Daily Briefing 3/12/25

Consumer Price Index (BLS)

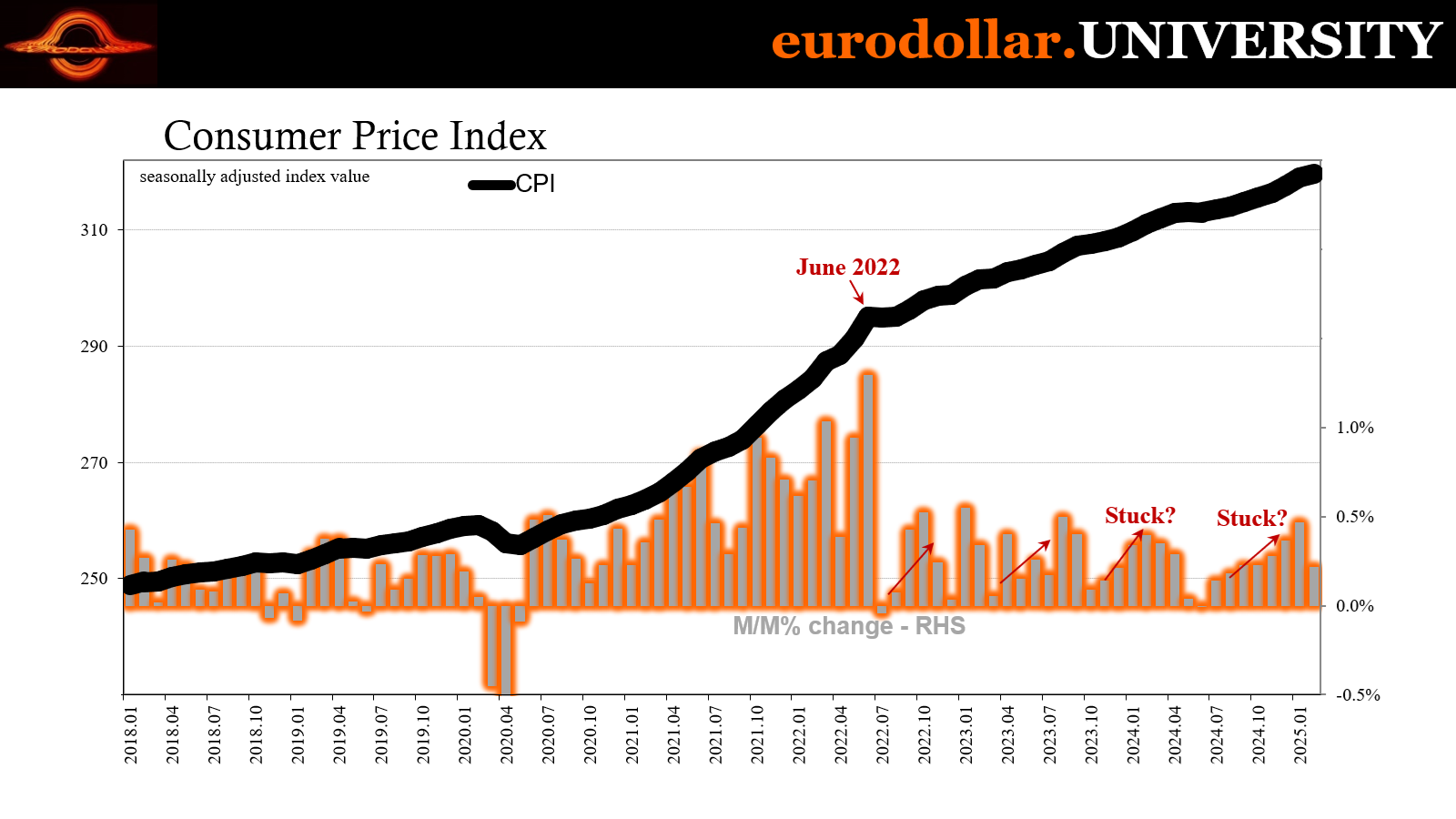

In February 2025, price expectations slowed, with the Consumer Price Index (CPI-U) rising 0.22% month-over-month, down from 0.47% in January. Year-over-year price expectations eased to 2.8% whereas core “inflation” (excluding food and energy) also decelerated, rising 0.23% for the month and 3.14% year-over-year (lowest in nearly four years). Shelter costs remained a key driver of price expectations, though their impact has lessened. Energy prices declined, with gasoline down 1.0% in February, while food prices increased slightly by 0.2%. Notably, airline fares fell 4.0%, reflecting weak demand, and new car prices also declined, suggesting preemptive consumer buying last year ahead of expected tariffs.

Interpretation

The February CPI report provides further confirmation that price expectation pressures are continuing to ease across key segments of the US economy. The 0.2% monthly increase in the headline CPI, down from 0.5% in January, aligns with expectations of a gradual “disinflationary” trend.

A major driver of price changes remains the artificial shelter index, which rose 0.28% in February and accounted for nearly half of the overall price increase. However, the fact that its rise was more moderate compared to previous months suggests that the impact of imputed rent calculations (a methodology often criticized for its lagging nature) is beginning to wane. On a 12-month basis, shelter costs increased 4.2%, marking the smallest annual rise since December 2021. Given that actual rent growth has been slowing in private-sector data, the shelter component of CPI will continue to ease in the coming months, further reducing “inflationary” impressions.

One of the most notable developments in February was the decline in energy prices, with the energy index falling 0.2% year-over-year. Gasoline prices dropped 1.0% month-over-month and were down 3.1% over the past year, while fuel oil saw an even steeper 5.1% annual decline. These decreases contrast with rising electricity (+2.5% YoY) and natural gas (+6.0% YoY) costs, which have offset some of the benefits of lower gasoline prices for consumers. As the weather warms up, however, those effects will also fade.

Transportation services, particularly airline fares, played a major role in February’s softer price expectations reading. The 4.0% month-over-month decline in airline fares, following a 1.2% rise in January, signals that airlines are struggling with weaker demand. This aligns with recent earnings warnings from major airlines, including Delta, whose CEO described the current quarter as a “parade of horribles.” Given the decline in fuel costs and weakening consumer demand, further softness in airfare pricing could persist, helping to keep overall price expectations subdued.

New car prices also declined slightly (-0.07%) after a barely fractional rise in January (+0.04) as it appears many buyers had front-loaded purchases in anticipation of potential tariffs on imported vehicles.

The broader implications of this report point to continued “disinflation”, albeit with the same uneven trends across sectors. Shelter remains a key driver but is losing momentum, while energy and transportation prices are exerting downward pressure on price expectations along with air fares.