WHAT DOESN’T HAPPEN CAN KILL (ECONOMY)

EDU DDA Dec. 3, 2024

Summary: It’s not just that JOLTS hiring was weak again, very nearly matching June’s shocking low, the consequences of that are piling up again in all-too familiar ways. The reason why the economy never recovered from 2008 was the lack of hiring following the crisis. We had already seen that once before in the 21st century, following the dot-com recession. The hiring rate here in 2024 is already worse than that time, around the same as coming out of the 2010s.

Hiring in the month of October tumbled yet again. The dismal result from JOLTS was immediately dismissed as the work of Helene and Milton. On the contrary, hiring fell sharply back in June and though the rate improved from there it didn’t shift the trend. In other words, October’s low not far from June is the fourth in five months pointing to big trouble in employment.

Another datapoint on a growing list, joining incomes, the unemployment rate and even participation.

It was the lack of hiring which had doomed the post-2008 recovery, itself a byproduct of monetary disarray. Too many businesses had found themselves in real liquidity trouble as the crisis unfolded, unable to raise cash just for basic working capital needs like meeting payrolls. Banks slammed shut, choking off emergency credit lines, plus even commercial paper, a key conduit for short-term working capital, basically stopped functioning.

You might recall the Federal Reserve inventing yet another “tool” with non-financial CP specifically in mind, something called the Commercial Paper Funding Facility introduced on October 7, 2008. Its purpose was to work with primary dealers to get the CP market moving again so business all over the economy wouldn’t have to resort to mass firings as a means to manage their cash position.

Which, of course, they did anyway, one of the most ultimately damaging failures which stands out amidst an entire ocean of them from that period. For one thing, the program immediately attracted investment firms (asset-backed issuers, mainly) who weren’t affected by the meltdown in CP – in the same way the BTFP late in 2023 created an “unanticipated” arbitrage for banks which hadn’t been impacted at all by last year’s bank crisis.

It might all seem like irrelevant details, but they matter in the respect survivors look at their liquidity profile very differently from having experienced the breakdown, and closely observing what was supposed to have been an effective, technically proficient central bank basically just winging it, making stuff up on the fly always behind events, often putting little forethought into what they were doing or what was happening and betraying a stunning lack of competence in the process.

JOLTS hires provide some of the most damning evidence that bridges the gap between monetary panic and permanent economic damage. Hires understandably fell off a cliff in the middle of 2008, even before the worst of the crisis, and then failed to recover for more than half a decade; that crucial period which sealed the fate of maybe the entire world.

No amount of QE could convince employers to re-hire the millions they previously let go, managers like markets simply no longer trusted the monetary environment nor the central bank allegedly watching over it. If anything, the fakeness of QE and its only appeal via sentiment further cemented the distrust especially via the repeated monetary/liquidity setbacks of the time reminding the real economy of their previous danger.

Businesses would instead overmanage their costs and cash profiles to the detriment of any chance for recovery, which predictably became a self-reinforcing process – the lack of hiring meant subdued spending which only rewarded the caution when recovery requires the opposite in the form of blatant risk-taking.

The real job of the central bank, at least as the modern version of a central bank sees it for itself, is to buoy sentiment in order to break that feedback loop. QE was supposed to reassure employers there was no more risk in money or real economy, therefore they could confidently appeal to their “animal spirits” so as to restaff without inhibition.

Which they never did, as is all over the JOLTS data (hires).

That is why the participation rate fell so much and then devastatingly remained there year after year. People who were laid off during the downturn finding no jobs available on the upturn, naturally they exited the labor market entirely which has been criminally attributed to those very workers themselves. Economists have spent the last fifteen years defending QE by claiming those laid off were essentially defective (too lazy, too drug-addicted, and, for a time, too old).

JOLTS blows that idea completely out of the water. Companies weren’t hiring in the second half of 2009 into 2010 because they couldn’t find workers, there were plenty who had only been out of work for a short time. It wasn’t until 2014 that hiring finally started to pick up just enough the participation rate would finally level off later in 2015.

By then, it was far too late.

Why did it take until 2014? Because it took that long for the developed economies to finally achieve a settled enough state, as the Euro$ disease took aim at the developing world from there on. By then the damage was permanent, drug addiction had taken off as a result not as the reason.

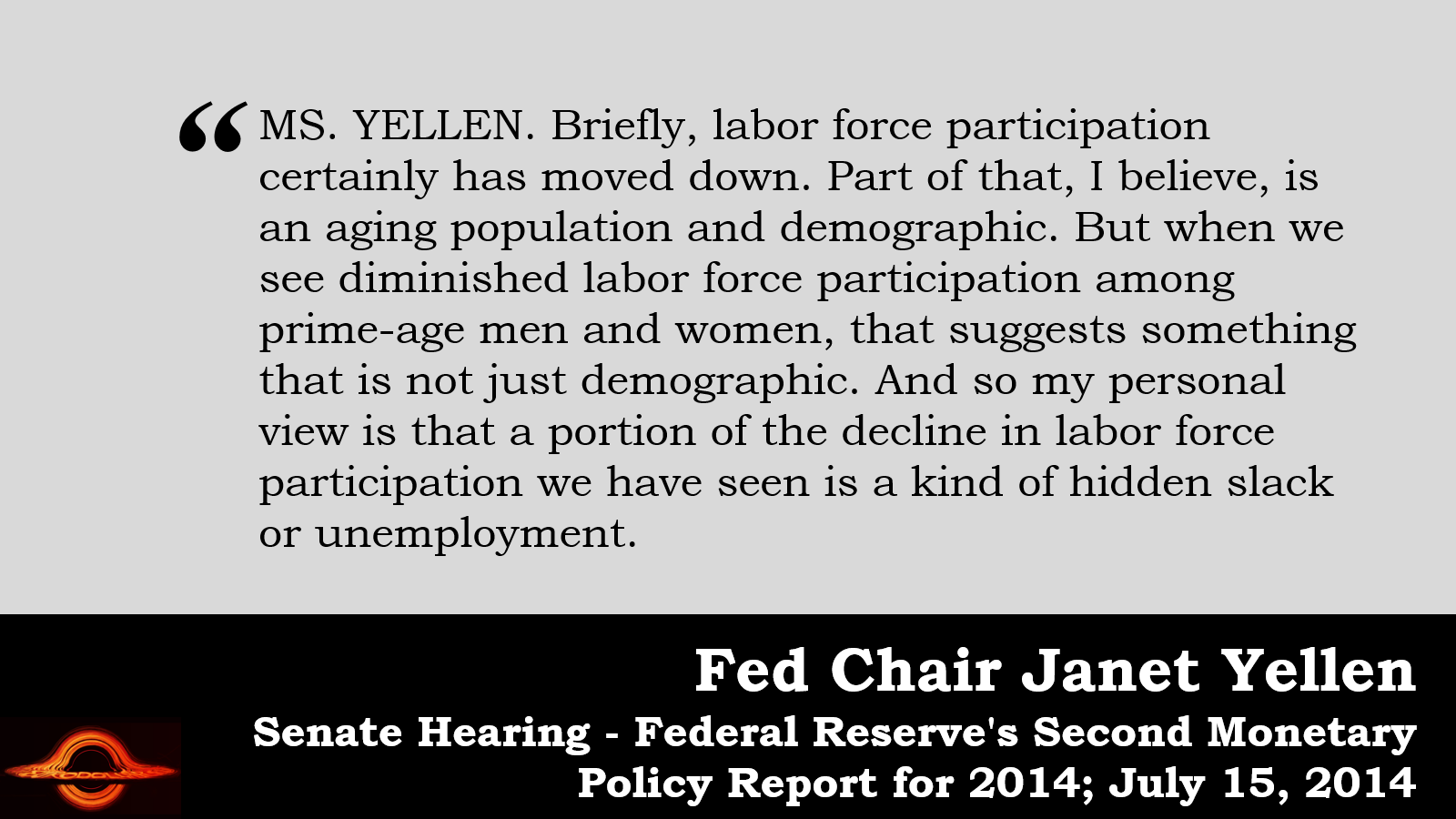

That’s why from 2016 forward policymakers kept forecasting an inflationary recovery, expecting it from a tight labor market that simply didn’t exist. The unemployment rate had dropped to low levels only due to the fact it no longer included all those millions who had themselves dropped out of the labor force years before – the very “hidden slack” Janet Yellen once admitted was responsible for so much holding “inflation” at bay plus the economy beside.

Whenever the labor market did pick up as it would during reflationary periods such as 2017, there were more than sufficient excess workers Economists had completely written off (see: R*) who would come back into the labor force however briefly.

The aftermath of the 2008 crisis wasn’t the only time in the 21st century the economy experienced this phenomenon, either. Following 2001’s otherwise mild dot-com recession, the appropriately-classified jobless recovery was marked by even worse hiring rates than during the recession itself.

This continued well into 2003 at the same time, once again, participation dipped (and, you’ll note, Alan Greenspan kept lowering rates until the middle of 2003 as a response to lack of hiring). In this instance, it wasn’t liquidity risk driving it, rather earnings. The dot-com bust had so depressed share prices corporate managers were desperate to make their pay back and so enacted Ross Perot’s Giant Sucking Sound, the easiest way to trim costs to boost bottom lines in a bid to get stock prices back up to where they’d been years before.

That wasn’t the only reason for the mid-2000s drop in the participation rate, of course, demographics played some role as they would again in the 2010s. That excuse has been overused and inappropriately applied in both cases when by far the bigger villain, if you will, is the lack of hiring during critical moments in the economic cycles.

While we focus our cyclical fears on layoffs and firing for good reasons, it really is hiring what should be at the top of the list. It is understandable why its absence goes unnoticed, since it is more difficult to sufficiently appreciate something that does not happen, hirings, in favor of the easier-to-identify therefore quantify events which do, firings.

As it now stands in late 2024, the hiring rate is roughly equal to 2014 at the same time having fallen well below the jobless recovery of the early 2000s, having already been this way for months. And as hiring has downshifted over the last year, going back to last September, what has happened to labor participation? It has dipped all over again despite so many reassurances the labor market remains healthy and resilient.

We’re seeing some of the worst aspects of past labor markets emerge when so much of the public has been hoodwinked into believing the opposite.

This hidden slack is once more the byproduct of the hiring side which central bankers continue to be biased to ignore, yet workers/consumers simply cannot. Everyone is waiting for layoffs when the dirty work, pun intended, is already being done – much of it has been done – in the near-total shutdown of hiring. Being in the same vicinity of the early 2010s is a huge warning, all the more given the “suddenly” lowering participation rate.

And on its opposite side, we have to likewise consider why companies are choosing this path. If the economy is improving or even just steadying, we see anything like this in JOLTS. The primary driving force this time around is the price illusion of the supply shock, the difference between nominal and real.

In other words, with so many businesses buying into the hype of 2021 (and early 2022) believing it to be a legit recovery, they did the opposite of what had crippled the economy in 2009 and 2010. They gave in to their animal spirits and restaffed. However, even then it wasn’t fast enough owing to just how many jobs had been destroyed by the ill-advised lockdowns.

It seemed like recovery for how fast jobs were coming back, yet the participation rate dipped yet again here in the 2020s from the low levels of the 2010s, primarily hitting younger workers the most.

Employers didn’t bring on nearly enough workers for the economy while at the same time they had actually rehired too many for the amount of work the fundamental economy could sustainably support – this is the illusion, price vs. volume.

The best illustration is the auto business. Prices soared yet employment only came back partway which even then was too much for actual output. Carmakers had assumed full recovery would follow therefore were anticipating needing at least their slimmed-down workforces. When recovery didn’t materialize, the slimmed-down workforces needed to be slimmed down even more which began with a halting on hiring.

Only more recently has the idea of layoffs been broached, with a lot more certainly to come spread out around the entire global industry.

The evidence for this is all over the labor data, too, when you look at the various series relative to their 2010s baselines. Even the CES Establishment Survey is a stunning five million below it, and that’s before we consider the looming QCEW benchmark downgrades (plural – the one for up to March 2024 which won’t be updated until February 2025 and then the next benchmark covering the current period which will near-certainly have to repeat the process).

Household Survey employment is twice as bad as CES, and its measure for full-time positions is an insane ten million below its 2010s trend. These are not consistent with a recovery.

In other words, employers brought back not nearly enough workers; and it was still too many.

Prices aren’t really the matter, incomes are. Had the labor market been able to continue growing and recovering, eventually incomes would have caught up to past prices. That would have required actual output to have recovered and it never did due to the destruction from the lockdowns. That’s the key driving force; we’re finally starting to pay the costs incurred by those.

Authorities had reduced the economy’s potential so much (volume) that when they tried to turn it back on there wasn’t enough left of it to get all the way back. Because the world was short that potential, there wasn’t the need to fully restock on workers similar to the aftermath of 2008. The difference was nominal prices covered the deficiency for a time, convincing some companies to bring back more staff than they otherwise might have, only to now leave them with too many.

Hiring has closed off as a result and only still the first step. This is far from unique to America’s workforce, either, as one Economist in China has become an internet sensation for highlighting youth unemployment over there after lack of hiring has left the younger Chinese generation as an unwilling sore spot in China’s attempted recovery.

Prolonged periods when no one gets hired (only slight hyperbole) are devastating in very real ways that go under- if not entirely unappreciated because, as I said, we aren’t wired to, nor are statistics made to, fully recognize how important something is when it doesn’t happen.

But that’s exactly what the data does show. Hiring doesn’t happen and the consequences are piling up. Again.