ABRUPT PAIR FOR S. KOREA

EDU DDA Nov. 27, 2024

Summary: Just over an hour ago, the Bank of South Korea voted to reduce its policy rate for the second straight time, unexpected because of how rare this has been for BoK. All that does is underscore just how weak the economy there has become. Why? Globally synchronized. Yesterday, the FOMC released its minutes which were predicably conflicted. What South Korea just did - and why - should put any conflicts to rest at least for the rest of the world outside Fed policymakers. Even so, those at the FOMC do appear to realize just how precarious the position really is.

South Korea became the latest central bank to accelerate its rate cutting schedule. Announced just minutes ago, officials there cut their benchmark by 25-bps for the second straight time totally surprising Economists and observers who had near-uniformly thought BoK would hold at this meeting. That is, after all, how the South Koreans normally operate.

This development helps clarify the risks to the global economy as well as which way central bankers including those at the Federal Reserve might really be leaning. The FOMC released the minutes of its last meeting yesterday which contained a few interesting admissions. They are hoping for decoupling yet wary since they, too, can sense things are less solidified than policymakers make it sound when speaking in public (or even being talked about).

Decoupling, the idea behind it, dates back to 2007 and 2008. Each and every time the world gets dragged into a downturn, it doesn’t happen all at once. The differences in timing (and intensity) lead to what looks like categorically different circumstances in various places. At initial onset of the cycle, decoupling referred to mainly China and emerging markets who were said to remain steady even as the US and Europe were being dragged into massive recession.

By the time Euro$ #3 came around half a decade later, the shoe was on the other foot: the West was going to decouple from China and emerging markets (they didn’t quite manage to, experiencing a significant downturn especially in the context of the middle 2010s malaise).

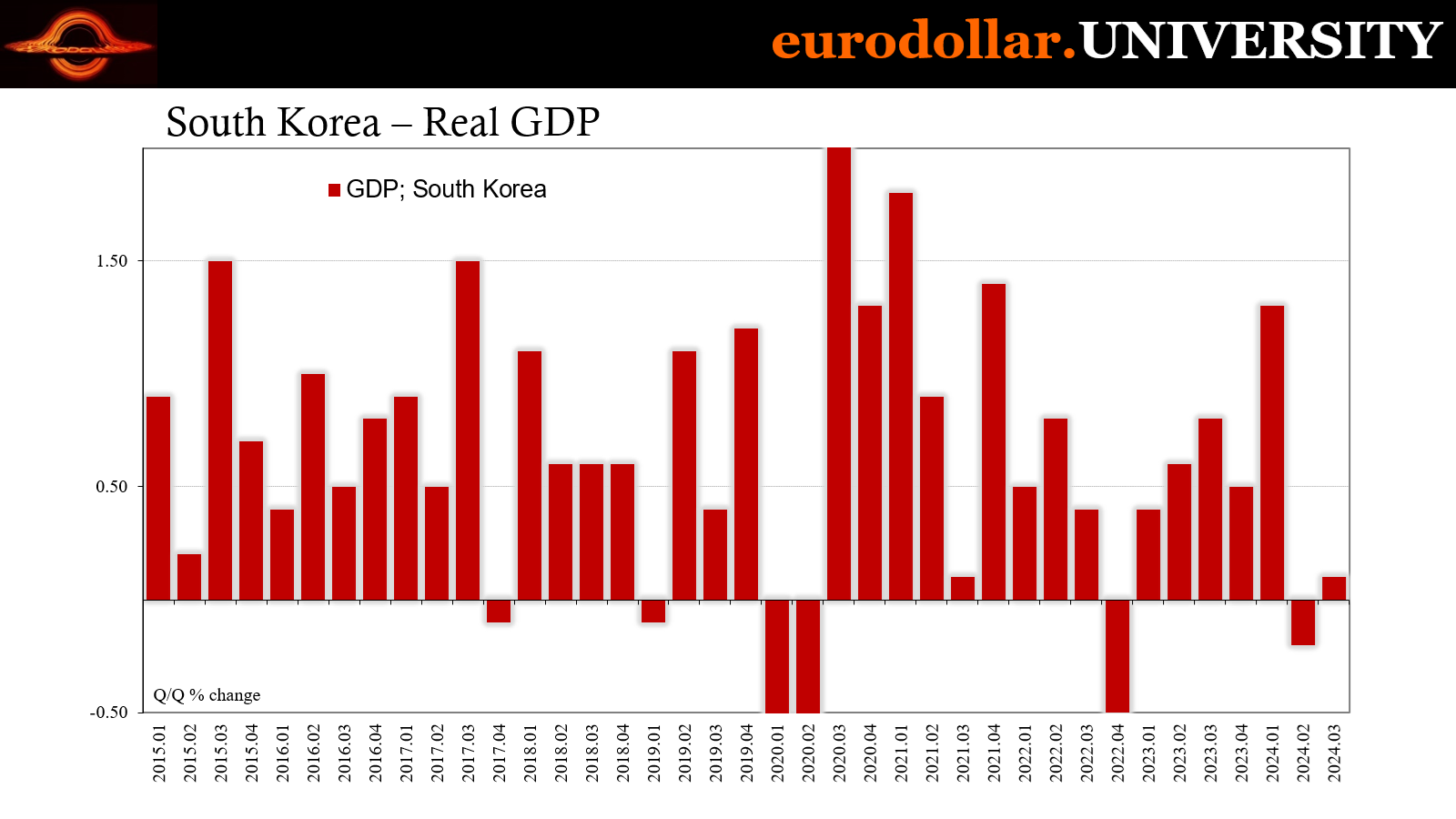

South Korea had been caught up in that one. By October 2017, officials at the Bank of Korea had started to see the country as emerging from its slump (Euro$ #3) and with globally synchronized growth expected to provide a sustained tailwind the central bank raised its benchmark interest rate for the first time since 2011 with one failed cycle after the next.

Twenty-seventeen was supposed to be different. The Koreans were hardly alone. Everyone from Janet Yellen (then Fed Chair) to Mario Draghi (then ECB Governor) believed the same. The reason it was called globally synchronized growth was the fact for the first time since 2008 all the major economies around the world were rising at the same time.

Thinking this was significantly, there wouldn’t be any need to talk about “decoupling” in 2018.

Of course, that’s not how it turned out and South Korea was one of the early warning signs. Along with export-heavy Germany and Japan, the South Korean economy hit a wall even before 2017 had ended. GDP would end up shrinking in the final quarter of the year, a rare sight on the peninsula, something that only happened a small handful of times since the late nineties Asian not-Financial Crisis.

While South Korea would manage to get through 2018 relatively alright, it was clear 2019 wasn’t going to turn out the way it had been imagined just the year before. BoK would raise its policy rate only one more time in November 2018 right as the global landmine was striking which ended up being the mechanism ending any idea of decoupling.

In other words: in 2017 synchronized growth (rather, temporary reflation); 2018 talk of decoupling; 2019 synchronized downturn. It’s the same multi-year process as in each cycle a process that always features a synchronized central bank cycle, too.

The Bank of Korea would be a full participant, beating out the Fed by a matter of a single month. Korean officials would reverse rates twice in 2019 prior to COVID the same as a lot of its peers would, not just the Fed also the ECB which rather than cutting rates (they were still on zero) would just restart QE in place of that.

Here in 2024, South Korea had already sent a warning to the rest of the world with another rare decline in GDP back during the second quarter. It was certainly a shock though not as much as when the country followed it by barely avoiding putting up a second straight negative in Q3. Maybe not a technical recession, close enough to count anyway.

As if there was any doubt about what was driving the economic weakness and therefore currencies including the won, in a meeting with Japan the respective finance ministers of both countries issued a joint statement recognizing the situation for what it was and what it meant.

A joint statement issued after the latest round of bilateral dialogue between Japanese Finance Minister Shunichi Suzuki and his South Korean counterpart, Choi Sang Mok, cited increased volatility in the currency market as casting uncertainty over their economies.

They vowed to remain "agile" in policy actions to ensure economic growth and financial stability as the Asian neighbors grapple with common challenges such as the war in Ukraine, conflict in the Middle East and the global economic slowdown. [emphasis added]

This was June right when the “global economic slowdown” was getting the yen carry trade treatment. That same downturn is the one which flipped the Fed from hawks (holding at their July meeting and sticking to “inflation” as their primary concern) to doves in a matter of weeks. Remember, it was the minutes to the July meeting released in August that all of a sudden said policymakers would have supported a rate cut had it been offered.

Since then, they’ve flopped from that flip. The Fed’s public position according to the latest statement that was released yesterday for the previous policy meeting is that summertime weakness appears to have blown over. Maybe.

When FOMC policymakers say they are data dependent, what it really means isn’t quite the impression you’re intended to get from that term. Data dependence is supposed to mean that officials use care and reason combined with clever insight to come up with an idea of what’s happening and then support their positions with evidence as it comes in. Should the numbers line up, then stay the course. Should the data go in the other direction, that requires rethinking.

It's a perfectly reasonable framework but that’s not what happens. Instead, the Fed won’t even take a position, using each new datapoint to formulate a new one at each and every update. If the CPI is “hot”, suddenly they’re all hesitant as to “inflation.” A weak payroll? Risks immediately shift to the other pat of the Fed’s Congressional mandate. Policymakers don’t have a prior position to check against macro data, they only have macro data to give them a reason to think one thing or another.

Until the next one comes out.

With the labor data looking more and more questionable rolling through summer, the collective feeling shifted to a solid rate cut for September. Since then, some figures have looked better, others seeming to hold up. Today’s GDP update is one of those, the labor data is not. Though they don’t want to admit it because that would require taking a position, and the FOMC just won’t commit to anything, these latest minutes contain clear references to unease about betting too much on decoupling (not that they would ever use that term).

Notice the reference to the QCEW thrown in this mix, something that has been brought up before for very good reason:

A few participants cited business contacts who were using attrition, instead of layoffs, to manage the size of their workforce. Some participants observed that the evaluation of underlying trends in labor market developments had continued to be challenging— with difficulties in measuring the effects of immigration on labor supply, revisions to data, and the effects of natural disasters and labor strikes among the factors cited as complicating this evaluation—and that assessments of the outlook for the labor market were associated with considerable uncertainty. [emphasis added]

This passage was sandwiched in between assurances that everything could be just fine, as if the intended audience for those was the group sitting around the FOMC conference table. They are trying to talk themselves into the more positive interpretation but can’t quite get all the way there with too much – and too many big ones - lining up against it.

And, yes, QCEW is a big one and they know it. The reference to “attrition” tactics circumventing the typical cyclical behavior (in lieu of layoffs) is another. They aren’t stupid or blind, just Economists.

Enter South Korea. The normally steady South Korean economy has not only hit another cycle wall, putting up two negative quarters (when combined), it’s now being judged by the usually stoic BoK as warranting extra-special attention. The Bank had avoided cutting twice in a row in 2019, preferring to stick to a more optimistic interpretation not unlike the Fed’s then or now.

This is why Economists were so surprised at today’s vote. Officials have just done something they hadn’t since the middle of 2015 way back during the devastating blow suffered under Euro$ #3. Globally synchronized again.

It’s more and solid evidence that weakness which developed during the summer (starting before then) didn’t actually disappear on its own. The downturn is still there; just ask any one of the number of US companies which over the past two days have seen their stocks crash reporting American consumers aren’t showing up and shopping for Christmas.

To be fair to the FOMC members, their preferred view of the domestic labor market situation isn’t entirely irrational. It is summarized in this quote which immediately preceded the one shown above (always put the positive take first):

Participants continued to cite declines in job vacancies, the quits rate, and turnover as consistent with a gradual easing in labor demand.

This has been the central bank position and forecast the entire time since early in 2023. Any weakness in jobs and employment is simply slowing down from the supply shock high. And, to be even more fair, that’s how it certainly has appeared up to more recently. But that’s why this summer’s developments were crucial; they showed that whatever might have been the case up to the middle of the year (or around March), it no longer was.

Again, the South Korean example showed the rest of the world something significant had changed. Globally synchronized.

On this side of that shift, other central bankers beside BoK are either doing or considering doing the same thing for the same reasons. The Fed is the outlier here and what the minutes show is that officials appear to understand that but are hoping, and hoping they can bet on, decoupling.

The cyclical part of the world economy has already changed as South Korea pinpointed months ago. Everything else is following along, just not in a straight line. Never in a straight line.

One final note: though it is still the short run it does appear as though the Treasury selloff has finally run its course and for all the reasons cited here. Globally synchronized bonds and rates once again solely because there never is decoupling. With Germany/Europe and China rates sinking, that’s too much fundamental to ignore even if the Fed can’t settle itself.