WHY TWO AND NOT NONE?

EDU DDA Dec. 19, 2024

Summary: The question everyone should be asking after yesterday’s Fed debacle isn’t about “hawkishness” at all. The real issue is why officials didn’t say the labor market was entirely out of the woods. In fact, we know from the dots as well as Powell’s statements no matter how much they’d like to declare a soft landing they know only too well they really can’t. The labor data is still coming up the wrong way, including several metrics and perspectives even inflation-ist officials are having a really hard time setting aside.

ME AGAIN!

The aftermath of yesterday’s FOMC debacle extended to today. Stocks didn’t rebound even if the DJIA did manage to end its slide on the smallest sliver of a green close. Developing currency crises kept developing (more Brazil interventions). And a growing list of data comes up showing the balance of risks in the US hasn’t shifted at all. If anything, it keeps tilting in the direction toward labor not consumer prices.

We know this, too, by what the Fed did yesterday. Even if it raised the dots, the fact there were any rate cuts on them is already strong proof.

Federal Reserve Fed Chair Powell said this was a new era for the FOMC. What he meant by that wasn’t, as some have claimed, the “central bank” coming to grips with resurgent “inflation.” He instead strongly implied the Fed is getting more mixed signals and is in many ways currently near-paralyzed by them.

That’s what he meant when Powell said what happens in 2025 will have little to do with anything being said or any data being analyzed at the moment. They’re waiting for one side or the other to clear up and given what they have in front of them it hasn’t.

To really understand what I mean, image you are Jay Powell (shudder). The Greenbook – the one which contains all the Fed and ferbus simulations, those that policymakers actually pay close attention to rather than their own dots - comes out and says there’s a growing chance consumer prices might become resurgent. What would you do?

As Jay, you’d say hold interest rates where they are. The higher probability the models indicate for “inflation”, the more likely you are to stay put and the longer you’d consider doing so thinking right now ST rates are “restrictive” (that’s not how the world works, but we’re conducting this exercise from Jay Powell’s perspective).

But what if the Greenbook instead said that there’s a growing chance unemployment doesn’t plateau, or, worse, rather than rise a little more on a gentle slope there’s a very real threat it can get out of control. It even presents the “curve” which has the economy today right on that edge (see: Beveridge below). In that case, as Powell you’d opt for rate cuts starting right now, get it all going to give them a chance to work (they won’t; again, we’re Powell).

How many? Three months ago, that same general description was “worth” four rate cuts or 100 bps, this time coming in three doses. The labor data was already looking the part.

What the Greenbook almost certainly said to Powell and the FOMC leading up to yesterday was both of those scenarios. And he basically said so without using those specific words, as I showed yesterday. Presented with that set of probabilities and still thinking the models are worth more than throwing directly into garbage bin on the Fed’s Windows95 computers (not kidding), you’d simply split the difference.

In other words, the “inflation” risk part says to the Fed hold here. At the other end, the risk to the labor market “deserves” four cuts. All Powell and the FOMC did at their meeting was split the difference. Seriously, that’s what they did. They summed the risks, so to speak, and took their average which was the two cuts in the dots.

I wish I was making this up. And while I may not be privy to the internal discussions nor the latest simulations, I’ve done this long enough and dug through far more material than I care to admit. In short, I think I have a pretty good handle on how those at the Fed would think in certain situations. I just don’t have access to their information, so I can’t always get a read on what those situations being presented might look like.

The current case isn’t one of those times.

To start with, we know with reasonable certainty how Fed officials react where and when it comes to consumer prices. I made a graphic illustration today to demonstrate this. While it’s cartoonish on purpose, the point stands and is entirely realistic.

Whenever the CPI is accelerating on a monthly basis, that pushes the FOMC needle toward holding rates as it has several times thus far.

The real variable, then, is what happens in terms of employment. Right now, the Fed therefore its models aren’t downplaying the serious negatives there, by any means, even if it might sound like they are with all the “hawks” being thrown around. What’s really happening is the estimates are overstating the “inflation” side biased by a couple of factors starting with whatever the last CPI report showed.

Everyone at the Federal Reserve to this day remains scarred by the Great Inflation. And having little insight into where it came from or why it persisted so long, knowing what it did to the institution and its credibility (not to mention, you know, the actual economy and real people harmed by it) the downside for officials is huge.

Worse, eventually Economists came to believe it was fairy tale-style belief which was responsible for the end to the disaster: the Volcker Myth. This requires demonstration of constant vigilance on the part of the Fed and its top members, a never-ending commitment to be inflation-fighter first and foremost. This is what they call “anchoring expectations” which demands top priority.

This is why the Fed overreacts to each and every near-regular re-ascendance of (modest) consumer price increases. Each one activates that deep bias.

But what about those risks on the other side? We already know – and the FOMC does, too – about the current data. Officials will downplay how flawed the Establishment Survey is, yet they all have access to the same facts we do from the QCEW on down.

Where they may be underestimating the risks on labor is in focusing too much on layoffs. This was the mistake Robert Shimer first and most convincingly pointed out. It doesn’t mean that his work and evidence is unknown at the Fed or has been completely dismissed. On the contrary, I’ll bet it is one of the key reasons why the Fed’s models aren’t able to give the labor market an all-clear.

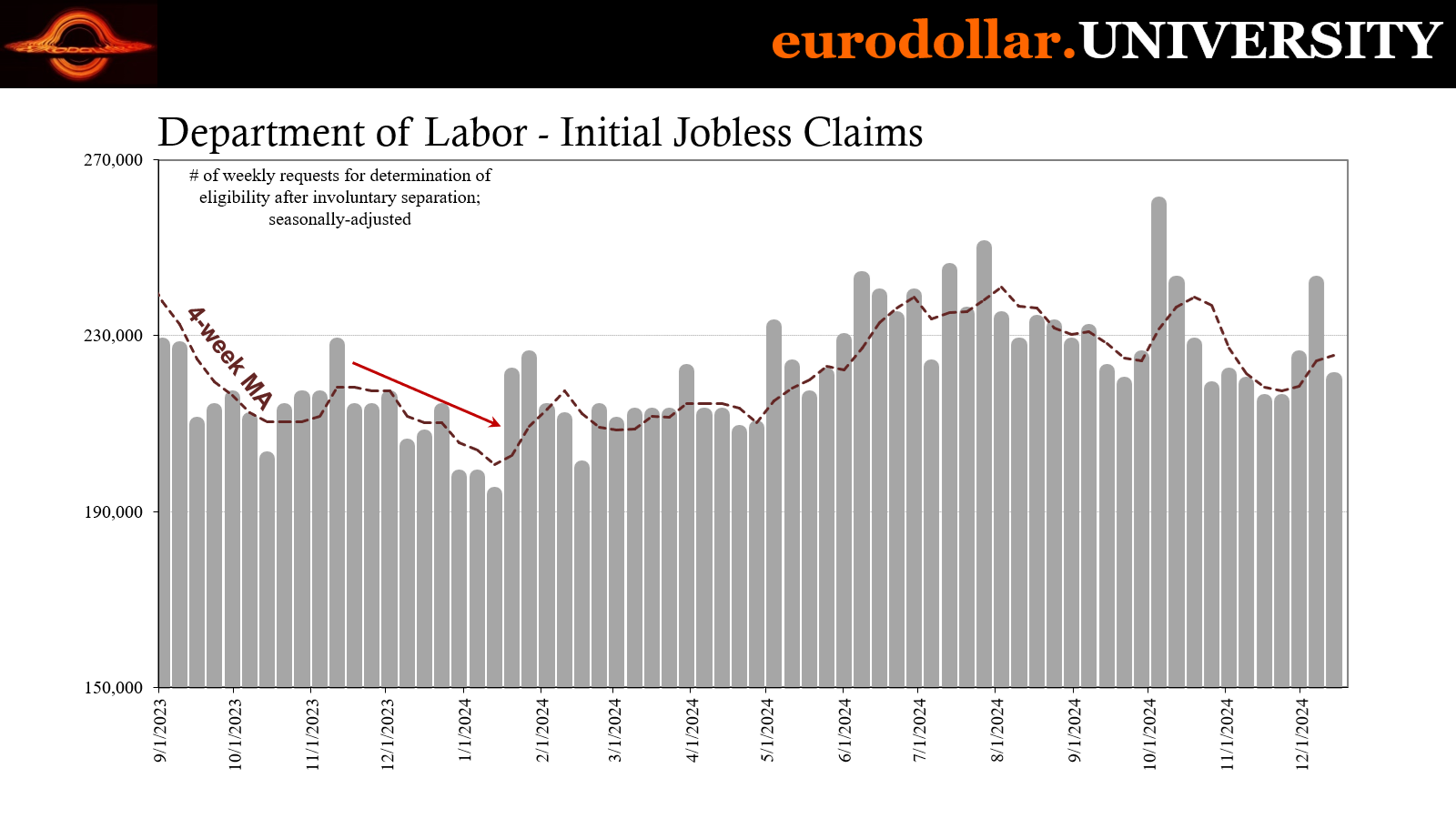

Layoff indications are contained, starting with the lack of media reports on big companies to initial jobless claims which slid back to a lower level again in the latest week after rising by a fair amount in the previous week. There just isn’t (yet?) an inkling of the kind of raw wave of mass firings that look like recession.

So, again, why aren’t the models giving the employment part of the mandate their probability seal of approval? All Powell said was that jobs data overall doesn’t look as scary as it had back in September. Without the layoffs, shouldn’t that be enough?

As Shimer pointed out starting twenty years ago, hiring is the issue not firing. And he went beyond merely stating that case and presenting evidence for it. Shimer also dug into how that process works, making quantitative contributions of his own centering on the “job finding” rate.

It’s simple enough as a concept, though trickier to actually measure in a reliable way. Basically, as labor churn rises, meaning more workers are separated from their current work whether voluntary or involuntary, the cyclical process gets triggered when the number and quality of jobs available lags or declines. Workers pile up stuck unemployed longer they’d prefer, also longer than the economy can tolerate.

This is where the “job finding” rate comes in. When it declines sufficiently it a prime danger zone. There are a couple ways to calculate it, and the Fed around its various branches do keep on top of it for these reasons. In just the past month, I counted three of them writing up worrisome notes on the topic.

Here’s an example from the St. Louis Fed which, I believe, both demonstrates what that warning looks like as well as why the Fed isn’t putting enough emphasis on it.

The most eye-catching results are all right in the job finding/hiring area. Payroll employment is actually weaker in this context than is reported across the media, though not by a degree which would scream trouble. Private hires is another story, way down already in the depths and dumps. But even that one isn’t all that much of a change or further degradation from last November (green line).

Both this year (orange line) and last year are bad, so you can argue with the amount of time in between (an entire year) it wasn’t decisive for a recession (at least according to the accepted view). Where you really see a major change last November to this November is specifically the job finding rate.

That plus hires are reasons to be very concerned about the labor situation. But the rest of the “spider” data at most indicate a slowdown. Fed officials are looking at these variables in a more equal-weighted perspective when they should instead majorly overweight job finding first and hires second. The rest of the data is more noise at this stage.

So, at the very least you can see where the FOMC is coming from when figuring or calculating in its regressions some reason to be concerned on the labor side, enough so as to remain unable to completely set aside those risks. As far as they are concerned, they have to take it seriously yet consider the signals to be “mixed” here, too.

There are other measures of job finding difficulties which didn’t make it onto this one chart (or too far into the FOMC conversation). Part of the CPS/Household Survey, the BLS calculates the median number of weeks those who are unemployed remain that way. As of November’s report, that estimate had jumped to 10.5 weeks.

That’s up a full week just from August, and nearly two going back to April’s 8.7. The median had already moved higher from last fall when the unemployment rate kicked higher and labor force participation peaked. In other words, here’s even more evidence unemployment is being driven by lack of hiring.

This current rise in difficulty measured this way is almost exactly the same as the first stage of the Great not-Recession, too. The median had been 8.4 weeks in December 2007 climbing to 10.4 by September 2008. Back in 2001, when employment was still stronger, the median was 6.1 weeks just prior to the dot-com recession then rising to 7.7 by the end of it.

The 1990-91 S&L recession was similar: from 5.2 to 6.7.

Putting demand for jobs into a context the Fed does very much consider, there is also the Beveridge Curve. For background on what that is and what it means, it will be helpful to review this DDA on it from August. The important points are:

The Beveridge Curve plots that demand for labor (job openings rate) against the possible supply of spare workers (the unemployment rate) meaning in this way we’re lining up both of the friendliest views of the current employment/unemployment situation to see what those might tell us. The purpose of this “curve” is to potentially gauge the balance between supply and demand for labor…what we’re interested in is if we might be able to see if we can pinpoint at least the general area of that possible point of no return, where demand for labor falls off farther because businesses have turned over to firing.

Should hiring and job availability fall off too far, the economic damage gets to be too much and the Beveridge Curve can help pick out those points in past cycles. Based on the current data which unfortunately uses JOLTS job openings on the one side, even with that handicap the curve is already right in the vicinity of the “flat” part of the curve.

Adjusting job openings (in this example simply subtracting one million from each monthly estimate) yields a current Beveridge Curve that is spot on to the last one from 2007-08 right where unemployment exploded higher.

To be very clear, this doesn’t mean or even necessarily indicate a recession has already begun or that layoffs are right around the corner. What all of these numbers do show is that risks over those are high, getting higher, and too much points to a labor market struggling badly in a manner consistent with a cycle change.

More than anyone, even those working at the most ardent inflation-ist institution, can honestly ignore.

So, back to the Fed, knowing all this, they cannot write off the labor market dangers in favor of “inflation” no matter how much they really want to. They desperately would like to declare a soft landing yet that’s not at all what these key measures propose. While officials and models aren’t, in my view, properly weighting the data, they are definitely taking them into account.

Since “inflation” risks are once again imaginary, the real debate and questions surround the “proper” view of labor deterioration. And once the next wave of disinflation breaks over the CPI, that’s exactly where the Fed’s focus will also shift, official expectations for rate cuts will increase all over again (and dots fall).

In the end, given the CPI, the very fact there are two rate cuts in the dots is an acknowledgement of Beveridge, Shimer, and how important hiring really is.

When it isn’t.