MR. BULLARD WOULD LIKE A CURVE WORD

EDU DDA Mar. 4, 2025

Summary: More volatility in markets, including stocks. Bond yields were down sharply, before turned around on tariff news. Target added to the negatives with several warnings, the first of which further verified the growing “growth scare.” With market interest rates already down sharply, attention turns to the short end. Forward rate markets are beginning to creep toward a sooner Fed rate cut trigger, with one key contract crossing its threshold. The history of the Fed with the yield curve sets out the dynamic, one that has been kept from the public.

DURING 2019’s RATE CYCLE, FORMER ST. LOUIS FED PRESIDENT JAMES BULLARD WAS A VOICE OF REASON.

Everything dropped to start the day as the combination of tariffs and the “growth scare” spooked all kinds of financial markets, building from the wave of “volatility” cresting over the last three weeks. Stocks continued to sell off, bringing the NASDAQ right to the edge of psychological “correction.” Treasury yields sank sharply, pushing the 2s all the way to 3.88% and the 10s to 4.11% at one point. SOFR futures (the primary subject of today’s DDA) were bid as the moment of truth for the Fed’s interest rate policy is being dragged closer to the present.

It also didn’t help the economic data – here in the form of retailer reports – was equally dour and intertwined with these major topics. Target warned; Best Buy warned; both promised they’d have to raise prices.

Then, toward the end trading, there was news from the Trump administration that maybe deals could be done to avert tariffs which unwound a lot of the anxiety-induced extremes at least in bonds. Stocks took a different direction, after having clawed back much of their earlier losses then dropped like a stone into the close.

Volatility indeed, yet hardly unusual for these periods of high “uncertainty.”

Is it really uncertain? If anything, at least in the short run, the situation more broadly is gaining clarity rather than becoming muddier. The drop in rates is exactly what it seems to be, to the point even the mainstream media is unable to mistake the signal (if still presenting it as entirely due to expectations for what the Fed will decide). SOFR futures buying has moved considerably up the curve.

First, the macro. Lost amidst the tariff fury, what Target reported wasn’t necessarily about them, not at first. While the company’s CEO admitted the retailer is going to try to pass on as much of the increased input costs as it can, reading between the lines what he said was management isn’t really expecting to be very successful (not inflation!)

The company sees comparable sales being little changed in 2025, below the average analyst estimate, while net sales are expected to climb around 1%. Target also warned of “meaningful” pressure on profit in the coming months.

Higher prices to customers yet reduced revenue projections, to the point they are now flat again. The “meaningful” profit pressure is obvious, the higher costs of obtaining goods from overseas that Target will simply have to eat because it knows consumers won’t be able to fully pay higher prices. Demand is going to be negatively impacted no matter what.

However, it was what the CEO said before this which should have gotten more attention:

Target said February sales were soft as cold weather affected apparel sales and declining consumer sentiment affected nonessential categories. The company expects these trends to moderate, though it will remain “appropriately cautious” through the year.

“Cold weather” had allegedly tanked broad consumer spending in January, if you recall with retail sales, and then, according to Target, did it again for at least their shoppers in February. Not even Target really buys the excuse which is why the “appropriately cautious” was lawyerly thrown in afterward. This is more evidence how, even before any price impacts from trade duties, the consumer economy experienced a sustained and sharp loss of momentum which, according to Target, extended further into February.

That’s the “growth scare” showing up in yet another category, this time a significant corporate anecdote from the country’s third largest retailer. One who, until recently, had become more optimistic after booking a not-as-bad-as-feared holiday quarter and had expected the late year bounce to carry over into 2025.

It didn’t.

The “it didn’t part” broadly explains why interest rates have been moving lower since mid-January. First, rates were moving higher for other reasons than inflation and growth potential up until then, particularly in December and the first half of January (acute selling of Treasuries by foreign reserve managers in response to the severe dollar shortage).

What had held up the short end of the curve until recently (February 12) was the lack of clarity over the Federal Reserve’s potential interest rate policy stance. As we’re all entirely too acquainted with, Chair Powell and his crew have been back and forth repeatedly since 2023, forcing the marketplace to judge when consumer prices or economic weakness will be sufficient to convince the helpless FOMC policymakers to make moves in one direction or seemingly the other.

As it stands – or maybe stood before the last week – the Fed is firmly in the inflation camp. Don’t let the exterior posturing fool you; officials all declare that they have no bias yet it is deeply institutional even if unspoken. Its entire history since 1979 has been that, in the absence of clear and convincing macro weakness, policymakers always prefer to posture on the consumer price side of the mandate.

Even after the Great not-Recession unleashed (Silent Depression) an entire decade of thorough disinflation, Bernanke then Yellen and finally Powell spent most of their time from 2013 onward looking out for “inflation” driven by a labor market they were convinced was increasingly and inflation-arily tightening.

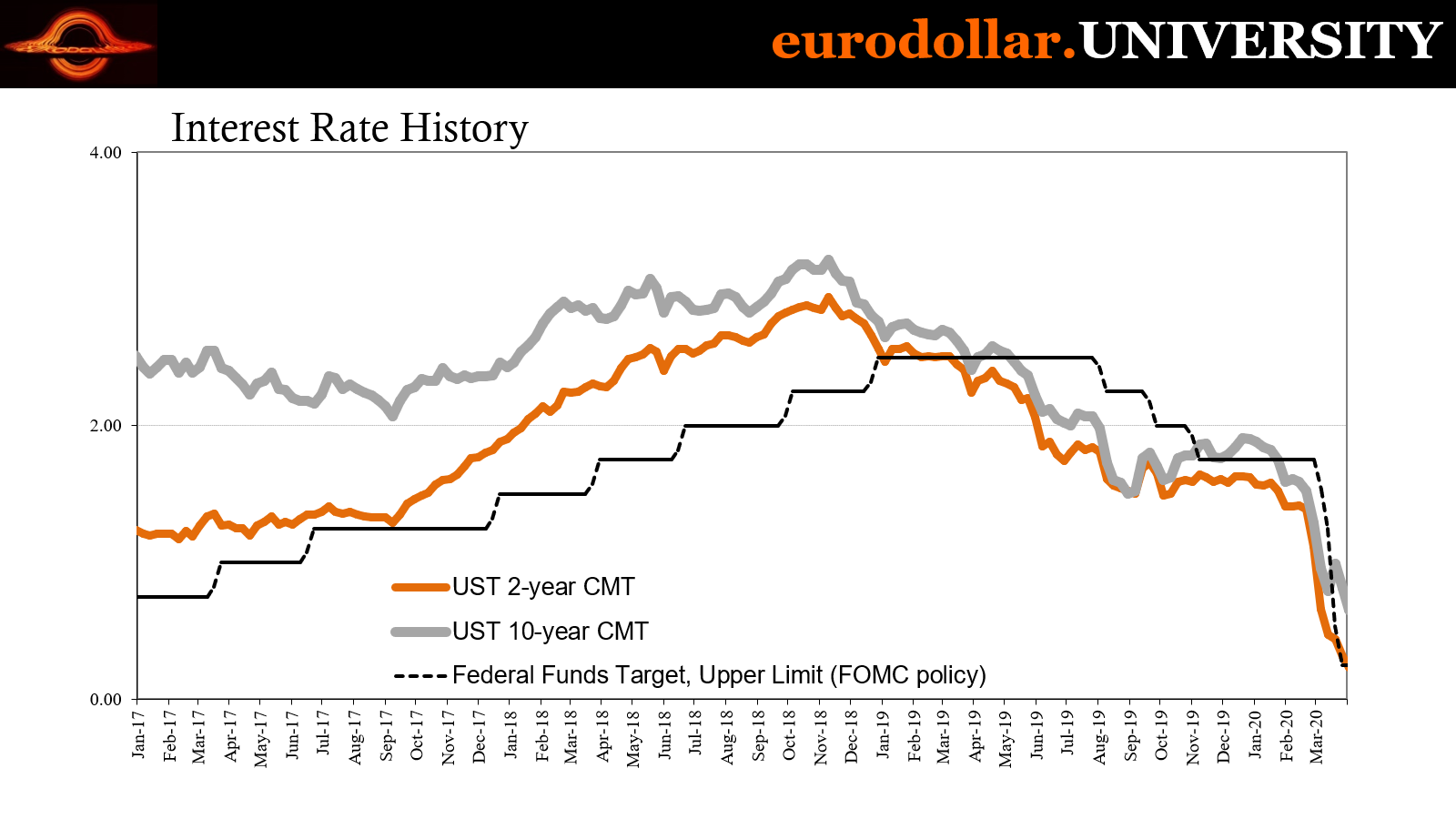

This is why policymakers pursued a higher rate policy in 2018 despite the growing evidence more strongly indicating both the absence of price pressures along with increasingly serious threats to the macroeconomy. Right at the top of that list was the curves.

Unlike how policymakers make it appear, the FOMC was not unaware of them; quite the contrary, where it came to the yield curve, anyway, there were repeated discussions about the flattening in it before the inversions in 2019. Their most vocal advocate, if you will, was former St. Louis Fed President James Bullard.

In April/May 2019, Bullard noted how it had earlier changed and twisted not in their favor:

MR. BULLARD. Yes. I would just say one other thing about the yield curve, and I guess Simon was saying this. At first, when we raised rates, the long rates went up one-for-one. But then, as you got further through the year, the yield curve got flatter and flatter, and it almost inverted, but not quite, and then pulled back a little bit later.

What’s really odd is that throughout these discussions in 2018 and 2019, while the yield curve did flatten dramatically, it didn’t invert in any part until late in December and not more completely until the middle of the following year. Yet, the eurodollar futures curve had, from June 2018 onward. It didn’t merit a single mention – NOT ONE! – in any of the meetings from then to COVID.

Such is the legacy, I guess, of Bill Dudley and his regrettable experience with them and the curve from back in 2006 and 2007.

As far as the Treasury curve was concerned, though the discussions weren’t all that extensive and officials failed to follow through with most of them until the rate cuts in 2019, Bullard had made an effort to make sure the FOMC was at least aware of its various twists and signals. As far back as December 2018, when committee members had voted for what would be their final rate hike, Bullard was at his strongest:

MR. BULLARD. In my opinion, previous Committees and staffs have soft-pedaled this important market signal. I would cite as an example former Chairman Bernanke, who gave a speech downplaying yield-curve inversion then, beginning in March 2006 in a speech delivered at the beginning of his tenure.

The Committee’s track record on this issue is not good. I think we are a little bit tone deaf on this issue. The base case that I would like the Committee to keep in mind is the mid1990s: The Committee normalized rates in 1994 and ’95 but stopped short before the yield curve inverted. The yield curve had a positive slope through the late 1990s—one of the best periods of performance in postwar U.S. macroeconomic history. The yield curve finally did invert in the year 2000, and the economy went into recession a year later. [emphasis added]

That last part may have been – and might still be – the most important one. People normally equate anything about the yield curve with recession, and, to be perfectly clear, the traditional postwar variety, the V-shaped temporary dive and recovery. What Bullard had pointed out was that the moderately positive slope occurring at a relatively high (compared to 2008 and after) nominal level of the late nineties signified some of the best circumstances the country had ever seen.

It isn’t just recession equals inversion, positively sloped matters just as much.

They were at their peril ignoring inversion yet just as importantly taking little from the flattening in the curve leading up to then, as Bullard went on to remind them a few meetings later as his caution was increasingly proving prescient. Growth prospects had deteriorated along with the flattening and inversion.

The common counterargument to the yield curve like the one from forward rates (now term-SOFR futures) is that the US economy has been able to avoid a recession unlike previous instances (2019-20 remains unsettled since we’ll never know for sure how it would have turned out). While technically true, it again misses the point, Bullard’s point.

Having been inverted the entire time since 2022, with eurodollar futures inverted since late 2021 before handing over to SOFR futures in the middle of 2023, it was the near inverse from the curve shape of the late nineties; the one which was moderately upward sloping at relatively medium nominal levels.

Inverted at historically low rates (even after the Fed’s “historic” rate hiking) had meant the other end of the spectrum from the stable, legitimately strong period decades ago. These 2020s inverted curves were reflecting first the forgot how to grow economy, one that is increasingly in danger of going from forgot how to grow to remember how to (typical) recession.

Where Bullard’s soft crusade applies in 2025 is the “reaction function” policymakers might have toward weakness reflected on the yield curve as much as in the data they claim to depend on. They know the curve’s condition and even know what it means, no matter how much they might pretend otherwise or more often publicly plead ignorance.

With the yield curve, anyway, re-inverting over the past week as LT rates have declined significantly, in many ways the current FOMC is confronting comparable conditions therefore interpretations and choices as in 2019 – not to mention the similarities with “trade wars” and the potential fallout from them (as discussed here). After all the posturing and downplaying, as it would turn out the FOMC did indeed heed what yields and forward rates were advising.

It was, believe it or not, noted current hawk Raphael Bostic who said in July 2019, the meeting when the Fed started to cut, “This is the last point that President Rosengren raised. If we are convinced that the inverted yield curve is telling us we are north of neutral, then we should take actions to get back to neutral as quickly and as boldly as possible.”

Not quite boldly, yet the committee did act several times more afterward, too.

What many today are wondering is how much and how quickly the current Fed might follow that earlier path. The complication here is obviously consumer prices which policymakers in their distorted and often incomprehensible worldview are even more biased in favor of. Even so, there is a level of weakness in the macro arena that does override the bias.

We saw it last summer and there are growing similarities now to then.

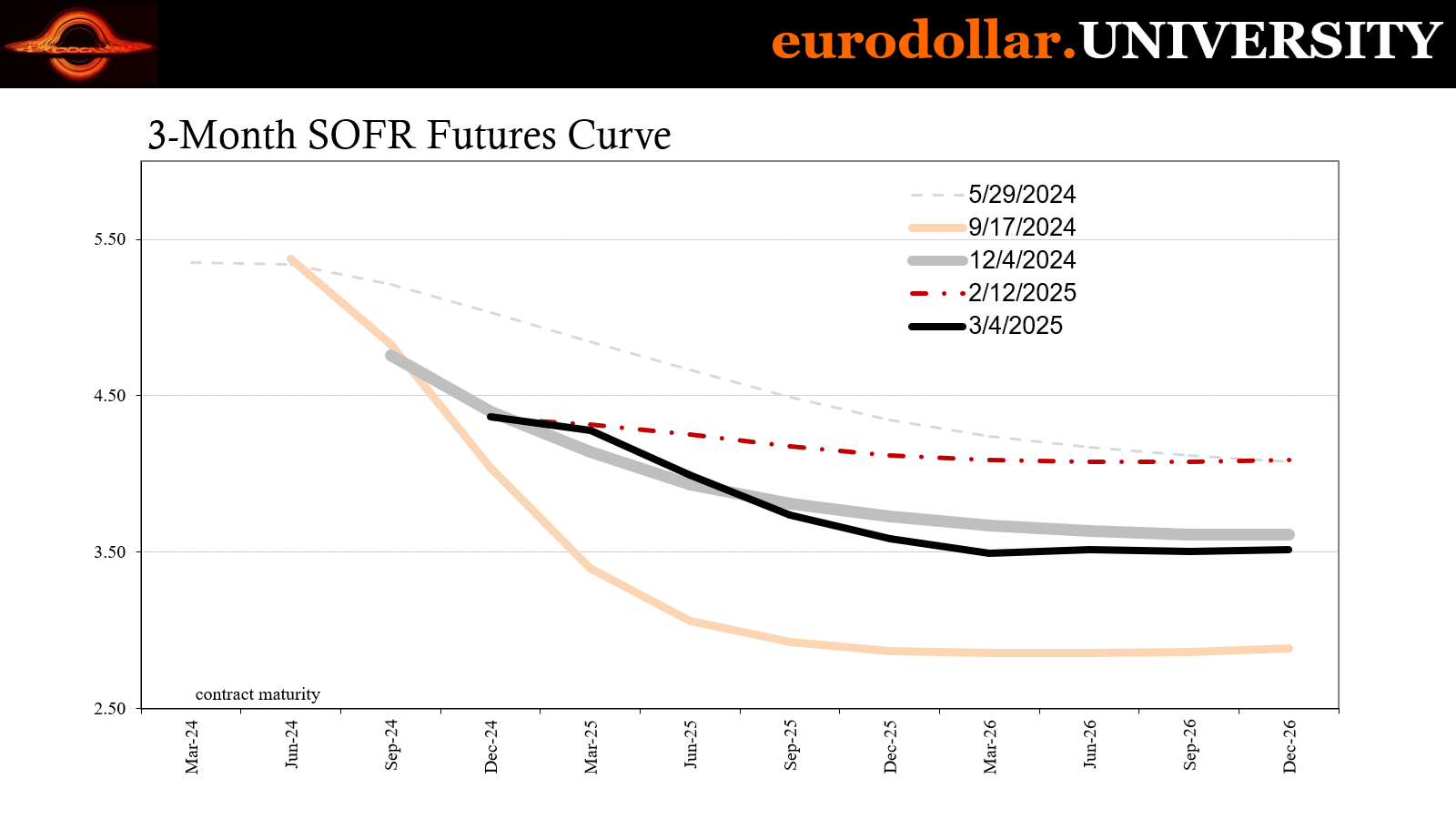

Another signal comes from forward rate markets like term-SOFR. I wrote here that one would be when contract prices finally break out of the range they’ve been limited to since November. For the December 2025 contract, that was around 96.30 and, for closer contracts like June 2025, around 96.15 if not 96.20.

Over the past few trading sessions, the December 2025 broke out whereas the Junes still have a little way to go.

In fact, the rate cutting impulse judged from the term-SOFR futures market has crept noticeably and more forcefully again from the back of the curve toward the front. What that means is the market sees a higher and growing probability the current weakness in the macroeconomy (primarily the labor market) becomes substantial enough and then is sustained (or appears likely it will be) to reorient the FOMC back into rate cutting.

Same as last summer and the middle of 2019.

The fact it isn’t all the way forward to June and closer simply means there isn’t enough on the table right now that is expected to move the next rate cut into the second quarter. That’s the same with the inversion in the 3m10s Treasury spread, both market segments pricing the Fed to be slow to react to flagging conditions not unlike last year and six years ago.

The breakout of the December 2025s and later contracts is a significant threshold either way. Like what Target said and a whole host of data has shown recently, the deterioration is substantial nonetheless. Even policymakers themselves know their own history is against them and with markets.

In public, they disown market yields and spreads. In private, they worry a lot about being on the wrong side of them. In 2025, the next rate cuts may be a lot closer than you’d think.