Daily Briefing 1/31/25

Consumer Prices (BEA)

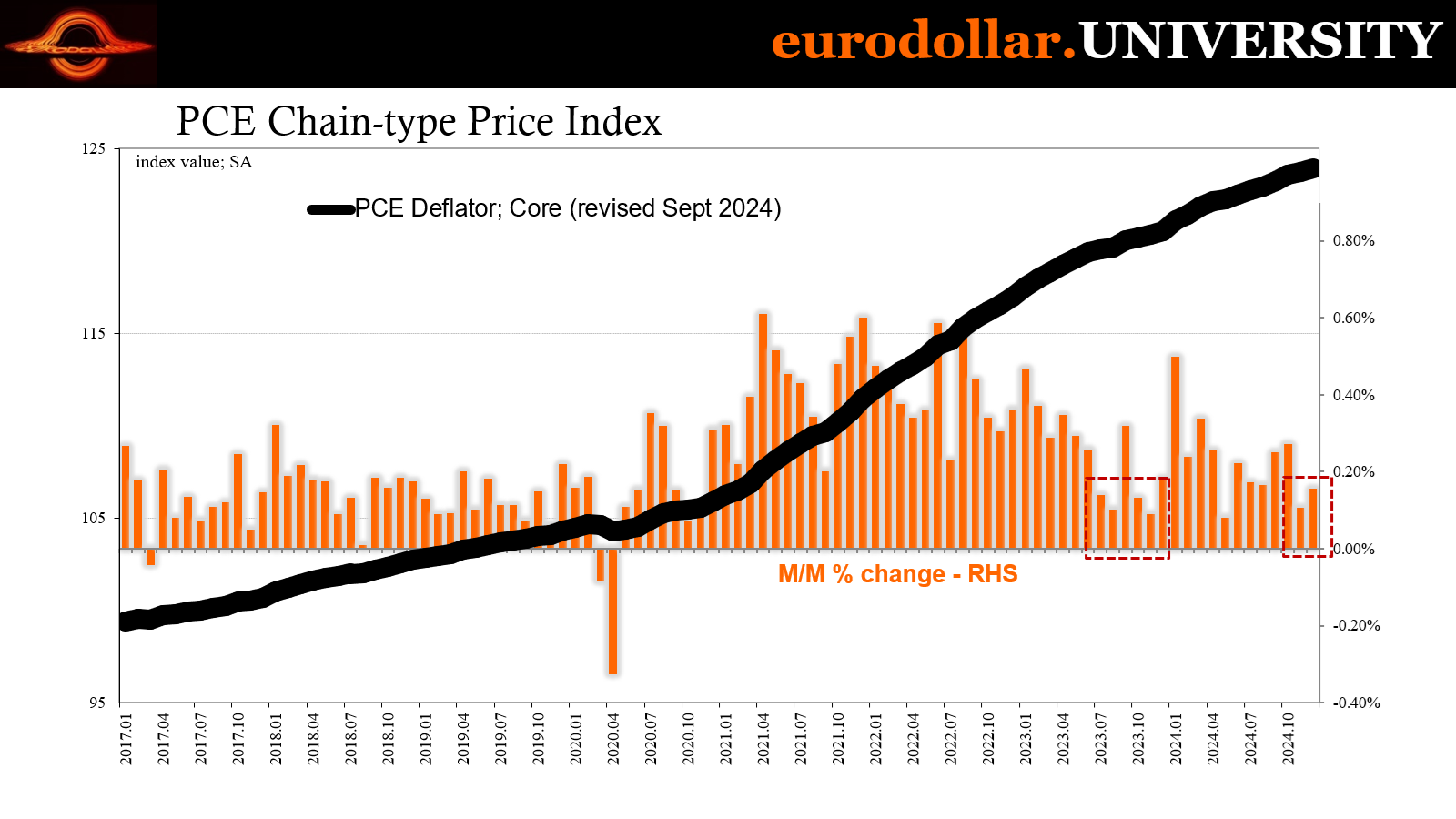

The BEA’s deflator version of consumer prices moved up to a 0.26% month-over-month in December 2024, above the 0.12% m/m rate from November and the fastest since last April. From a year ago, the index increased 2.55% compared to 2.45% year-over-year prior. Core prices were only 0.16% m/m higher last month (vs. 0.11% m/m), rising 2.79% y/y (vs. 2.82% y/y).

Interpretation

As usual, the CPI takes all the drama and suspense out of consumer price results simply by virtue of being released roughly two and a half weeks prior. The December estimates for the BLS series had already previewed the effect of retail (certainly not wholesale) gas prices on the overall average. So, we were on the lookout for the same from the BEA’s deflator, which it provided.

Since it wasn’t inordinately out of line with the CPI, the highest monthly rate for the deflator in eight months was treated as a non-event. And like the earlier December CPI, most attention was focused on the core rate given the influence of the energy component on the overall calculation.

Same thing PCE and CPI, December making two straight months of relatively benign increases. For the former, November and December combined are back to the July-August summertime pace if not going farther on the disinflation side. In fact, it was the slowest two-month change since November and December 2023 (hidden seasonality?); yet again demonstrating how “strength” in consumer spending shown above was limited to certain segments and categories rather than some broad upswing.

The core’s annual rate remained stuck for yet another month at ~2.80%, right where it has been since last March. It’s not exactly “sticky” as commonly described since a lot of that was front-loaded in the first half of 2024. Over the second half, the index gained only 1.1%, or a 2.2% annual rate and slowing materially in four out of the six months.

While another example of the discontinuous process of disinflation, and how much the variations in it are driven by gasoline, both the CPI and the PCE deflator show consumer prices overall are moving back toward recognizable disinflation, the pendulum swinging back in that direction just in time for the FOMC to flip-flop again.