a significant escalation. In fact, the last time the Master II was as high as it is (probably) today was October 2023. Unlike August, however, this jump in spreads has been sustained over more than a week, now reaching nearly two months with more disorder thrown in.

No surprise, then, interest rates worldwide have been moving sharply lower – starting with, yep, Japanese bonds. Back then, JGBs were driven downward even though the Bank of Japan had just hiked its policy rate. JGB 10s sank from 1.06% to 0.75% in a matter of days with everything in meltdown. It had nothing to do with Japanese central bank actions and everything to do with perceived recession risks in the US not to mention globally.

Over the past few days, Japan’s 10s have slid from almost 1.60% last Thursday all the way to 1.16% as of today with everything melting down all over again.

Up until maybe the past couple days, BoJ officials including Governor Ueda had been suggesting their next rate hike may be as soon as next month. The JGB market is taking that one off the table for now, at least.

So, from Nikkei to JPY and now JGB, it all fits not only with carry trading in reverse but also pointing to monetary difficulties at least on the financial side of the world. This encompasses the entire financial world beyond strictly what the Japanese are involved with. Too many big moves that reckon margin and maybe collateral calls coming in.

Naturally, market interest rates have tumbled. While they came back from their lows early on today, Treasury yields remain down huge anyway. The critical 2-year note yields 3.63% as I type this, having been as low as 3.53% this morning – which would have surpassed the September lows for it.

That’s another critical signal we’re watching given how important the 2s spot on the curve is. This is where longer-term independent growth and inflation expectations collide with those of the Federal Reserve therefore typically the mainstream, too. When those are in opposition, as they are now, the 2s can become sort of a referee, a judgement as to which side might be “winning” the argument.

LOL

Markets worldwide are pricing trade wars as part of the overall weak/slowing economy direction. Therefore, any impact on consumer prices and business costs is being viewed as demand destructive, maybe a short run pick up to the CPI before ugly weakness especially in labor markets (plural). We’ve already seen the latter before even getting to tariffs, with the Household Survey (released today) ugly in the US in February then not making much of it back during March, raising the chances February wasn’t mere statistical noise and therefore the two-month period combined was probably a negative (no one cares about the Establishment Survey, either as old news or simply recognizing how much it overstates demand and activity).

The same happened in Canada where the Canadians just reported a sharply negative March payroll estimate which follows a nearly flat reading for them in February. Both pointing to the weak economy primed for a “shock.”

From the Treasury market’s perspective, it’s gotten to be strong enough of a global signal to overlook the Fed’s unwillingness to give up tariffs as possibly “inflationary.” Jay Powell just today said he isn’t at all sure despite all the melting down.

Powell said that the tariffs, and their likely impacts on the economy and inflation, are “significantly larger than expected.” He also said that the import taxes will probably lead to “at least a temporary rise in inflation,” but added that “it is also possible that the effects could be more persistent.”

“Our obligation is to ... make certain that a one-time increase in the price level does not become an ongoing inflation problem,” Powell said in remarks delivered to a conference of the Society for Advancing Business Editing and Writing.

Markets are saying with growing confidence he’s wrong. That’s the 2s sliding toward new lows, siding with the 10s and the long end on growth expectations.

We’re also seeing this in term-SOFR futures. I’ve been highlighting two spots on the forward rate curve as places to watch: December 2025 and June 2025. The former had already broken out of its prior multi-month range from last year, with the forward rate market pricing a higher chance the Fed would be proven incorrect on tariffs-as-inflation and with a strong bet already on them having to pivot to lower policy rates again at some point.

The past few days, the June 2025 contract has now broken its range, too, meaning a rising perceived chance “at some point” is becoming sooner than later (stock market liquidations do help with this, too). Plus, with the latter part of the forward curve receiving massive hedging interest, participants are also back to hedging rates going a lot lower once they do get going (basically what the swaps market has been pricing since 2023).

Powell was never going to add to this week’s carnage by saying much. The most he ever would have said was that the Fed is confident in the economy, which the Chair did reiterate in his remarks today. Yet, Powell also went beyond them to once more emphasize the potential “inflationary” aspects of tariffs which the market says there’s zero chance for.

Finally, the dollar. As earlier in the year, some are mistaking the euro for the eurodollar. What I mean is, the euro has been tracking higher against the dollar in exchange value which has naturally influenced DXY leaving many people (including far too many so-called experts) with the impression the dollar is rapidly weakening as if the world is “fleeing” the dollar, its assets, or anything remotely associated with what they wrongly understand of the currency.

While overall exchange values have been volatile these past few days, the dollar is higher against more than not including those like CNY which really matter. Mexico’s peso had jumped yesterday then got dumped even more today. Nearly the same for the loonie, or anything other than the euro (and yen, for the reasons stated above).

HUH?

CAD like MXN has barely moved from its lows set earlier in the year. CNY (onshore yuan) is racing back toward 7.30.

A persistently “strong” dollar, in addition to forced liquidations and distressed selling, those are the kinds of monetary difficulties that aren’t going to be inflationary even if tariffs would have been like the Fed fears. That’s ultimate the key takeaway from everything – the margin for error has shrunk so low that’s the reason for so much widespread reaction in all these various ways and places.

Even if it is all basically a knee-jerk response to irrational fears over tariffs, what even that shows is essentially zero faith in the “strong economy” let alone an inflationary one the FOMC constantly frets.

The good news is that nothing is ever a done deal until everything is signed and delivered. That doesn’t appear to be the case right now, the harsher economic results (forgot how to grow remembering how to recession) isn’t presenting in the current data. We’re still looking at probabilities, therefore anything is possible and this could be another false start.

That said, those probabilities are getting slimmer and slimmer each time something like this materializes. Market positions are more and more confident, not less. Not to mention longer run indications have consistently pointed to just this kind of eventual outcome: lower and lower interest rates, volatility then bad macroeconomy.

We may not be there yet, but what’s happening really does look the most like “there” we’ve gotten yet.