SIDEWAYS TO THE 2s

EDU DDA Jan. 30, 2025

Summary: A global deluge of GDP reports. Not surprisingly, they showed a lot more sideways and not just across Europe. Starting with the Europeans, though, GDP misses and more than a few minuses show that nothing has changed either in the economy or most officials’ interpretations of it. More importantly, it isn’t solely Europe where we see sideways. Most of all, this is right where the 2s had had the world going after central bankers won the bank crisis battle then unknowingly lost the money and macro war.

SIDEWAYS HAS GONE GLOBAL.

Gold prices finally surpassed their previous high today, nearly hitting $2,800 per ounce for the first time. While the prospect for “trade wars” dominates the commentary surrounding it, not to mention everything else, the key datapoints released today from all over the world instead point to what Mexico’s deputy finance minister either doesn’t get, or won’t admit.

There were GDP reports coming in from all over the globe, starting with the very much expected setbacks throughout Europe’s largest economies. Germany fell; France, too; Italy stagnated for the entire second half of last year. As a result, Euro Area (19) GDP was basically zero, a difficult disappointment given how many had previously though the continent was building momentum toward a breakout at long last.

Looking at each GDP series, however, you can far better see what’s going on here. Because there isn’t some massive, immediately-recognizable collapsed in output officials, Economists, the media, no one has any idea what to do with these results.

If it was only Germany, OK, fine, maybe it would be entirely about political choices. But France, too? Also Italy, one country which had performed genuinely well during 2021 unlike the nominally-driven fake price illusions near-everywhere else.

It didn’t end there, however. The Europeans may have pioneered this unique-looking contraction, the first to trend sideways as opposed to either up or down with output. Globally synchronized is becoming more globally synchronized, not less.

Outside of Europe, Mexico just confirmed the spread. GDP there fell sharply in Q4, dropping 0.6% during it which was, by far, the largest decline since 2021. In response, Amador Zamora did his best to downplay the result, blaming everything from climate change to guacamole wars. As Mexico’s Deputy Finance Minister, no one should expect anything more from the guy.

Mexico’s Deputy Finance Minister Edgar Amador Zamora later Thursday attributed much of the last-quarter downturn to drought and climate change that weighed on manufacturing and spurred the agriculture sector’s worst performance in a quarter-century.

“This performance doesn’t imply the Mexican economy is in a recession or that it will enter into one,” Amador said at a Finance Ministry news conference. More than half the contraction in the fourth quarter data “is explained by the poor performance of the primary sector.”

OK, yet if it was only slightly more than half the contraction, that still leaves another half of the worst GDP estimate in years. Even if it was only -0.25% excluding agriculture, as the numbers show, then that’s also the worst quarterly result of the cycle so far.

The focus on how much of a negative Q4 “should” be is yet another distraction, too, since it is hardly the first sign of weakness.

The Mexican economy isn’t quite to Germany or Ireland territory, yet unbeknownst to most it is halfway. GDP has been weak and going mostly sideways from all the way back in the third quarter of 2023 – that same initial inflection as what hit the American labor market. For our neighbors to the south, there was the inventory cycle already but also an abrupt shift in the massive nearshoring buildout Mexico was experiencing.

Going to back to the summer before, 2022, the Mexican economy had been supported by two major countercyclical factors, starting with the belatedly-recovering auto business out of sync with the rest of the goods cycle. The other one was a flood of investment and construction, supply chains being moved out of China (see: Chinese FDI) and other places around Asia into Mexico (and still other places around Asia).

Between August 2022 and October 2023, Industrial Production in the country jumped by 7.1%. Construction output alone absolutely exploded, soaring 35% in that same short time period.

Then, seemingly out of nowhere, it just stopped. Construction didn’t completely reverse and revert to its previous position, though it did take a clear step back and has yet to recover that former peak even if production and building remains elevated compared to where it started. As of November 2024, construction is down almost 10% from October 2023, and several percent from the summer of 2023, while remaining 20% above levels in 2022.

Is that the work of a forming recession? Or normalization?

It’s another case of confusing results. It doesn’t fit neatly into the cyclical outlines and definitions we’ve been given, that that begin and end with a bimodal assumption – either an economy is visibly shrinking, or it is must be strong and resilient.

That supposition didn’t work in the 2010s, either. Not-enough-growth is a contraction maybe in its own class with its own set of destructive tendencies; all the more so when not-enough-growth follows a contraction period and thereby cancels out badly-needed full recovery.

Mexico is already another example of that here in the 2020s, joining places like the above-mentioned in Europe while also those like South Korea. GDP therefore economic output – in real terms – never really got close to recovery and then just stopped. For the Mexicans, that point of departure was around October 2023.

The timing isn’t random.

After all, why did bond yields tumble starting right then, too? By every other mainstream assessment, late 2023 was the point of maximum inflationary risk, overrun with media as well as central banks each hawking higher for longer, not to mention, for Treasuries, those about to be destroyed by the ongoing fiscal explosion crisis. Yet, why didn’t any of those seem to matter at all?

Long run fundamentals.

Going back to late 2022, the even more massive reshaping of global curves had signaled growth potential had taken a major hit, and it sure wasn’t those still-early rate hikes nor the rest that followed after them which did it. As I’ve pointed out before, look at, for example, how Germany’s 2-year previous to all this had closely followed (slightly ahead) the ECB’s rate hikes throughout 2022.

Once the September (not gilt) crisis erupted, suddenly the market behavior clearly changes. It went from slightly ahead of the ECB to slightly lagging. Then once the 2023 banking crisis erupted, German 2s stopped tracking the central bank entirely. This was a pronounced and profound shift in the marketplace that was entirely lost in the congratulations over how officials appeared to handle that bank crisis.

A case of them winning the battle and losing the war.

From that point on, the bond market worldwide began to (mostly) ignore (there were short run fluctuations along the way) central bankers. The critical 2-year maturity told the story the entire way (it hadn’t just been the German 2s; I had repeatedly pointed to the UST 2s in the summer of 2023 up to and during the September effect selloff). October 2023 was simply the next step in the transition process begun the year before, and accelerated by the March 2023 bank matter.

That’s what bond yields are, after all, at least when unmolested by central bank interference: growth and inflation.

It was a significant enough transition that even the 2-year maturities were increasingly disregarding the interference. That’s what makes the 2s such a critical signal, sitting right at that spot on the curve where both factors – CB policies and fundamentals – are normally balanced. So, when they become unbalanced to this extent, it is a clear expression of fundamentals over policies no matter how intent officials may be in enacting them like they had been all through most of 2023.

Look at the chart for the German 2s (above); that yield has gone lower ever since March 9, 2023, meaning you can make a case the bond rally really got going the day SVB failed. The process in the monetary system and the transition in the global economy got going the fall before, and it would take another step the fall afterward. While Germany’s schätz went sideways to lower the almost two years since then, the ECB (and the Fed) kept raising rates while also declaring its intention to leave them however high they got for a very long time thereafter.

And that wasn’t idle chatter, as it so often is with jawboning central bankers. Lagarde’s crew immediately raised by another 50 bps not even a week after Credit Suisse went down. Following that there were another four 25-bps hikes. In other words, the ECB added another 150 bps more to its policy rates all the while Germany’s 2s only went lower.

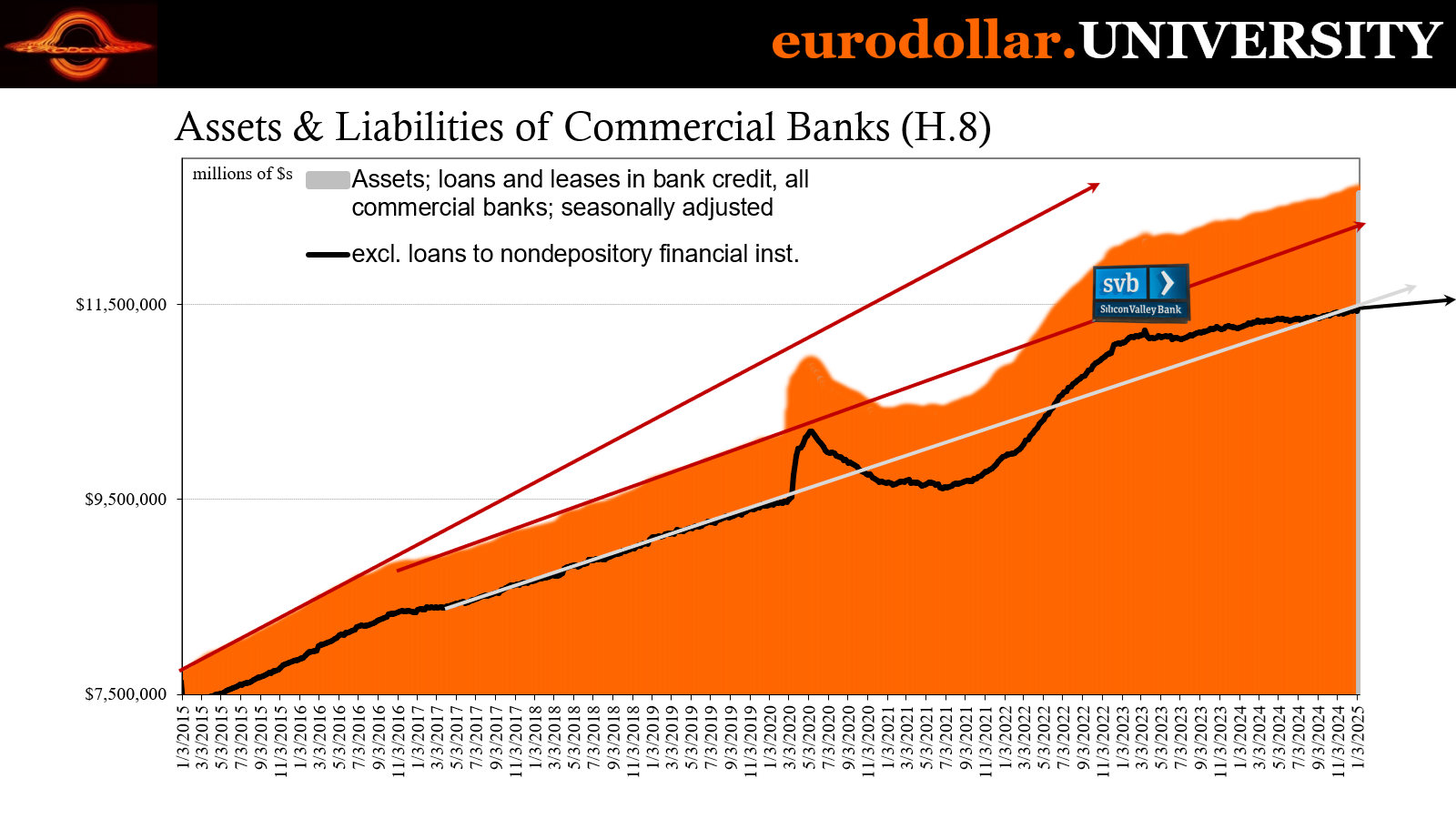

Again, winning the battle on the banking crisis yet more importantly missing the turn in the economic “war” the banking crisis itself represented (I covered the Fed’s miss and how American bank lending did the same thing bond yields did after SVB). Bonds declared the probabilities of lower growth (and inflation) from that point forward had soared; that’s what the growing divergence between markets and policymakers had always signified.

Because the global economy didn’t immediately crash during 2023, this perspective has been lost in the way expressed by Mr. Zamoro. What Mexico’s experience adds, though, is that this process of lower growth potential hasn’t been nor is now uniform. As much as I might throw around the term “globally synchronized”, it is variable and hardly monolithic.

As it turned out, Mexico had a little longer runway, so to speak, compared to Europe being supported by its two factors, autos which were out of sync and nearshoring as, at first, a serious countercyclical force. Now with both having already faded, Mexico begins to look more like Germany.

Sideways is now practically everywhere as each place runs out of runways. Even US GDP, for example, missed expectations for Q4 because outside of PCE (consumer spending) almost everything else was weak and even negative, particularly capital expenditures (contracting for the first time in years, and by the most since Q2 2020). The American economy is the furthest from sideways, exhibiting the longest runway, yet the signs of sideways are there, too, especially labor use and hiring.

The more we see sideways the more it confirms the lower growth didn’t just happen as 2s strongly warned, it also remains the future, validating how all this had gone unnoticed and unappreciated for years without recognizable recession and in the shadow of a bank crisis the public has been led to believe left no lasting damage.

Only now central banks are following the 2s.

The most devastating aspect of Europe’s Q4 disappointment is that it was one. GDP had been modestly accelerating in the middle of last year, raising hopes that the area was slowly pulling out of its mess, however one might categorize it. That’s one thing everyone does agree on; Europe is a mess, whether you call it “stagnation” or simply “damned.”

The widespread weakness there in the fourth quarter resets everything back to zero anyway, further establishing how we’re all stuck with sideways – as a best case.

That’s the thing; sideways is that lower growth, the transition from the artificial high of the supply shock period and its insidious price illusion, to the long run potential devastated by the impoverishment, the lost purchasing power of that period. Some places have or had more runway than others, by the end, as the 2s warned, it’s all sideways from here right on through to a 2020s that look way too much like the 2010s.

Thus, gold is soaring. Not because of trade wars, at most how those could contribute even more to what’s already going wrong. As the other side of copper to gold, it’s got the ratio in the 2020 or 2008-09 territory not because the economy is going to crash, but because it already did.