SENTIMENTAL PARALYSIS

EDU DDA Jan. 29, 2025

Summary: The FOMC announcement went as everyone expected. It was the language used in conveying the statement which caused some commotion. For his part, Chair Powell made things clearer by offering to clear up nothing. Officials have no idea what to think on the economy, particularly prospects for trade wars. That’s more than curious because policymakers have an enormous volume of scholarship on the subject from which to form solid opinions. Still, they refuse. Why?

ARE TRADE WARS INFLATIONARY OR NOT? WE KNOW THE ANSWER.

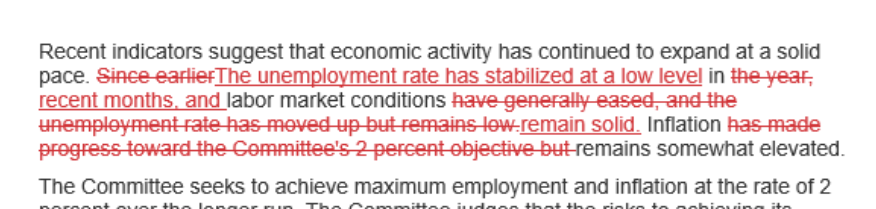

Today’s FOMC release got made into a minor mess for what was supposed to have been a total non-event. In the end, it proved to be anyway. The Fed held rates as everyone expected, yet decided to rewrite nearly the entire first paragraph of the press release, the important bits.

I covered the statement and market (non)reaction in both today’s YT (live) video as well as the Daily Briefing. Check those out for the particulars. Here’s the most succinct summary of the fiasco:

Given so many unknowns here in 2025, starting with prospects for “trade wars”, the FOMC wasn’t doing anything other than saying, we really don’t know. Maybe disinflation will continue to make more progress over the months ahead, policymakers refuse to commit to it because by their models tariffs might inflationary or deflationary, the labor market might still be on the “tight” side of the Phillips Curve, or unemployment could even be too far into the Beveridge Curve it suddenly explodes higher from here.

Policymakers’ biggest concern is obviously the prospects for large tariffs. When asked about them at his press conference, Chair Powell pleaded complete ignorance when there was no reason for him to do so (as you’ll see). It was basically the same answer Governor Waller had given a few weeks ago when Waller said, paraphrasing, if the economy turns out weaker or more disinflationary the Fed will cut rates, and if neither of those happen it won’t and could even raise them.

In other words, everything is on the table as far as officials are concerned when it should not be this way at all. This unnecessary complication, at first, appears unnecessary.

Powell said essentially the very same thing Waller had:

The range of possibilities is very, very wide. We don’t know for how long or how much, what countries. We don’t know about retaliation. We don’t know how it’s going to transmit through the economy to consumers. That really does remain to be seen. The best we can do is what we’ve done, which is study up on this and look at the historical experience, read the literature and think about the factors that might matter.

What? Totally noncommittal when there’s no legitimate reason for this. To begin with, we already have experience with “trade wars.” It might not be exactly the same, far closer than you might imagine.

In fact, when asked to determine the prospective broad economic consequences from Trade War 1 that first time around, the Fed gave near exactly the same answer Powell just did. In late August 2018 – so already quite a way into the tariffs – the FOMC released the minutes of its policy meeting held three weeks before July 31/August 1.

On the subject of possible impacts from the trade matters, all it would say is, “all participants pointed to ongoing trade disagreements and proposed trade measures as an important source of uncertainty and risks. Participants observed that if a large-scale and prolonged dispute over trade policies developed, there would likely be adverse effects on business sentiment, investment spending, and employment,” and that “an escalation in international trade disputes was a potentially consequential downside risk for real activity. Some participants suggested that, in the event of a major escalation in trade disputes, the complex nature of trade issues, including the entire range of their effects on output and inflation, presented a challenge in determining the appropriate monetary policy response.”

Basically, trade wars might be inflationary; they might be disinflationary; they may spark consumer retrenchment; or, maybe unleash a real price spiral. Policymakers completely refused to give any answer because, like everything else, they really had no idea how the economy operates and so have no way to factor one more unknown.

Mainstream observers had less difficulty expressing singular views. Most were decidedly on the side of price pressures. From the financial media to maybe the vast majority of financial services, the thinking was the same as that for whenever crude oil spikes for non-economic reasons. Costs of important goods go up, how can it be anything other than inflationary?

Here’s one example among thousands from right around this same timeframe back in the summer of 2018:

The trade wars have moved from political rhetoric to actual law, affecting global trade flows between the world’s largest economies. For the US, the biggest burden may be a rise in inflation, potentially forcing the US Federal Reserve (Fed) to quicken its pace for further interest rate hikes.

Trump’s aggressive stance on trade has put the Fed in an awkward situation, where it is forced to raise interest rates to match increasing consumer inflation. We project two more interest rate hikes in 2018 and three in 2019, but the additional tariffs may increase the number of hikes in 2019.

NOPE, NO INFLATION FOR 2018 OR 2019.

While the two additional rate hikes took place over the balance of ‘18, none of the rest of that happened. Some prices increased, yet disinflation intensified especially the following year. The Fed involuntarily and summarily ceased rate hikes in December before cutting three times in 2019 with consumer price rates diminishing along with deteriorating global economic conditions.

Having gone through that experience, it ushered in a flood of studies, reviews, and retrospectives on the matter and the consequences. As Powell himself said today, he (meaning the staff) is going to be incredibly busy reviewing all the literature. But, why wait? Or why delay having an opinion? The work has been done and is easily available.

It’s all there. The combined verdict from the mountains of ink spilled on the topic remains uniform and broadly shared.

One of the most influential and widely cited (over 1,000 citations) was this March 2019 paper published by the NBER. The authors found that:

The deleterious impacts of the tariffs have been largely in line with what one might have predicted based on a simple supply and demand framework. We estimate the likely impact on U.S. consumers and find that by the end of 2018, import tariffs were costing U.S. consumers and the firms that import foreign goods an additional $3 billion per month in added tax costs and another $1.4 billion dollars per month in deadweight welfare (efficiency) losses.

Yeah, $1.4 billion per month in lost collective income…for a $20+ trillion economy. Cue the Dr. Evil meme.

That wasn’t the total cost, however. They also found additional inefficiencies would exert secondary drags on activity, therefore raise the damage even higher.

We estimate that if the tariffs that were in place by the end of 2018 were to continue, approximately $165 billion dollars of trade per year will continue to be redirected in order to avoid the tariffs. Given the fixed costs associated with the current supply chains, this reorganization of global value chains is likely to impose large costs on firms that have made investments in the U.S. and China, as they have to move their facilities to other locations or find alternative sources of import and export destinations.

Notice that the anticipated drag is not $165 billion per year; that’s merely the amount of total trade that the study figures might have to find another third-party route by which to circumvent the tariffs (as the Chinese appear to have done rather effortlessly, contrary to this warning). In other words, maybe a few billion would have to invested in 2019 and afterward to beef up additional facilities in other places.

It's all so underwhelming. But what keeps this inflation-tariff narrative alive is this part:

We find that the U.S. tariffs were almost completely passed through into U.S. domestic prices, so that the entire incidence of the tariffs fell on domestic consumers and importers up to now, with no impact so far on the prices received by foreign exporters. We also find that U.S. producers responded to reduced import competition by raising their prices.

Prices got raised, yet that isn’t necessarily inflation let alone inflationary.

Another influential study later in 2019 from the Federal Reserve drew similar conclusions, finding diminished economic activity, lower industry income, and a rise in producer prices. In other words, input costs rose which squeezed profit margins rather than being passed fully along to consumers as what everyone wrongly assumes is inflation.

We find that the 2018 tariffs are associated with relative reductions in manufacturing employment and relative increases in producer prices. For manufacturing employment, a small boost from the import protection effect of tariffs is more than offset by larger drags from the effects of rising input costs and retaliatory tariffs. For producer prices, the effect of tariffs is mediated solely through rising input costs…While one may view the negative welfare effects of tariffs found by other researchers to be an acceptable cost for a more robust manufacturing sector, our results suggest that the tariffs have not boosted manufacturing employment or output, even as they increased producer prices.

Similar to any oil price spike, which will raise consumer and producer prices temporarily, it never leads to some inflationary process let alone a major spiral requiring immediate and forceful policy attention.

In sum, tariffs like oil prices harmed the economy and even then it wasn’t enough to explain the global recession developing in place of recovery. Trying then to reconcile how the global economy the same Economists and central bankers were certain in 2018 was heading for an even stronger 2019 had gotten derailed, they came up with “trade war sentiment.”

Not tariffs or even price changes, the negative psychology Economists use to plug in the considerable gaps they have in understanding the real economy and its workings (let alone the colossal black hole in their monetary worldview). Back to the first study noted above:

Our estimates, while concerning, omit other potentially large costs such as policy uncertainty as emphasized by Handley and Limão (2017) and Pierce and Schott (2016). While these effects of greater trade policy uncertainty are beyond the scope of this study, they are likely to be considerable, and may be reflected in the substantial falls in U.S. and Chinese equity markets around the time of some of the most important trade policy announcements.

The stock market!

Policymakers themselves had already been considering these possibilities. The Federal Reserve just released its FOMC meeting transcripts for the year 2019. While I haven’t had the chance to review all of them (other than have AI scan them and locate some interesting inclusions), I have seen many examples similar to the above as well as the following which took place in June 2019.

MS. MESTER. Even firms not directly exposed to the tariffs expressed concern that the renewed uncertainty will weigh on sentiment and investments. Some contacts are beginning to reassess pending capital projects, and some smaller firms are holding off on acquiring financing for new projects because of the uncertainty surrounding trade policy and tariffs.

Funny enough, what Cleveland Fed President Loretta Mester had said just prior to the above should have been ended the entire argument:

MS. MESTER. Some manufacturers indicated that new tariffs will compress their profit margins more than the earlier tariffs did because they have limited ability to raise prices, especially if demand softens. Indeed, price pressures in the District have eased since last summer, with the majority of firms reporting they haven’t changed prices in recent months. [emphasis added]

Whatever trade wars might be, the underlying economic conditions are what ultimately matters. A few billion in lost income isn’t the end of the world; it still doesn’t help an economy already struggling.

And this wasn’t just one Fed branch president related a single anecdote from her district, they found the same all over the economy. The results were absolutely conclusive.

Tariffs reduced activity and incomes, raised input costs and squeezed margins. There was absolutely no inflationary impact. Zero. None. Increasing input costs is not inflation no matter how many times it gets confused for some. Repeatedly.

Yet, the economy was experiencing a major downturn regardless, thus the appeal of “trade war sentiment” as a depressing agent to fill in the gap. It couldn’t have been that the 2018 economy with its “labor shortage” and presumed recovery tendencies was a mirage based on a misreading and overassessment of 2017’s relatively underwhelming globally synchronized growth.

Admitting to those facts would require also admitting the markets had been right the entire time, with flattening curves fighting against the Fed’s rate hikes and forecasts all the way to the “unexpected” rate cutting.

The lesson or lessons applicable to 2025, assuming trade wars do happen, maybe as soon as Saturday if the February 1 deadline still applies, is, first, they are the opposite of inflationary. Even if they don’t represent a massive challenge to the economy, around the edges they depress activity and compress profit margins. They raise the costs to the trade economy, as if that is somehow a profound revelation.

Therefore, even if 2025 tariffs do impact the global economy, they are far more likely – if not inevitably – to cause more disinflationary harm and depress activity than any semblance of inflation. That’s not my view, it’s all the academics which came out of the 2018-19 period, reviews and conclusions everyone at the Fed today already knows.

So, why this nonsense about trade-wars-are-inflation-maybe? Because what Powell like Waller really said was, they have no idea. The FOMC is completely blind to what the economy is doing right now having been caught off-guard by this latest (and predictable) short run rise in the past few CPIs up to last month’s. Their models are useless. Policymakers keep getting hammered for missteps, both perceived (by the public) and real ones.

They are, in a word, paralyzed.

Remember, the Fed in Summer 2018 had said it didn’t know how trade wars would go. Officials said the same thing today, near exactly, despite having all the answers and evidence right in front of them. Maybe they say they don’t know because they really don’t.

Tariffs won’t help an economy already experiencing global weakness. Those instead make it worse. Not by a huge amount, and with varying degrees depending on where the focus might be. No need to appeal to “sentiment”, either, Economists’ favorite stand-in for we-don’t-know-what-else-it-could-be.

The one aspect which is most certain is that tariffs like oil price spikes are the opposite from inflationary. The only real question is by how much.