GOLD PLUGS PARADIGMS

EDU DDA Oct. 22, 2024

Summary: Stocks and gold have been on an incredible run, though mostly just coincidence. Only one of them has fundamental purposes and it is critical to get those right. To understand that significance, we have to detour back to the Great Collapse and the Crash of ‘29 to untangle misconceptions about gold, money, banks, and equities. The missing perspective is the blackhole. Bullion is hedged for the next one to come along, whenever it might and whatever it might be.

Gold keeps going as does the NYSE/NASDAQ. Both the stock markets and gold have had surging runs one alongside the other. Each began theirs around October 2022. On the surface, it would seem as though there has to be some other reason beside random coincidence for this since it has gone on this long, over two years. And there is, just not the one commonly cited.

These are vastly different signals.

Many people wrongly associate equities with money. No fault of their own, superstition has filled in the knowledge gap for uncountable phenomenon going back to forever. Narratives have quite frequently substituted for understanding. When it comes to money, mysticism is all there is so why not incorporate the mysteries of stocks, too.

In this context, rising share prices would appear to be due to increased money circulating if not a surplus having been created. And if abundant “liquidity” is driving stocks higher, inevitably inflation would follow. Since everyone also “knows” gold is a hedge against that monetary evil, the two appear to validate one another.

Much of the first part of this mistaken impression dates back to the Great Depression and its initial collapse. After all, huge monetary deflation triggered by a stock market crash. The real story, as always, very different. It is true that the Black Days of October 1929 set in motion what would become the Great Depression, but the NYSE’s role in it was entirely due to the specific circumstances of that time and it wasn’t nearly the decisive factor.

Money creation since the 1880s had been in the form of bank ledger money, deposit liabilities. Actual reserves of cash were largely hierarchical, being stored in the aptly-named money centers such as NYC.

In that particular one (Chicago and St. Louis being the other two primary centers), there was also a surplus of foreign reserves which piled up in gold and other forms of currency owing to World War I. Much of it was left in New York to take advantage of the booming business and finance of Roaring Twenties USA.

This meant NYC money center banks had excess cash which is an expensive burden. Cash is a cost, requiring some infrastructure to manage. Therefore, if it wasn’t being lent out, it actually yields a negative return. With so much surplus floating around the city and its largest depositories, the banks were itching to find an efficient use for it that also met key constraints.

Banks couldn’t invest or lend out at term. Reserves had to be readily available on short-term notice. For this to work, the banks needed both a return as well as the ability to liquify their loans straight away on demand. And this is where call money came in, also known as street loans.

Right as the name implies, call money is available to be called back by the lender on little notice. To make it even more dependable, these short run advances would be collateralized. And to make that happen, the collateral would need to be highly liquid, too.

At the time, there was no Treasury market to speak of. In fact, Treasury auctions were drawn out affairs where dealers had to solicit subscriptions from customers, holding the cash Treasury buyers physically sent in as a deposit somewhere (in a money center bank, of course) for months on end until the auction finally took place.

Corporate bonds had a limited marketplace, too. Instead, the only real choice was the market is which had been developing for equities. At first, it seemed an ideal accommodation; banks could lend their cash surplus into the call market collateralized by financial instruments backed by the most dependable and regular market around. Plus, stock prices only ever seemed to rise, so even after a haircut the collateral seemed solid in every sense.

With more cash coming into NYC from the rest of the country not to mention the surplus from overseas, the call market boomed as did stock prices. Of course, this was an unstable arrangement very akin to every other one throughout history; the more money flowed, the more stable the market seemed as prices only rose hiding a great instability underlying.

Note, stocks were not money, they were collateral for ST funding.

You can see where this was going to go as we went through something very similar in recent memory when the 2008 crisis wasn’t subprime mortgages, rather how those were packaged into securities that were then used as collateral in ST funding across even larger wholesale money markets. Subprime MBS in 2007 were the equivalent to 1929 equities.

What appears to be safe is suddenly the primary means of contagion sowing fear because safety gets revealed as its opposite.

Even then, however, shares did not cause the Great Depression. They were, like subprime mortgage bonds and other securitized products like CDOs, merely the spark which unleashed a complex and convoluted set of consequences, a sequence of bigger and bigger dominos.

A business downturn that began to develop during the Summer of 1929 put the stock market on edge and led to a growing breakdown in the call market. Once shares collapsed, after October call money near entirely ceased to exist. This wasn’t the deflation, either, rather the next stage in the process. Banks had become obligated to stand behind many brokerage houses as well as each other through the money market transactions. Trying desperately to prop up the entire stock market therefore the price of so much collateral, it only drew the money center banks deeper into the crisis.

It is important to note that the Federal Reserve during all this stood by and did very little. Part of it stemmed from policymakers’ reading of their mandate at the time and disagreements among them about just how much of a role the institution should play and when. For the most part, though, the Fed committed the same fundamental error people still make to this day – thinking that low interest rates equal “easy money.”

The reason why rates in money markets went down was because the only borrowers who could negotiate even a ST loan were the safest out there (just like 2007). Money center banks had thrown way too much of their surplus cash into the growing hole of the brokerage industry, leaving them increasingly exposed to any other large and unanticipated drain – such as a depositor run.

With stocks no longer a viable market to liquidate collateral, once the first major run happened those money center banks were unable to withstand it, having been drained off too much liquidity though they did throughout 1930 almost making it all the way through the year, hanging on for over thirteen months since the stock crash.

There had been small waves of bank runs during 1930, mainly limited to the interior. The significance of them was that it showed how fragile the entire banking system had become, how money did not circulate the way it had before or the way in which was required, cash coming up at a huge premium apart from those highest quality credits. It was simply a matter of time before depositors finally challenged a big reserve city firm.

That came on December 11, 1930, when NYC’s fourth largest bank, the unfortunately-named Bank of the United States, was lost to a run.

Even then, that still wasn’t enough to make the full Great Depression. As Ben Bernanke (the scholar) had pointed out forty years ago, the monetary crash was just the next thing unleashing deflation (which is the lack of sufficient circulation of money, in this case leading to a huge contraction in the stock of bank ledger money deposits) and causing multiple waves taking down banks all over the world. The loss of so many of them permanently damaged the capacity of the entire system to intermediate across the real economy and financial markets.

The equivalent in 2007-09 was in interbank money dealer capacities rather than depository institutions. For systemic purposes, the same broad result, permanent loss for the capacity to intermediate for the eurodollar format of money.

All the while the Fed congratulated itself for its “easy money” policies – both times - which it had supplemented starting in 1931 (after the big banks began failing) with government bond purchases raising the level of bank reserves then doing exactly the same, calling it QE, beginning late in 2008.

Almost nothing in that chain of failures had to do with stocks; equity weakness triggered a shutdown of the money market causing banks to use their liquid surpluses to try to stem the reverse leaving them increasingly exposed to the wider loss of confidence first among other institutions (not to mention foreign governments who yanked their own reserves bank home) then eventually the public.

Stocks merely created doubt about some collateral that led to rising illiquidity the system couldn’t withstand that then became enough monetary deflation it obliterated the capacity of the banking system to intermediate.

For the rest of the lengthy depression, the banking system would simply seek out safe and liquid, prioritizing those characteristics by buying up government bonds however many the out-of-control New Deal feds would issue.

Exactly what has transpired over the last sixteen years, too. Supremacy of safe and liquid no matter how much debt the increasingly bankrupt federal government sells. There’s nothing remotely inflationary in that equation, just like there wasn’t in the thirties.

If there is a key difference it’s that stocks have had no role in any of this since that earlier time, something that was fixed by default during the Great Collapse itself. This is why, for example, there was no Great Depression 2 following the 1987 crash though many very smart people believed that was going to be the case.

This group did not include those at the Fed, however. Alan Greenspan’s FOMC understood the difference so what policymakers at that time were concerned about was any sentimental impact on the real economy rather than some real link between falling share prices and banks, as there once had been in the call market of the twenties. Greenspan’s rate cuts following the crash were meant purely to help shore up sentiment (as is the case today).

Yet, how many people understood this critical difference? Paul Tudor Jones, to give you an example, he made his name and fortune betting on the stock market crash getting that right, only to then incorrectly surmise it would be immediately followed by a depression. The similarities were only ever superficial, including the fact hundreds of banks (S&Ls) were failing in the middle to late eighties, too.

Tudor Jones wasn’t the only one.

No one ever stops and contemplates why stock crash + bank failures of the thirties became a Great Depression but then stock crash + bank failures during the eighties barely merit anything more than a curious footnote to the genuinely booming Great “Moderation.” The entire difference is money; what it is and, most important, how it circulates.

That point came back up in 2007, of course, not from stocks but again from the monetary and banking system (those had long ago merged to become one and the same). Tudor Jones, not to pick on the guy who is obviously wildly successful and who among us hasn’t made really bad calls along the way, weirdly became bullish in late 2007 because of the Fed’s rate cuts!

From October 2007 as the topic of record-high stocks was high on everyone’s mind:

But don’t expect Mr. Jones to relive his 1987 glory. One investor who has spoken with him in the last week, who asked not to be identified because he is not authorized to speak publicly about Mr. Jones’s investment strategies, said that the recent rate cut had made Mr. Jones increasingly bullish. Indeed, as opposed to 1987, Mr. Jones is said to be reminded of 1998, when cuts by the Federal Reserve led to the stock market boom of the late 1990s.

He thought there would be a depression after ’87 because of stocks then decided a few rate cuts in ’07 so everything could turn out just fine. The difference in all of it, 1929, 1987, 2007 and still today is…money. Period.

Since October 2022, stocks or at least stock indexes have had nothing to do with inflation, deflation, money or even the economy. Stocks are up simply because stocks are up.

Whereas gold is something deeper, far deeper and more fundamental than maybe people realize. To begin with, gold isn’t money, either, though it does shine when there is a particularly bright paradigm shift. Before its latest bull run which dates back twenty years now, gold was moribund, when? The eighties, nineties and for a few years into the oughts.

Going back a bit before the “moderation”, gold had previously surged not just in the seventies during the Great Inflation, it was also stirring in its own way steadily throughout the sixties, too, even before the Great Inflation got started around 1966. At the time, governments and central banks were obligated to redeem currency for gold at fixed prices, so the price didn’t change – not officially.

Gold had forced its way to a two-tier pricing system by 1967 into 1968, and going back before then the formation of the London Gold Pool in November 1961 was a recognition that gold was in huge demand. But why? What drove the metal higher from the late fifties until the early eighties, then again picking up in the middle 2000s?

The answer is in the name of this very website: those are eurodollar eras.

Gold is the preeminent hedge for paradigm shifts. The first of those, beginning in the late fifties, the eurodollar system was busting out and taking over the monetary world, completely changing the global order and how everything worked. In those earlier days, it was a very messy and uneven affair with a lot of kinks to be worked out before eventually getting it right.

Gold then receded as the eurodollar made possible the late 20th century boom, a level of genuine and, for the first time, truly global prosperity. The eurodollar system wasn’t the reason for it, as money is not the object, instead the key ingredient allowing it to all work in the way it best can. Money doesn’t create that prosperity but take money away and suddenly all the other components are there but they just don’t work.

As with any human endeavor, the eurodollar took things too far which became quite noticeable entering the 21st century. Gold then picked up on it, participants demand hedging against what collectively was understood what was likely to lead eventual breakdown therefore the next paradigm shift well in advance of 2007. It has been on an upward trajectory – for the most part, there was that delay in the middle 2010s – ever since.

The gold bull is recognition that the eurodollar transition, meaning transition away from it, hasn’t finished; in many ways, it hasn’t even started. And unlike the sixties becoming the seventies during the eurodollar’s initial run, on this side existing within the eurodollar’s final stage it won’t be inflationary. It can’t be.

All the signals we continue to get are lining up on that side for this reason, with gold coming at the problem from a very different angle from other indications, instruments, marketplaces.

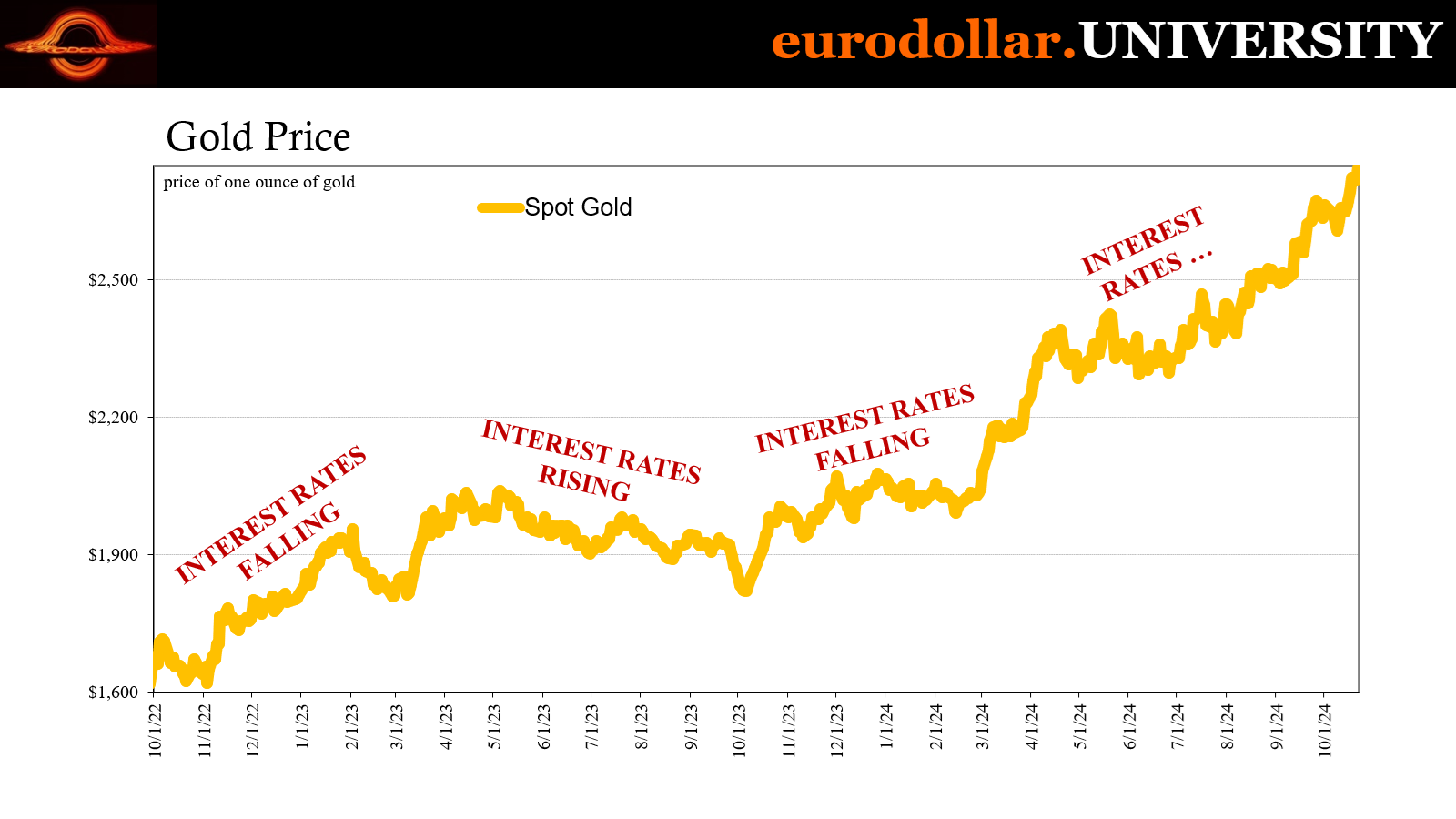

The corresponding rise since October 2022 therefore makes perfect sense. Not only was that partly recognizing how long run interest rates were going to go lower – remember, October 2022 was when yield curves dramatically and historically inverted meaning market rates violently broke from central bank rate hike efforts – as the global economy or enough of it fell into recession. As I’ve been saying ever since, even from well before, the macro downturn was just the process of transitioning out of the supply shock and its price illusion, the world beginning to revert back to its baseline which wasn’t a prosperous post-pandemic condition.

The more it looks like the world is reverting back to the 2010s, the more that means eventually the paradigm must change. Gold is riding the wave of recognition even if individual participants might not be able to adequately describe what it is or why.

To be perfectly clear, this isn’t the-dollar-is-doomed thesis, quite the contrary. The eurodollar stays in place, which is not good, until the next arrangement can take over its vital functions in much the way the eurodollar supplanted Bretton Woods while both were active. Russia, China, BRICS, it’s not that they won’t do this, they absolutely can’t (and this will require a fuller explanation and closer examination in a future DDA).

Basically, gold continues to get confirmation the world needs to do something different, but that something isn’t on the horizon so demand for the ultimate hedge keeps on going.

Whether the stock market soars as a response is really just anyone’s guess. The only real link between gold’s current run and the corresponding jump in stock indexes is, weirdly, interest rates. Equity market participants perceive lower rates as a positive for stocks while a higher chance rates go lower and stay there is definitely a factor for gold.

Not just in terms of lower opportunity cost owning the metal, what long run lower rates imply about a world and conditions that will demand the next system beyond the eurodollar.