XI’S BAD BET AND BAD BANK MATH

EDU DDA Nov. 11, 2024

Summary: China began the month with some mild good news on its housing condition. It hasn’t been able to follow that up, however, with the latest credit data again majorly underperforming. That, plus the slow response on the bank plan from authorities, brings up the possibility of the credit and balance sheet math being against them. Not quite insurmountable, just far more difficult and time-consuming than may are hoping for.

November began with a few morsels of decent news for China in its fight to stabilize its economy and financial situation, the latter plagued by a seemingly intractable real estate bust. While that briefly buoyed the ongoing if less enthusiastic euphoria, there are no easy and quick solutions. This much is becoming clear, too, even in places where the buy-in was immediate and large.

Even in the best case, this is going to be a long process full of dangers and twists. It’s much more complex and difficult than it might currently seem.

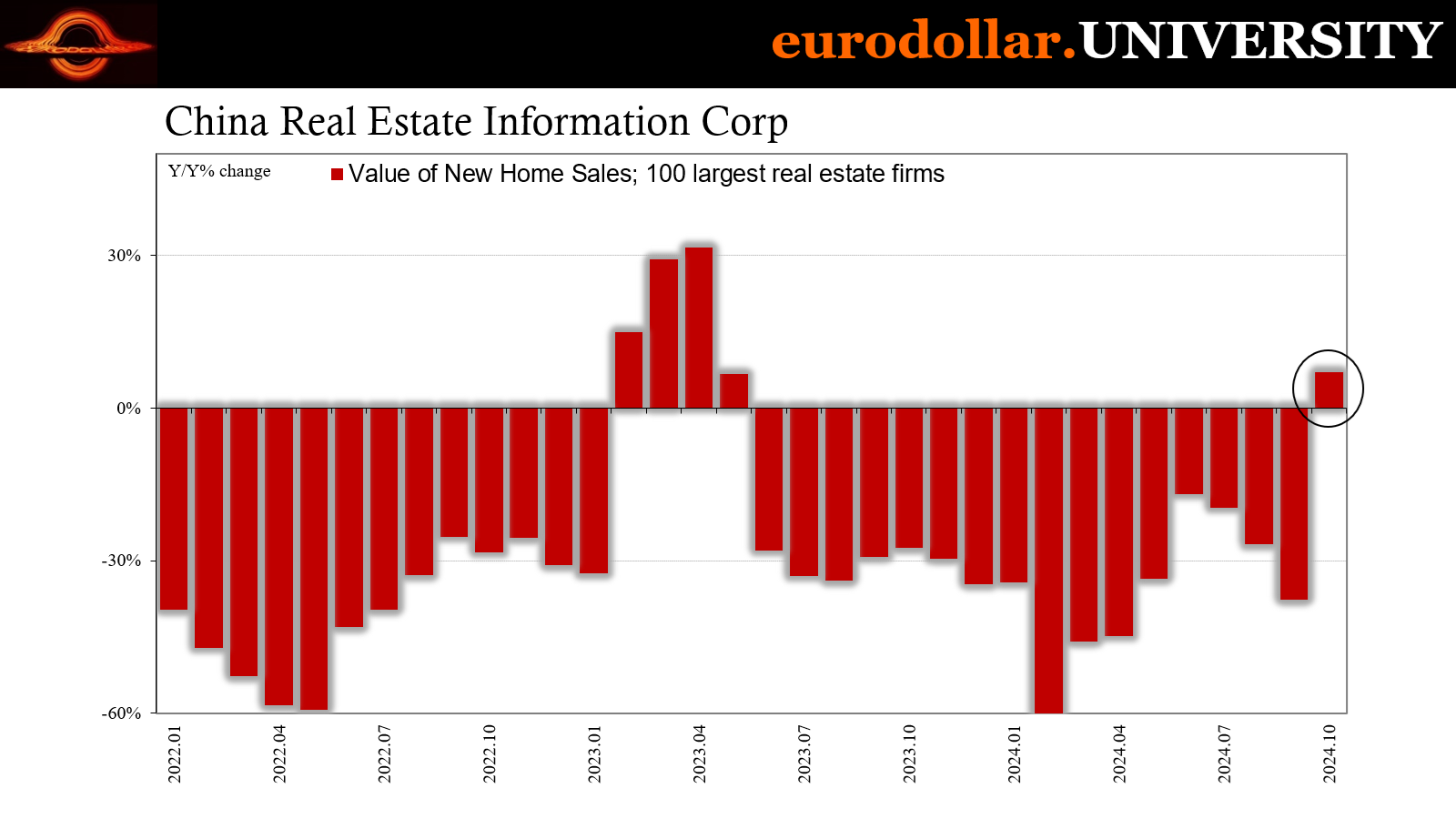

As far as good news, authorities have already lowered interest rates while relaxing various restrictions to make homebuying easier by lowering downpayments and removing onerous regulations in some top cities. It seems to have paid off initially, the government announcing the total value of new home sales booked during October by the country’s 100 largest realtors turned positive for the first time since 2023 reopening.

Not only is that a spread of seventeen months with some of the largest declines ever seen over there, it’s also a sharp turnaround just from September’s estimate of -37.7% year-over-year.

October managed a +7.1% y/y, not a huge plus coming up from an increasingly lowering base but at least on the good side of zero.

There were concerns still afterward, too. The data hid a stark dichotomy that sits at the heart of the matter. State-owned firms saw their sales rise while private developers did not (an average of +26% y/y at the former, compared to -24% y/y booked by the latter class).

In terms of credit, that real heart of the matter, the just-released credit reports for the month of October found only minimal movement in housing credit and lending for the second straight month. Total household loans made were RMB 160 billion after being RMB 500 billion in September. October’s rate is somewhat better than the small decline in the same month last year.

Not much for a full month of “stimulus.” And it only gets worse because this is no longer strictly about developers and homes. Banks are ailing up and down the spectrum, the reason why state regulators have referenced a bank recapitalization plan – though curiously failing to ever follow up on it even as it was announced with the rate cuts back in September.

Officials have offered nothing more than somewhere around RMB 1 trillion to be dispersed among six of the largest. Which ones? What about struggling regionals?

Chinese regulators have had to merge dozens of those already this year. While there appeared to be some movement toward doing much more, that never materialized, either. Every part of this bailout or “stimulus” plan leaves observers wanting real details.

The fact they haven’t been more forthcoming feeds into the growing realization the government doesn’t really know what to do. Feeling pressured in September to do something, they cobbled together a few broad outlines and went with them. The PBOC part, rate cuts, those are easy requiring neither thought nor detail.

Plus, they could be done straight away – and were – making it look like officials were committed.

What the PBOC reported today for the broad credit environment is instead more of the same – as in, more of the same as before September. Banks don’t want to lend. Full stop. There may have been a few more household loans last month, in reality little more than a rounding error.

From the Financial Statistics Report, the total outstanding stock of RMB loans rose 8.0% year-over-year, yet another new record low and missing expectations for 8.1%. Of greater concern, Total Social Financing (TSF) – the broadest credit and money measure China has – grew by just 7.8% y/y, its own record low.

That one includes government borrowing and financing already behind last October.

“Stimulus” borrowing wasn’t enough to keep up with the ongoing retreat at the bank level. From the TSF perspective, new RMB loans were just 500 billion. October isn’t a big month for credit by any means, it does continue the yearlong slump which has seen new bank loans collapse by an astounding 22.5% comparing the first ten months of 2024 with the same months in 2023.

It puts this year’s trend so far below the precrisis they aren’t even the same thing anymore. China’s initial response to the pandemic/lockdowns was a burst of debt which banks obliged, bringing 2020’s tally above that trendline. They were slowed in 2021 and 2022 by further lockdowns then revived in 2023 for a limited time by reopening.

The failure of reopening, as I pointed out at the time, was a watershed moment for China and its banks, a wholly underappreciated development. A lot had been staked on the government’s Zero-COVID policy being the reason holding the Chinese system back. Once it became clear that wasn’t the case, the retrenchment has been increasingly severe.

Led by the banking system.

For banks, specifically, this meant they had limited space and capacity to keep operating their balance sheets. Bad loans had been accruing on them for a long time before the last few years, yet operating results/profits were just enough for the various depositories to write them or move them off (repackaging as “bad bank” assets, called “asset management companies”).

When the real estate market failed to reignite on reopening, that meant banks had nowhere to go to make profits. Same for the real economy. Up to that time early in 2023, banks were thinking (more like hoping) once the system was opened back up that would mean some parts of their loan-making business would recover and, if so, they could depend on profitability there as the means to clean up non-performing assets stacking up by then.

Losing out on both counts, real estate and economy, has meant banks have shrinking capacity to handle bad debts and expansion. Without being able to generate return on equity, writing off more equity would erode their capital base too far, too fast. Loan growth that had already been slowing down before then suddenly accelerated massively to the downside, particularly in 2024.

Now those non-performing loans (NPLs) are piling up with no way to handle them and an economy stuck in between.

The official totals indicate somewhere around RMB 3 trillion across the various classes of lenders. There are about RMB 4.6 to 4.7 trillion additional troubled assets classified as “special mention” loans that aren’t quite non-performing, a step or two away (in a worsening economy, housing market).

Those are just the estimates authorities provide, so are taken as the floor. Some private, outside observers believe the real scale is at least two if not three times that.

It isn’t just strictly real estate loans, either. The infamous Local Government Financing Vehicles (LGFV) Beijing is now intending to swap its debt for were financed in large part by Chinese banks themselves. Understanding this helps explain why so much of the current fiscal “stimulus” seems to be focused on local governments.

First, the municipalities are struggling being able to meet basic services, thus in bad need of a boost just to maintain minimal expected capacity. They can’t repay LGFV liabilities and provide those given their current lack of revenues when so much of their revenue base had historically been generated by land sales and development fees (skimming).

You really begin to see how entangled all these various pieces really are. It all goes back to the Silent Depression and how China initially chose to deal with its immediate aftermath.

LGFVs got going and borrowed from banks, spiking the real estate bubble which kept China busier than it would have been without it, just never quite busy enough to reach liftoff. It only ever partly filled in the loss from the Silent Depression which meant more debt was yielding less real results. The economy kept slowing down, raising perceptions of risk which slowed it all even more.

China has been on a collision course the entire time – and Xi Jinping has known this since before 2016. He may not have been truly certain, which is why he gave Li Keqiang the space for one last try in 2016. Once it became clear it wasn’t going to work (it didn’t take very long), Xi pulled the plug, enshrined Xi Jinping Thought on the New Era in the constitution at the 19th Party Congress, and has been try to hold everything together managing the decline.

The pandemic, it turns out, was one more stumble neither China nor the world could really afford. It didn’t look that way straight away, of course, which is, I’ll note again, that seems to have been the one big blunder Xi committed. All the evidence points to the Chinese leader buying the boost China got from the early supply shock and seeking to use it as a platform to accelerate the economic transformation; at least by taking more air out of the real estate bubble (the “red lines”).

It seems very likely that, apart from a sudden bout of insanity, Xi saw the level of economic growth in those early days from 2021 as the means to keep the banks loaded; they could continuously rebuild their capital from profitable lending to a booming real economy which would allow them to speed up the process of clearing bad loans off their books as well as the transition away from property development.

This would have been a win-win-win. It is possible that the government underestimated the severity of bank balance sheet quality, too; after all, they badly miscalculated on the economy. Perhaps Xi really was desperate and decided to just take a shot, a stab in the dark hoping maybe it could work.

Whatever the reason or reasons, the math just never worked and it only would have had any chance in the boom scenario. That’s why I think the mistake was macro and I also believe that explains why Beijing had been so reluctant to deviate from that path for so long – starting with putting so much emphasis on and, really, faith in reopening.

Once it failed, they couldn’t see the bank math had turned decidedly against them, the credit environment really began to sour, and the economic danger turned way up by 2024.

Now they’re facing questions about whether or not it is too late to start digging out.

That should therefore mean even more emphasis on bank recapitalization, yet nothing is forthcoming. My suspicion is that authorities don’t quite yet know the full extent, particularly how much potential exposure there might be from any fallout only starting with LGFV debts. Thus, the central government absorbs as much of that as possible reducing the ultimate need for capital at the bank level.

This still leaves the real estate NPLs (and whatever LGFV doesn’t get swapped). They don’t want to risk acting too quickly, underestimating the balance sheet math, then being forced later next year to come back and do it again. That would risk undermining everything, up to and including transforming what is a still-growing credit crisis into a liquidity one.

Even if done well armed with good information and undertaken with loads of foresight, balance sheet cleanups are still messy and a drag on economic performance. They take time, sometimes a lot. And, unlike 1998, this time for China the world is in a vastly different place.

Given all that, there should be no surprise the October credit stats were beyond underwhelming. I still believe that means the Chinese don’t really know what they’re doing just yet, too. Authorities know they can’t drag this out forever, though they are equally aware acting prematurely could end up being worse. The whole thing is fraught with landmines.

People or markets looking for a quick fix aren’t going to be happy. Even if successful, and there is a decent maybe not majority chance the Chinese pull this off, it will take time. The October credit data was first a reminder over that, and, second, the math really isn’t in Xi’s favor.