THE LACK OF LEHMAN STANDARD

EDU DDA DEC. 27, 2023

Summary: Continuing to evaluate the effectiveness of our monetary and financial signals. With markets on a rampage right now, it is as important as ever to calibrate and review. What have massive inversions really been saying all this time? What does their increasingly negative spreads say about what’s still ahead?

It is, at first, anyway, fair criticism. From the outside, all this stuff we go over here at Eurodollar University may seem at best trivial. Interesting, sure, but ultimately useless. After all, curves have been screaming bloody murder for a long time already, so where’s the damn body?

That’s the thing, though. There is one; several, actually. It just doesn’t look like what everyone has been led to imagine. To most people, they’re associating massive curve inversion with Lehman 2.0 and a repeat of 2008 if not something worse. The corpse they’ve got in their mind is some victim from a slasher film, gored up with a mess spilled all over the place.

This is Lehman syndrome. Having established what the worst case can be for the modern 21st century world, anything short of it seems practically uninteresting to the point of being of no concern. Compared to the mutilated victim, a simple body over there in the corner not moving with no obvious signs of distress can’t even rouse a little suspicion.

Our standard is not a major systemic collapse, nor should it be to any reasonable and honest observer. Something like that does not encompass the entire universe of bad scenarios. In fact, the worst case wasn’t actually 2008 anyway, it was the repeated and cumulative setbacks (which these signals uncovered) over the intervening decade and a half which deprived the world of any chance at full recovery – as I wrote recently, exactly what eurodollar futures had priced in 2011 and throughout Euro$ #2.

The biggest criticism I get on social media or in casual conversation is what I wrote above; curves are interesting and all, though who knows about those swaps and other complex numbers, it just doesn’t seem to matter. For a little while, sure, when SVB and Credit Suisse were all over the internet and markets, then the average person could plausibly correlate our set of numbers with the world which seemed to be unfolding then.

Since, it all just up and vanished; a Great Big Nothing. The inversions remain, but that seems to be the problem since the US economy appears to be just fine if not better than fine. GDP just put in around 5%. Labor data isn’t awful by any stretch as the unemployment rate actually declined in November back to what used to be a fifty-year low.

What does any of this other nonsense matter?

Answering that question is a key reason why I’ve begun the series of background checks on those various esoteric curves. But like yesterday, I want to stay more current today because there’s a lot happening right now that can get lost in this “disappointment” over not witnessing the end of humanity.

We do have some bodies to examine and they are instructive.

The first one belongs to Great Inflation 2.0. Remember, it wasn’t all that long ago you couldn’t go more than a pair of tweets without someone confidently comparing Jay Powell to Arthur Burns while saying with certainty how 2021 was already the next 1971. Inflation was here to stay, they said. The Fed was way behind the curve and we’d all pay for it with out-of-control prices well into the 2020s if not longer.

Except, the Fed wasn’t behind the curve, the curves instead all said it wasn’t going to end up that way. Nothing is ever zero chance, but in financial terms Great Inflation 2.0 was as improbable as to be almost zilch. We knew that because of what the curves are first and foremost – the monetary system.

Inflation is money, not supply imbalances. The way the markets were behaving left little doubt.

Basically, from the very first inversion in eurodollar futures way back at the end of 2021, that upset was as much about the non-existent chances of another Great Inflation as recession or anything else that has or will still come up. Again, those contracts are about interest rate mechanics, and interest rates are backward from the mainstream.

Eurodollar inversion was the market saying there was a growing chance wherever ST rates got to be in the short run they’d likely as not end up going back the other way. Permanently lower rates, as everyone should’ve learned from the 2010s, are the opposite from inflation.

With more and more disinflation if not deflationary data coming through in the final months of 2023, Great Inflation 2 has disappeared with each new low in whatever deflator rate. Surprising to some, not on the curves. That one wasn’t about Lehman, either, it was the initial stage setting the stage for rates to go lower again.

As far as the economy goes, since most of the public associates yield curve inversion with recession, the lack of one seems an obvious omission. Yet, that fails to account for where there are and have been outright contractions already, notably Germany and Europe.

Furthermore, in real economy stuff there was also failed China reopening. Where Germany and Europe fell into recession (score another body for curves), the US lost a substantial amount of strength and combined those conspired to kill any chance for the Chinese by crushing the global environment the Chinese were counting on to do most of the reopening work.

Together with other esoteric signals like the US$ especially against CNY (which when down equals bad for a reason), watching our eurodollar signals told us the premature celebration over China was, well, highly premature. In fact, those signals were so spot on; the reopening euphoria faded so fast today it is scarcely remembered, that’s how little impact it ended up producing.

It was so bad, the reluctant authorities in Beijing have had to pull out some stops to try to stop the reversal.

More recently, very recently, we’ve uncovered yet another body: higher for longer. That slogan was 2023’s official theme, too. At every opportunity, whichever central banker from wherever central bank proclaimed it all but certain interest rates once they got up would stay up for so long we’d never see the end of them.

Inversions were a decided bet against it. As the Fed has let the pivot genie out of the policy rate bottle, and with market yields on a rampage right now, while it’s too early for a conclusive determination the balance of probabilities are decidedly in that favor (as I wrote yesterday of things like the NTFS).

Cumulatively, what all those have in common is…interest rates. They are all outcomes which a rational analyst would have immediately associated with global yields dropping back toward where they had started out prior to this whole 2020 and aftermath mess.

But the thing is, we aren’t done. We still don’t know exactly how the supply shock era will fully finish up. Those I’ve already listed are just the first part preparing for the final straw.

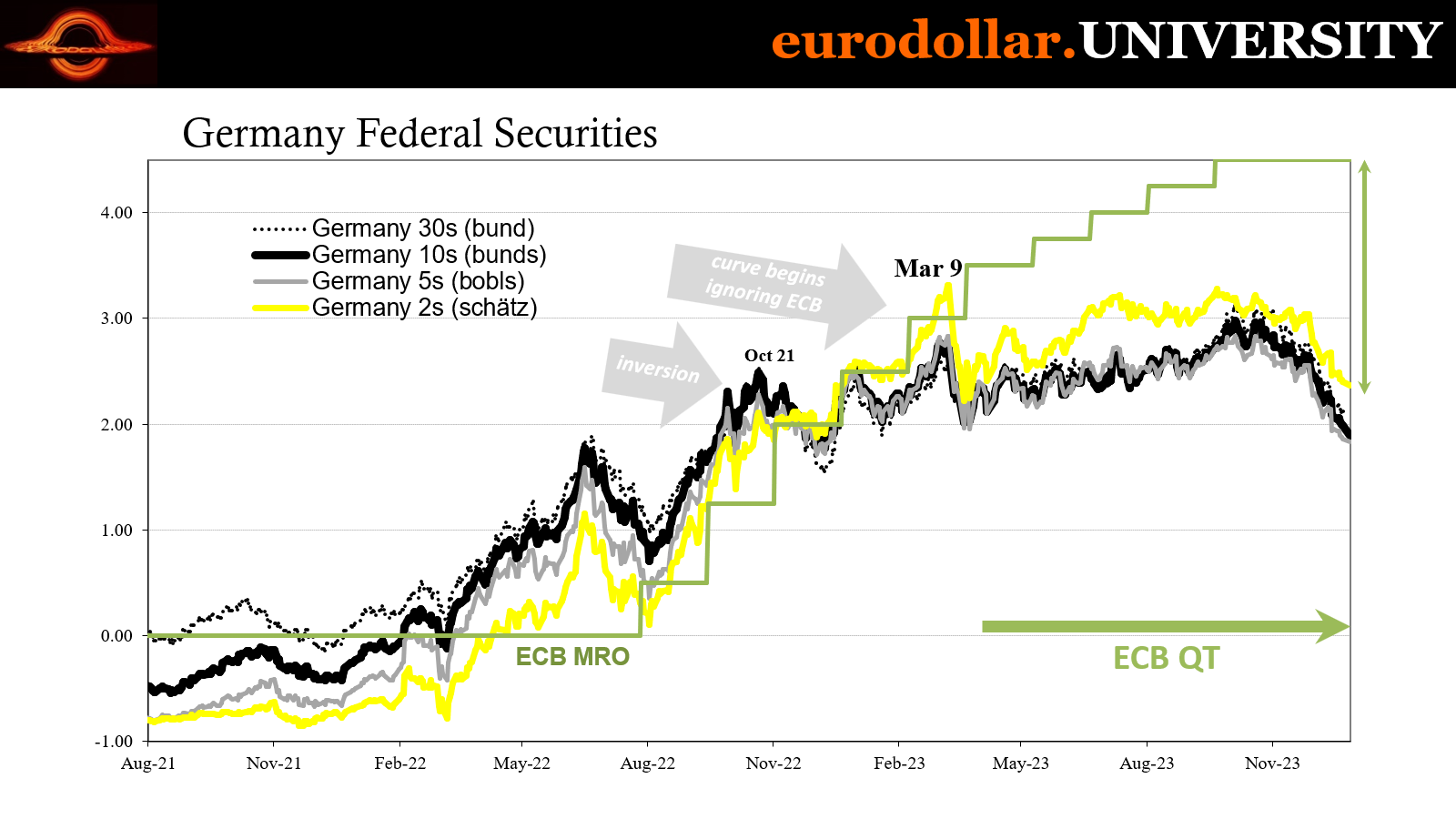

Yields right now aren’t just dropping, they are nosediving. USTs are getting all the attention, look at Germany and Europe. Bund rates are at more-than-year lows today, sinking farther and faster than anywhere. When you look at the circumstances, that almost seems insane – the ECB has steadfastly denied rate cuts and European yields are already way below current and future cuts when the European central bankers finally give up and follow the market.

EurIBOR futures are on a eyepopping rampage, too, alongside cash markets. The forward rate curve for euros has absolutely plunged here. That isn’t because Europe has been stuck in a shallow recession for about a year which might, perhaps get a little worse. Combined with bond market rates, forward money rates are telling us something that maybe Europe is where that next forecast stage starts from.

Does that mean Deutsche Bank fails? Maybe, the inversions don’t preclude something like that, but it doesn’t have to in order to produce the results which would get interest rates in Europe and everywhere else back down again.

See, that’s the proper way to frame all this – and I’m as guilty as anyone for not strictly enough adhering to that proper framework.

In my view, I see a deflationary recession (which, again, does not necessarily mean something like the Great “Recession”, there is an entire range of possibilities here, too) as the natural consequence of the initial supply shock cycle. One of those coming at the end would absolutely fulfill the curve “destiny” from its inverted inception, as it would fully destroy “inflation” and then neatly (though destructively) reset future expectations for growth along with it back closer to 2010s conditions.

To me, that’s more than bad enough; a silent macro serial killer no one knows is operating so close by is far worse than a single slasher economic “murder” that has everyone talking.

Everything that has happened thus far lines up in that direction, too, but that isn’t the only possibility. Curve inversions, swaps, the whole gang have already claimed Great Inflation 2.0, China Reopening, Europe’s minimal expansion, and now higher-for-longer. All they’re saying right now with exploding inversions is this list of “victims” is still incomplete; there’s very little chance this thing is done.

What else has to go on it to fulfill the full range of increasing inversions? That much we can’t yet say. I have some ideas and I’m more than willing to share them. However we ultimately get back to the 2010s from 2021 isn’t clear, but the probability that’s where the world is heading has left little other alternative despite the lack of Lehman.

Claiming these market signals are useless trivia is completely missing the point, disingenuously holding them to an unreasonable standard they’ve never once claimed. As the “bodies” continue to pile up, though, that is what ultimately matters and this stuff does indeed help us find and identify them whether anyone else notices or not.