Daily Briefing 3/13/25

Car Exports-Production/Industrial Production (INEGI)

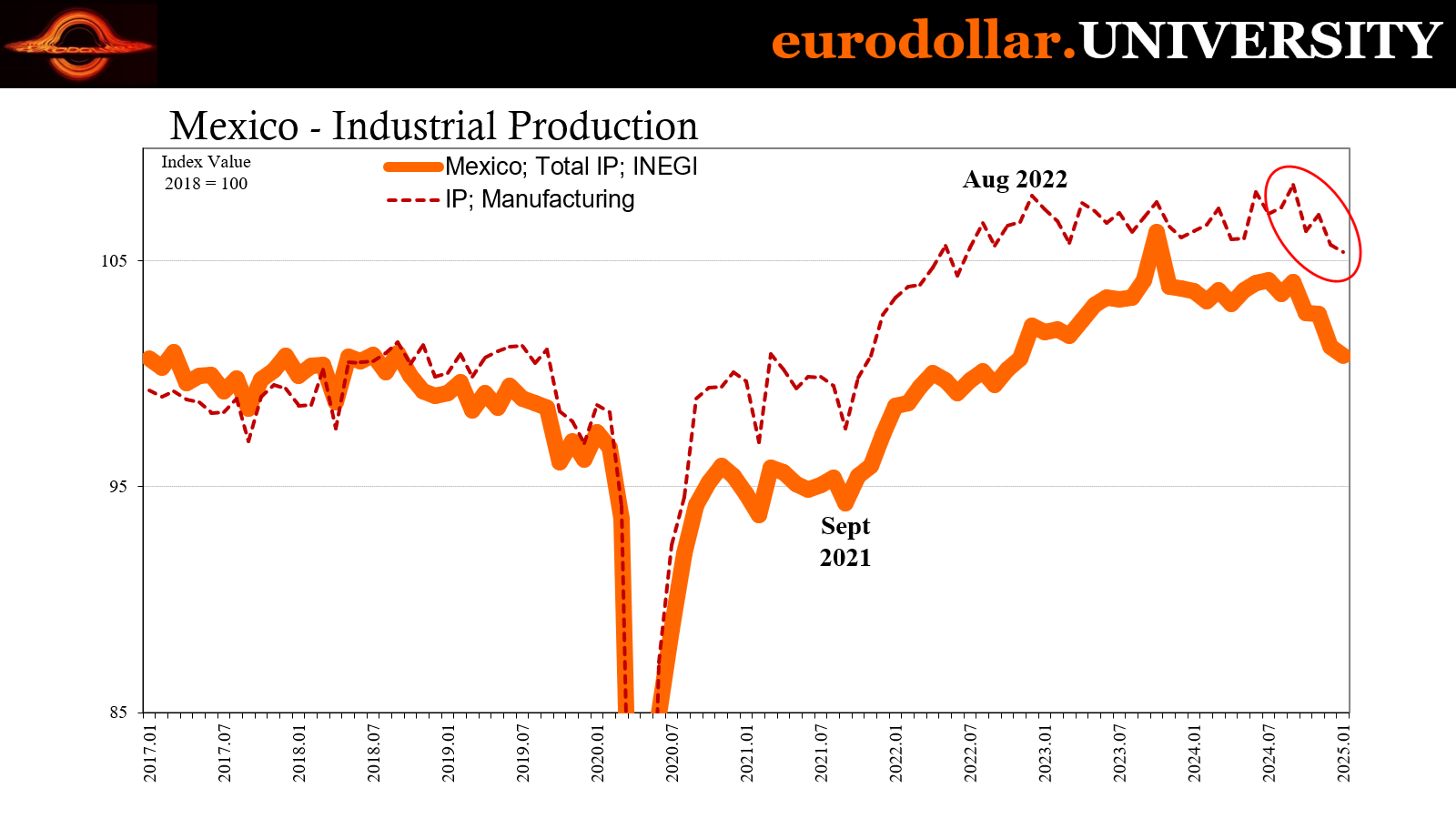

Mexico's light vehicle exports declined by 9.2% year-over-year in February 2025, totaling 258,952 units, following a 14% drop in January. The main driver of the downturn is weakening US demand. Additionally, uncertainty surrounding potential 25% US tariffs on Mexican goods has led some automakers to pause shipments while awaiting trade clarifications under the USMCA agreement. Production also declined slightly by 0.8% year-over-year to 317,178 units, though domestic sales increased by 3% to 117,678 vehicles. Meanwhile, Mexico's broader industrial production (IP) continued to weaken in January 2025, declining 0.4% month-over-month and 2.8% year-over-year. Mining and manufacturing led the downturn, with Pemex’s struggles contributing to an 8.6% contraction in the mining sector. Construction saw a marginal 0.1% monthly increase but remained in decline on an annual basis.

Interpretation

The continued contraction in Mexico’s auto exports and broader industrial production reflects a clear cyclical downturn in the country’s manufacturing sector, driven by both global economic conditions and trade uncertainties. The February data confirms a trend of declining auto exports, which is unsurprising given weakening consumer demand in the US and persistent trade tensions.

The uncertainty that has gripped small businesses, expectations regarding future economic conditions, and the relative decline in consumer incomes in the US are all putting pressure on consumer spending and reducing demand for new vehicles. With over 80% of Mexican auto exports destined for the US, this drop in demand has directly impacted production and shipments.

However, the slowdown is not solely a demand-driven issue - policy uncertainty is also playing a role. The threat of a 25% tariff on Mexican auto exports, even if delayed, has already begun to disrupt trade flows. Some automakers have temporarily halted shipments while determining whether their products meet USMCA’s zero-tariff criteria. This front-loading effect - where firms rushed exports ahead of potential tariffs - may have amplified the decline now, with further downside risks if tariffs are ultimately imposed.

The weakness in Mexico’s auto sector is also feeding into the broader industrial slowdown. January’s industrial production data showed a 2.8% year-over-year decline, led by contractions in mining (-8.6%) and manufacturing (-0.9%). The struggles of Pemex, which is increasingly showing signs of distress similar to Venezuela’s state oil sector, are weighing heavily on the mining sector. While construction saw a slight monthly increase, this appears to be a short-term fluctuation rather than a sustained recovery, particularly given the sector’s overall negative annual performance.

The February data will likely reflect further deterioration, as the auto sector’s production decline feeds even further into industrial production figures. This confirms a cyclical slowdown in Mexican industry, which is not just a result of trade tensions but also a broader reflection of global economic conditions. With demand cooling in the US and uncertainty persisting around tariffs, Mexico’s industrial sector and therefore its overall economy faces increasing headwinds in the coming months.