THE REAL LEGACY OF SVB IS TRENDING

EDU DDA Jan. 24, 2025

Summary: The dollar soared in December and January. Everyone said it was Jay Powell. We now have more than enough evidence to conclusively show, no surprise, it wasn’t. Instead, a pretty significant dollar crisis when primary dealers hoarded massive amounts of Treasuries and foreign central banks and govts used massive amounts of theirs. But it’s the background which led to this which needs reviewing for what it means about a lot more than this recent monetary breakdown. This starts with Silicon Valley Bank.

MISS ME? I’M NOT BACK - BECAUSE I NEVER LEFT.

How does copper-to-gold get this low, and stay there? Or this negative on swap spreads? It seems like honest-to-goodness dissonance. A bunch of Cassandras must have taken charge of these deep, sophisticated and critical markets. But, no. You have to first understand what it is these signals actually signify as they have slid way, way down to 2020 or 2008 levels.

When you see and make those comparisons, most people immediately think crash, therefore that’s what these prices/spreads/ratios mean and that can’t be possible so it’s dismissed as noise, as nonsense. No, as we’ll see here, that’s Jay Powell-level thinking.

The issue isn’t crash, it is far more important and alarming than that. Everything is really about trend.

To make that point, we start by noting how just over the past two months primary dealers have socking away a record number of Treasury coupons after a truly massive binge in December and January. In addition, American banks have been adding to their own stash and now hold a record amount of Treasury and agency assets, too. At the same time, foreign officials mobilized as many of their Treasuries as they had in March 2023 just after SVB leading up to Credit Suisse.

That’s something that requires revisiting.

Basically, Treasuries have been flying all over the place since the end of November, adding more solid proof to the dollar shortage which had spiked the dollar exchange against nearly everyone else’s currencies around the world.

The timing for everything argues for “trade wars”, significant fears that any interruption in trade might prove somewhere between difficult and catastrophic. We keep seeing November 27 as the moment it all started, timing to the Trump Truth Social post. However, the violent reaction isn’t really about tariffs in isolation.

It’s one more potential economic “headwind” for a global system that’s already in a highly fragile shape to begin with. That’s where the banking system comes in; there’s a dearth of lending activity all over the world. I may have mentioned China’s once or twice. The pittance in European lending is almost entirely to investment funds. Not surprisingly, we see exactly the same thing in the US from American depositories.

I’ll cover the monetary parts of this story in tomorrow’s YT video and get into the broad outlines of banking, only after we go much deeper into the far more profound elements here.

In advance of the video’s publication, let’s start with the recent data: a truly colossal surge in dealer hoarding of Treasury assets which began that same week of November 27. Against that, a flurry of Treasury assets out of foreign largely official hands, more than $80 billion which puts that post-November 27 period on par with March 2023 (bank crisis) and September 2022 (not-gilt crisis).

For those not familiar with the latter of those (another one of EDU’s esoteric indications, as my buddy Gammon calls them), FRBNY offers custody services for foreign governments and central banks. They can “store” their Treasury assets with the Fed’s New York branch so they’re easily used for dollar purposes. What we find is that when reflationary conditions prevail, meaning there are more eurodollars circulating around the world, naturally they end up in official hands and get converted to more reserve assets like Treasuries ending up in custody of FRBNY.

When dollars get to be scarce, such as March 2020, September 2022, March 2023, or December 2024/January 2025, Treasuries “disappear” from FRBNY’s custody since they’re being used by those foreign institutions to fill in some of that implied missing dollar funding. This pattern has held for over a decade, repeatedly validated.

Along with the really sharp rise in dealer holdings of Treasury coupons, both of these are consistent dollar shortage signals. Together, they are solid evidence for a real monetary problem the past six or seven weeks, therefore what was really behind the soaring dollar exchange value (so, not Jay Powell).

While this acute monetary outbreak since November 27 argues convincingly for “trade wars” fears, it isn’t the sole factor nor even the primary one; meaning, the global situation was already on edge and has been for quite some time before.

Bigger picture, this goes back even farther right to those prior dollar outbreaks in late 2022 and early 2023.

To start with, the Federal Reserve and Mr. Powell have been widely credited if not celebrated for how they handled the sudden and “unexpected” (mini)outbreak of bank failures in March and April 2023. As usual, the standard for assessing their performance is assumed to be whether or not the world ended; if it didn’t, then the Fed must have been successful.

It was the same in 2008 and 2009 when Great Depression 2.0 didn’t follow the Global not-Financial Crisis. Since we didn’t see a repeat of the early thirties (completely ignoring whether a catastrophe on that scale is even possible nowadays), Ben Bernanke was uniformly judged to have been a real hero. Then they gave him a Nobel Prize (ironically for his version of why the Fed failed).

In reality, it took some time to truly reveal just how badly the economy and banking/money system had been damaged. While no Great Depression repeat, there absolutely was a depression nonetheless. Any realistic standard for judgment would at the very minimum start with avoiding all depressions, whether great, lesser or even Silent.

The trajectory of the economy was permanently altered due to it, because the same thing happening to the banking system. Trend changes that got to be plainly obvious with enough time and perspective.

We are now more clearly seeing something similar from the aftermath 2023 banking crisis. I don’t mean to that same devastating degree, the same pattern and outline including how after a major event hits, which “no one could have foreseen”, then the Fed is quickly credited with containing the damage without giving it nearly enough time to make a reasonable assessment; one that only years later can we truly get a good enough sense of.

Like 2008, the real worst case wasn’t the event, rather its aftermath. Not the crash, the trend change.

While everyone is judging performance based on a single assumption about a single downside case, crash, the real world offers a spectrum of possibilities very much including like we found after the 2008 disaster. The worst case wasn’t an immediate collapse, it turned out to have been impaired potential that continued to hurt the economy and world year after year, closing in on two decades.

The same thinking was applied to March 2023. No Lehman 2.0, therefore congratulations were made to Chair Powell and friends by May. It was always way too soon to tell, and applied the wrong standard. Further on, we keep finding changed trends all over the world including here in the US.

First off, we have to consider that the banking crisis itself was already an extension of the September/October 2022 eruption.

We already know only too well that parts of the global economy started to “forget” how to grow right in that same timeframe, with the best example being Germany in a pattern that is nonetheless being duplicated in serious if lesser ways all over the place (see: now South Korea).

In fact, the persistence of the trend is what has confounded politicians, observers, as well as central bank officials ever since. They keep expecting a short and shallow downturn followed by recovery, only instead to get another shallow downturn. Then another. And another. Before anyone knows it, Germany is looking at Year Four of this and a new set of government officials.

That late 2022 crisis does appear to have initiated the breakdown in economic conditions. And if it is indeed tied in several ways to the March 2023 banking crisis, which seems more than reasonable if not very likely, there has been other such clear trend changes which then followed SVB, Signature, Credit Suisse and First Republic.

While the world was hailing Powell for the BTFP, the banks themselves had already altered their behavior (lessons of Bear Stears, as I had repeatedly pointed out at the time). You couldn’t see it at the time or even the months immediately following. Now nearly two years later, it is clear as day.

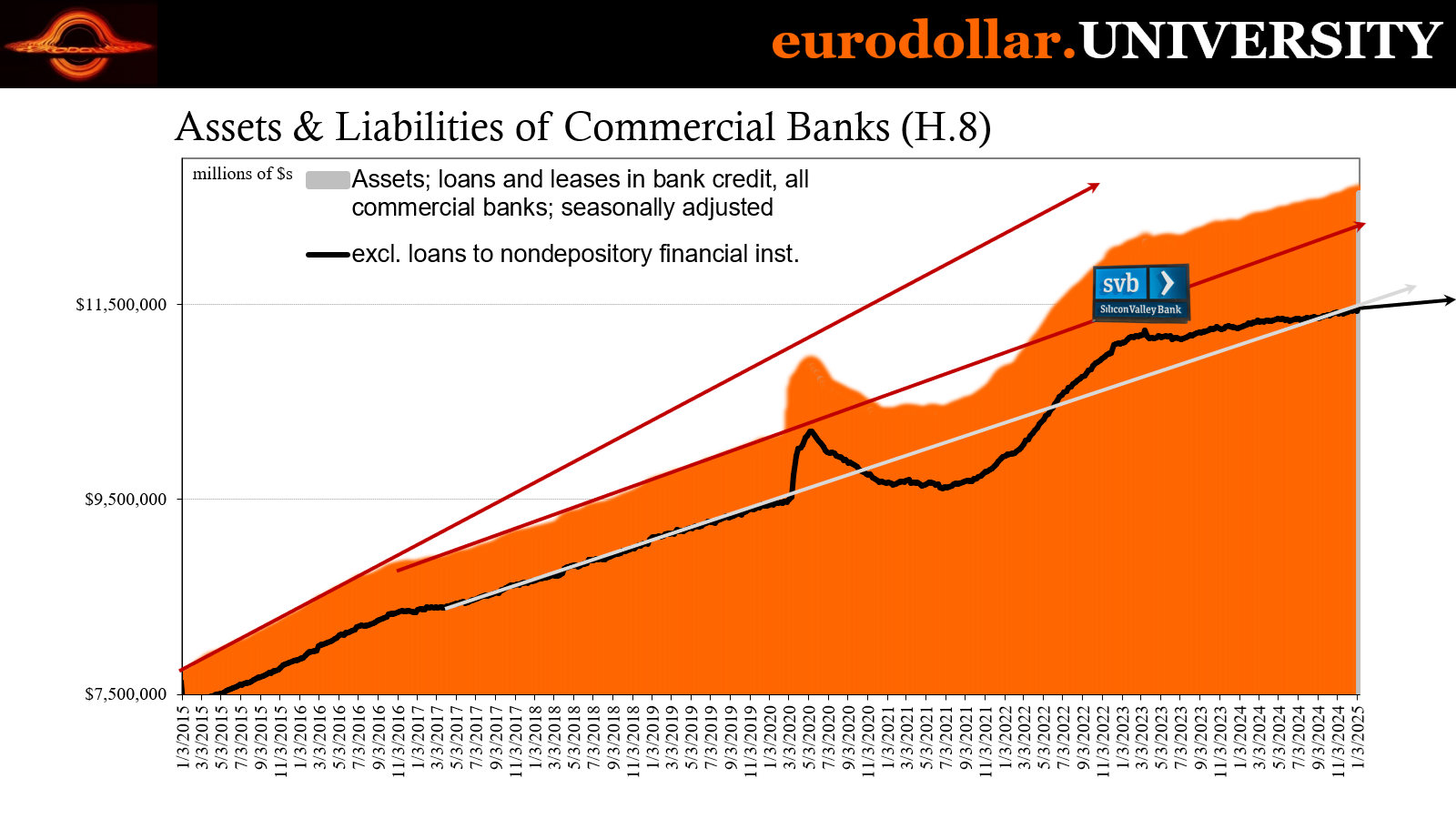

Bank lending total soured. Over in Europe, it had already happened the prior autumn (remember, too, how curves had also gone crazy right at this same time, which is not some other random coincidence). American banking and financial conditions were transitioning, too, and then SVB finished the transition off in reverse of how that very transition had finished SVB off.

See for yourself:

IT DOESN’T LOOK LIKE A POTENTIAL WORST CASE.

It doesn’t immediately look like any big deal. Lending didn’t crash, which is what we’re led to imagine as the worst consequence. Bank lending slowed down after SVB, so what?

Not only that, when you first look at those trends, especially stepping back and analyzing those from before 2020, it at first appears as though banks may have been overextending loans in late 2021 and early 2022, so that transition I keep pointing out really is nothing more than slowing down from “too much” and inflationary (as mainstream sources claim) to something steadier and more stable.

Yet, just like Europe, the majority of that small increase in total bank loans since SVB is in lending to investment funds for financial not real economy purposes. It’s another form of low-risk, highly liquid credit rather than true real economy risk-taking. The fact we see the same thing in both America and Europe only further reinforces this same point.

Doing the math, US loans to non-depository financial institutions soared a whopping 28% since March 2023 (through the latest H-8 data up to middle January). Meanwhile, lending to everyone else increased 2%, or barely a 1% per year rate. That’s a real pittance and lines up with Europe, too.

In short, following SVB if you’re Larry Fink and Blackrock you’ve got all the bank funding you want. Everyone else? Trend change.

Yet, because like GDP or real economy variables that aren’t crashing, the fact bank lending is proceeding along and even growing, if at a very tiny pace, we’re left to believe this isn’t that big of a deal when it really is.

We know it is by the labor market, for example, which began to break down as the unemployment rate bottomed out in April 2023. The official rate began to rise in May when First Republic failed. Bank lending trend changed and so did the labor market and not strictly unemployment, more importantly the lack of hiring seen in at least the HH Survey which has been driving it.

Moreover, when we compare this current trend change in bank lending to previous crisis periods, it already is equal with other major events like the S&L crisis. In that one well over a thousand banks had failed to the point that lending and credit creation (particularly among depositories) fell off for several years.

Loans didn’t crash, they went mainly sideways to slightly lower for a prolonged period. Sound familiar?

Lending slowed down late in ’89 as the crisis reached its zenith. Even then, however, lending only slowed down somewhat in 1990 until the recession finally reached its layoffs stage in November. From there, loans trended sideways to slightly lower over the next two to two and a half years.

During that time, starting from the inflection in November 1989, the S&L recession (as it should be known, and only isn’t because it would make the Fed and its rate cutting look bad which is why the mainstream pinned the downturn on Saddam Hussein for purely coincident timing) happened as did the “jobless recovery” which followed afterward (and cost George H.W. Bush his Presidency once James Carville admitted, “it’s the economy, stupid.”) In other words, that’s how serious bank lending going sideways really is.

Crashing is unquestionably bad, but that’s not the only worst-case scenario. Some worst-cases are actually worse.

Fortunately for everyone in the early nineties, it didn’t turn out to have been the worst case if only because the economic conditions of the time were incredibly, historically favorable and, nearly as important, the whole banking system itself wasn’t permanently impaired, just a part of it. Depository institutions retreated from the scene as major suppliers of credit but had already been overtaken by “commercial banks”, which are really investment firms (eurodollar banks).

In other words, the credit crisis was only ever going to be temporary given the massively fortunate economic and monetary fundamentals outside the S&Ls. And, even then, the sideways for lending was still enough to create the recession and significantly hinder the recovery afterward.

When comparing trend changes, the one we’re dealing with today is already in the same category as the S&L period even if people conditioned to fear only a crash can’t appreciate this. Worse, today we’re seeing this same trend changing far outside the domestic banking system, too, everywhere from Europe to even China. Lending may not be crashing but it doesn’t need to.

We also don’t have an early nineties climate, either, nor commercial banks waiting in the wings to supplant traditional depositories. Ever since 2008, there is no longer any distinction. There is no alternative for loans or banking.

Some people have claimed it is being made up by non-banks like the investment funds noted above, a rash of private credit. While more needs to be said about this (future DDA topic), that actually isn’t anything new, either. The same occurred in the middle 2010s with the surge of leveraged loans and similar. Those undoubtedly softened the depression, yet couldn’t and didn’t come close to erasing its tendencies and restoring the prior trend in credit let alone the economy.

All of this answers the original question: how can copper-to-gold or swap spreads be at levels equal to late 2008/early 2009? Easy. Trend. The markets aren’t saying we’re going to experience a similar crash as 2008. Instead, what they’re anticipating, because it’s already unfolding, is the same kind of aftermath as before, when trends changed for the worse, and, worse, stayed that way.

This latest trend change in economy and banking goes back to late 2022 and early 2023. Jay Powell like Ben Bernanke has been credited (pun very much intended) with saving the world from a worse when there wasn’t nearly enough context to have made that determination. Like after Bernanke, with enough time we can better see and appreciate what that fate really is.

It’s that backdrop which, I believe, heightened the ferocity as a reaction to “trade wars”, the monetary backlash from a global situation that had fallen off from all the way back when Silicon Valley Bank did.

MEANWHILE, WHAT HAVE BANKS BEEN DOING?