A NEW GRESHAM FOR OLD MONEY

EDU DDA Dec. 27, 2024

Summary: There will not be a BRICS currency. And that’s first assuming any of its members want one (spoiler: they don’t). Contrary to every mainstream belief, money is not a government matter. It is instead driven entirely by commercial, free market interests. We have centuries of development and evolution which stand as an unchallenged testament. The whole thing comes down to one single factor, a modern “Gresham’s Law” which explains the entire way the world, not just the monetary world, really works - has for centuries.

BITCOIN HASN’T DONE WHAT ITS FOUNDER SET OUT FOR IT. WHY NOT?

The very idea of a BRICS common currency is a nonstarter. China and India may have settled their latest border dispute, though how long it stays settled is quite another matter. The two countries are bitter adversaries so neither of them are going to rush headlong into a full-blown monetary marriage. Or even partway to one.

Even if they were willing, that’s not the key element anyway.

THIS IS EXACTLY WHAT I’VE BEEN WRITING FOR YEARS. BRICS AREN’T REPLACING EURODOLLARS, THEY’RE TRYING TO WORK AROND ITS SCARCITY AND INSTABILITY. IF THE EURODOLLAR IS THIS BAD, WHY ISN’T ANYTHING CLOSE TO REPLACING IT?

There is this notion that money is driven by governments. It is exceptionally difficult to get people to realize this if only because the world has been conditioned to believe money like economy solely derive from whichever bureaucracy seated within the closest capital; just the way the bureaucrats and politicians want it.

Just general economic matters, too. Recession question? Time to get out the “stimulus.”

In that respect, the entire global public has been conditioned like Pavlov’s poor canine. Anything that goes wrong, and a fair amount which goes right, immediately gets thrown into the public lap. The real truth is that everything gets done in this modern age via private means.

Money, first and foremost.

Not only do governments prefer to pretend they’re in the center, most of their critics have had to put them there, too, not helping their own cause. Whether Bitcoin or gold proponents, both have vilified authorities which they have to in order to have any chance. Governments, they claim, are responsible for the demise of store of value money, commodity money in the case of gold.

They’re stuck making the claim governments have forbidden commodity, store of value money as an option. This isn’t true but you can see why they have to make that claim. Otherwise they’d have to admit the free market world freely chose not to adopt either one. It puts quite a dent in the argument each one makes about them being superior.

So, why aren’t those?

I only got to briefly address this error, sometimes made intentionally, in my debate with Dan Oliver over the gold standard (if you haven’t seen it, the full hourlong debate is right now available to DDA subscribers in the “Conversations” section of the DDA site). The free market chose the current form of global money without either the knowledge or the consent of any bureaucrat or politicians.

Twice!

GOVERNMENTS HAVE NO IDEA WHEN IT COMES TO MONEY, ESPECIALLY MONETARY INNOVATION. ALWAYS THE LAST TO FIND OUT.

The money we all use, the entire world, was created and maintained with few or any of them being the wiser. Ultimately, it came down to commercial needs which actually means regular people. Businesses chose the form of currency most advantageous to their customers, as banks did the same for those businesses.

We might think of deposit money as uncontroversial, yet as it was being adopted as the pre-eminent form of currency the vast majority of officialdom refused to recognize it as such. Of the few who might have, they were left confused as to why it seemed to proliferate so quickly and spread so far.

Deposit money, or fractional reserves, is actually nothing more than ledger money. The reserve isn’t really needed since the ledger acts as a form of settlement all its own (it took a while for this to catch on). Quite naturally, the ledger is more mobile, elastic and in every way a more elegant solution to the needs of an increasingly complex economic and financial framework. In primitive economic systems, where trade and exchange isn’t preeminent, cumbersome store of value forms of money can dominate (like gold) since exchange is a secondary matter.

Moreover, distance isn’t likely to be much consideration, either.

As economic systems became more specialized, however, and trade grew to be a significant part, money couldn’t remain static without hindering that development. In fact, this was the chief reason the world moved away from gold.

Banks as we know them arose as a solution to that problem. Contrary to popular belief, what made a bank a bank was not its storage capacities. The vault was incidental. Merchants who had no interest or monetary capability had long developed storage for valuables under a simple bailment. If you were only interested in keep some coins safe, you took them down to the local goldsmith.

Should you need monetary services, that’s where a real bank comes in. Initially that was limited to exchanging forms of commodity money, gold or silver coins from all over the place. That service, primitive as it was, actually made inelastic and static money more mobile therefore more useful. Money changers were an important development in creating flowing currency.

If a merchant/trader had a way to easily convert a coin from the princedom on the other side of the mountain into anything, that coin would be more useful even if it belonged to, and was official tender, somewhere else.

This made trading across wider distances more efficient and cost effective. The ledger format took it a step or two further, adding an intermediation function to the bank and further distinguishing it from a simple vault operator and caretaker.

To engage in truly specialized commerce required speed of settlement. This part needs no explanation, merely making people aware of what they’ve done their entire lives without thinking about it. Imagine having only physical forms of payment today, having to find a way to ship silver coins to China via when buying something off Amazon.com. There’s no way to make that work even nowadays with all the technology at our disposal.

Instead, there is a series of ledgers which do all that work. You have a “bank”, as does the Chinese producer and the Amazon merchant. All you or the merchant really needs to do is make sure the banks involved are connected to each other, then how or when monetary settlement takes place is entirely up to them. They all balance on book entries with no need to ship anything anywhere – apart from whatever it is you bought which now can become instantly available since ledger money settles at the speed of light (or would, if legacy parts of the system would update and further modernize).

It may seem farfetched, that’s exactly what happened in the 19th century. Banks began to develop a surprisingly sophisticated and complex network (correspondent banking) of telecommunications as far back as the early 1800s. You could deposit coins or specie with one member of that network and then be able to use the funds anywhere in it by writing a check.

When doing so, the banks in between figured out how among them – no central bank or agent necessary – to settle the movement of money. In most cases, it was another book entry or series of them, meaning a single piece of commodity money didn’t need to physically move in order to be used anywhere else within the coverage.

You deposited something at one end and then claims on the something were exchanged several times before ultimately reaching the seller of the good or provider of the service, who was given a claim on something else within the banking system – a paper deposit.

This was in every way real money, even if the government didn’t think so. The free market increasingly chose ledger money for all its benefits in mobility and speed of settlement. Money had become mobile, and that’s what the commercial system has prioritized (for better and worse).

Throughout the 19th century, this ledger form (and check writing as the key tool) grew to dominate. While bureaucrats and politicians focused their entire limited efforts on gold and physical bank notes (which had to be produced by the Treasury Department and only upon deposit of Treasury bonds, often borrowed, by the way), the commercial system in America and elsewhere instead turned to another format of money anyway.

This had not only puzzled them, to this day there are Economists (who are generally terrible at money) who can’t figure out why. By their reckoning and those of contemporary sources, it would have been profitable to locate Treasury bonds and have physical currency printed up for customer use. Profitable for the bank, perhaps, not the demand by the bank’s customers.

Banks followed commercial demands.

Those, not DC or JP Morgan, dictated the money format. Even as early as the turn of the 20th century, ledger money had taken over. Hand to hand payment was well on its way to being rendered a triviality as the 1900s began. Only then did the politicians finally come to realize money had evolved and changed without their “permission”, or even being fully aware it had.

When FDR finally gave up on gold, while still a “crime” its effect on the commercial system was minimal. Gold wasn’t in use as a medium for decades by then (it’s entirely a different matter where it came to peoples’ savings, which is beyond our scope here for what really made Executive Order 6102 a crime, not as the money in use). Ledger money had already fully taken over, to the point today no one even gives it a second thought.

What’s even more astonishing is that the commercial system then did it all again. Yes, twice. This time making even greater evolutionary leaps. Ledger money got extended into the eurodollar via two extraordinary developments, neither of them with the knowledge of any government let alone some kind of input or approval.

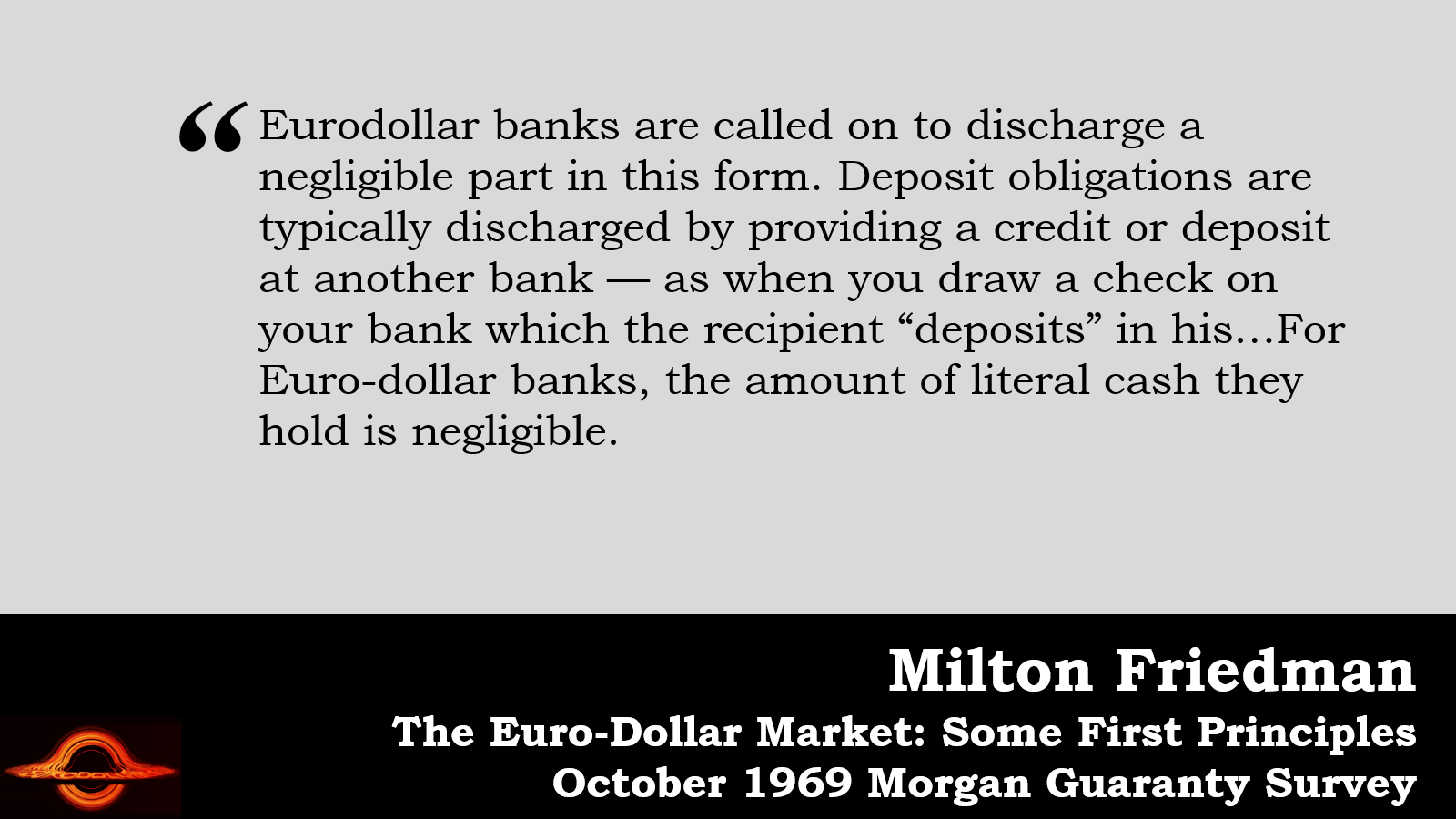

First, the reserves part of fractional reserves was removed entirely. As Milton Friedman had tried (in vain) to explain in 1969, there are no Federal Reserve notes here. No gold. Nothing physical anywhere. Where he erred was in not realizing banks had gone even further than that; this was a fractional reserve system with zero reserves, entirely ledger based.

The easiest way to think about it is with a thought experiment. A bank outside the US claims it has accumulated a bunch of physical dollars. If it has a topnotch reputation, who’s to say it doesn’t. The bank can therefore lend them to other overseas banks and individuals who need them since they are the only way to do business outside of home countries.

Rather than have to ship pallets of cash around Europe or to Asia, this bank simply keeps track of who owes what to whom, and therefore who owes what on its books. It has simply created claims on its pile of dollars and the transferred those claims throughout the rest of the world.

Those claims technically mean the person holding the claim has a right to literally claim the actual dollars the bank claims in its possession, but, with usefulness as the priority, no one ever days. The free market world offshore freely chooses the ledger claims because they are demonstrably more useful.

As a result, any physical cash which may have been in the system nearer to the start simply disappears since no one in this eurodollar system had or has any need or use for it. Technically these “dollars” weren’t dollars, instead claims on reserves of dollars that didn’t exist – fictive currency or ghost money.

You’ll notice this removes the government, too, apart from one another’s ability to regulate bank books. And by moving those books offshore, there was even less of that.

This was the second major innovation, taking this pure reserve-less ledger money and having it transcend physical space and boundaries. Government-drawn borders no longer mattered. Commercial agents within them were conducting business with this eurodollar world with or without permission, and banks inside the eurodollar were advancing those commercial (and eventually financial) interests.

It was the customers who drove adoption and therefore acceptance. As with the first stage of ledger money evolution, by the time any government caught on, let alone those in the US government or the Federal Reserve (which was properly treated as a joke back then), this eurodollar had already come to dominate the entire world. And what parts it hadn’t from the earliest days, it eventually would because by then it didn’t matter what authorities had to say this is the way the world worked and there was no going back.

This is a corollary, of sorts, to Gresham’s Law, the one which has never been communicated before. Even the few who realize what’s taken place, I don’t get the sense they fully grasp what has truly happened, either. In many ways, it replaces Gresham or at the very least updates it to make it appropriate given the modern settings.

Overriding every other concern in this lengthy process of monetary evolution is usefulness. It isn’t really that commodity money or store of value money came to be disliked, those formats simply weren’t mobile nor efficient. Settlement doesn’t match current needs.

Sir Thomas Gresham said that bad money drives out good, meaning that people will naturally spend and use “bad” money that is overvalued or loosely valued while hoarding “good” money that is properly valued or generally more stable.

The ledger or eurodollar corollary is that useful money drives out less useful forms, flipping Gresham around entirely. While the good Sir was thinking strictly about commodity money, this goes beyond that limitation and, in fact, obliterates it.

In other words, the free market commercial system chose more mobile and efficient monetary formats and because it did other forms of money essentially disappeared or were limited to very special cases existing only around the margins of the system. Gold was gone from commerce long before FDR, and in foreign exchange because of the eurodollar way before Nixon in August 1971. Bitcoin has had sixteen years to catch on and never has (whereas in sixteen years the eurodollar went from nothing to that closing of the gold window having took over the whole world by then).

This, then, finishes what we started, updating Gresham. The more useful form of money will replace the less useful form and it will do so with or without any government involvement. Decisions will be made from the bottom up dictated by commercial needs and directed by the private free market.

IT WAS LATER CLARIFIED AS A TROLL, AND NOT AN EFFECTIVE ONE.

It isn’t, nor will it ever be, up to China or India to “design” a competing alternative to the current eurodollar. If anything, this version of Gresham is exactly why no one has. They can’t drive out the eurodollar without first making something more useful which, let’s be honest, is the last thing any government is capable of doing let alone the ones in India and China (forget Russia).

This is the threshold any aspiring reserve currency must meet, and demonstrate it in the commercial (and financial) space first and foremost. No politicians required.

Of course, we have to define what it means to be “useful”, though I do think a fair amount is self-evident given how ledger money has evolved and why – mobility, elasticity, efficiency being paramount. I’ll save the more complete conversation on “useful” for some other time.

New Gresham’s Law (needs a better name) explains why Bitcoin or gold are relegated to the outer edges of the monetary world. Neither can meet this standard. BTC has become a NASDAQ stock increasingly dependent on who holds the coins not how they might or even can circulate, whether Wall Street or, shudder, now the federal government itself! This is why sixteen years of Bitcoin and it only has its price to show for anything.

Gold in physical form is likewise an investment, both of them being stores of value and, yes, even good ones, but they are not successors. They are competing with stock markets and financial products, not the eurodollar.

No one in Delhi, Beijing, or Washington will decide where money goes from here. There is no BRICS currency, nor will there be one. Even the BRICS “banknote” Vlad Putin was gladly showing off for the cameras a couple months ago was, whether he knew it or not, a perfect illustration of New Gresham.

The thing was totally useless - even as a troll attempt.