Daily Briefing 3/13/25

Producers’ Price Index (BLS)

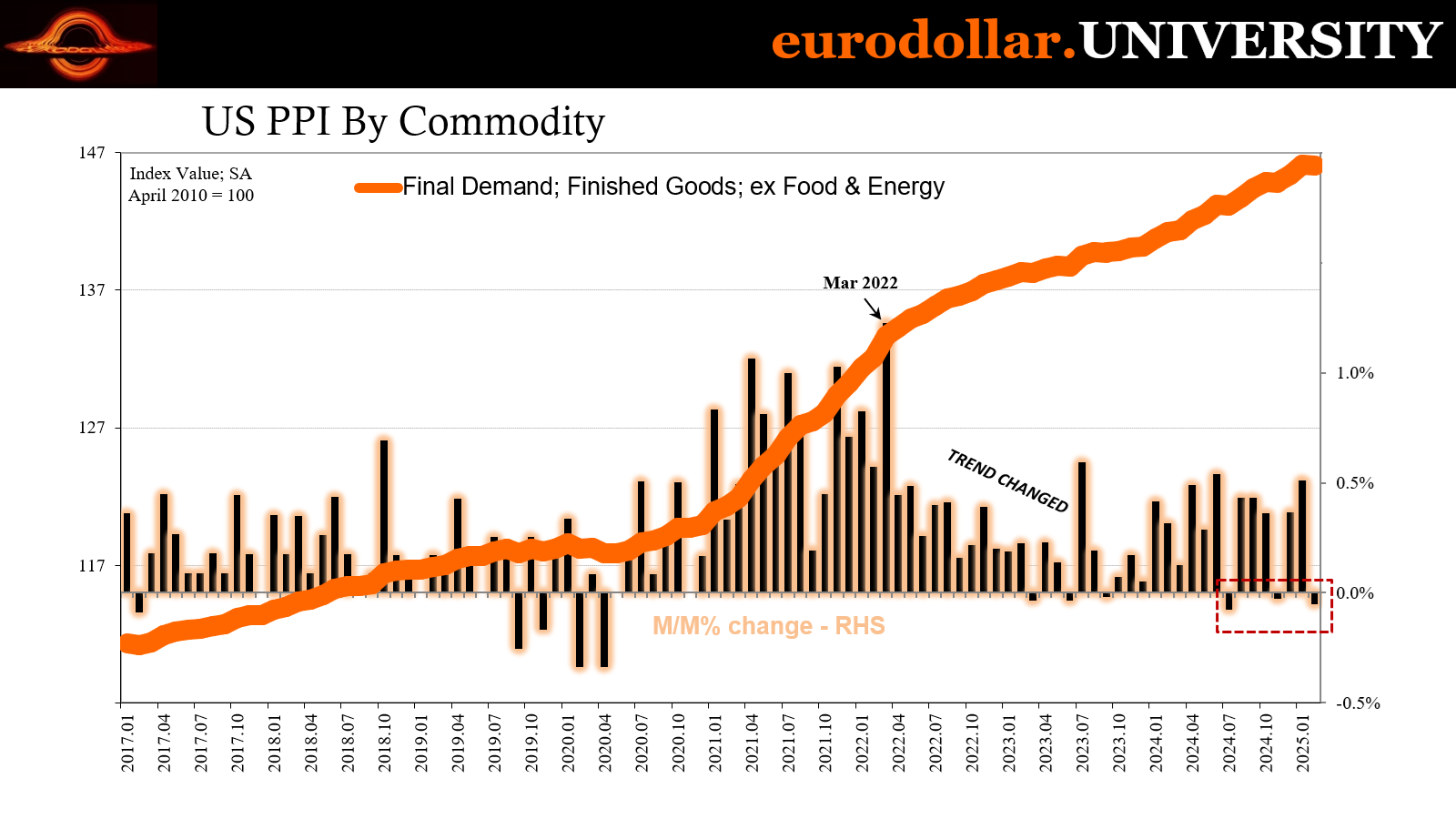

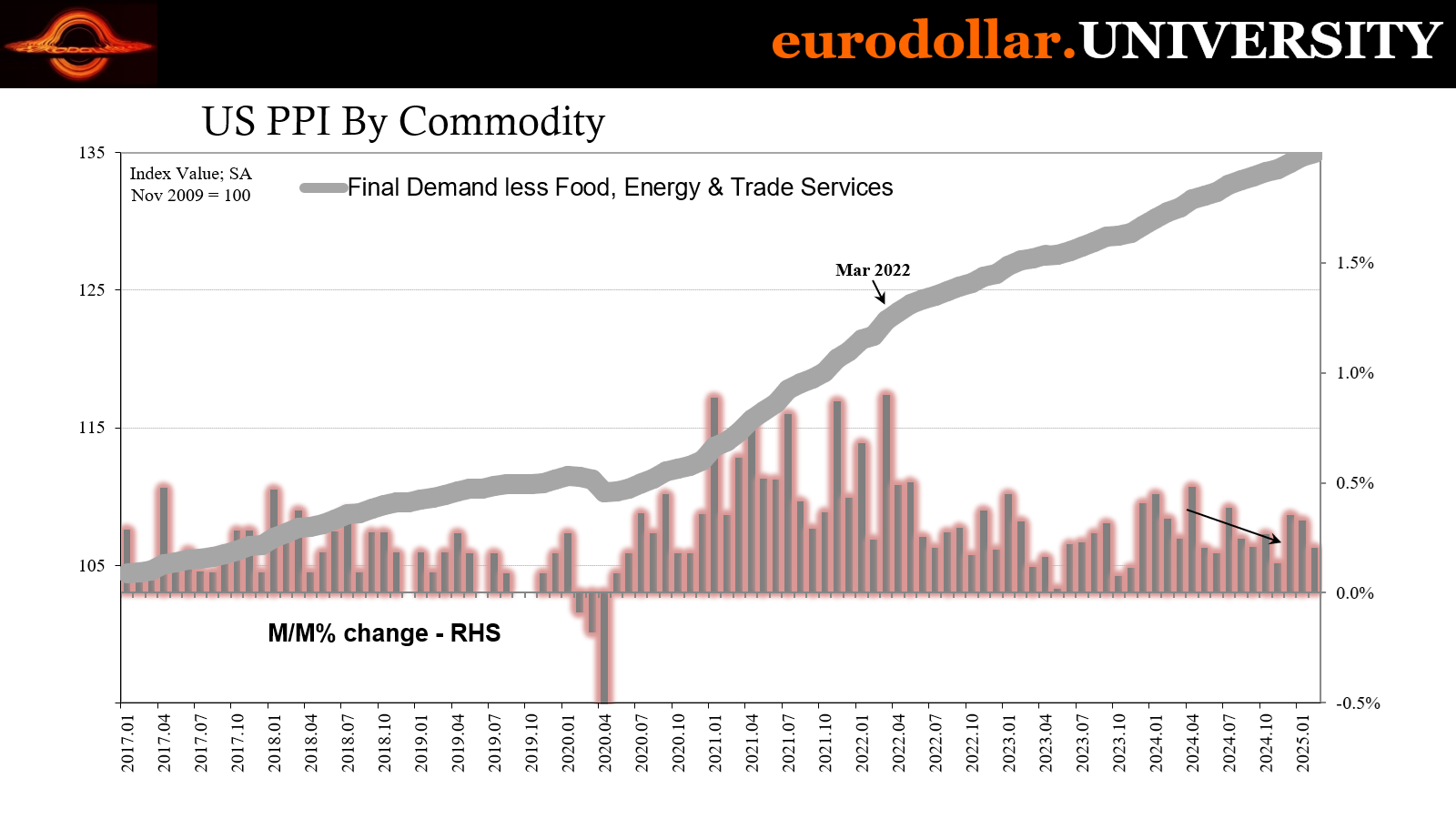

In February 2025, the Producer Price Index (PPI) for final demand was fractionally lower, following upward revised increases of 0.6% in January and 0.5% in December 2024. On a year-over-year basis, the index rose 3.2%. A 0.3% rise in final demand goods prices offset a 0.2% decline in final demand services. Core PPI, which excludes food, energy, and trade services, increased 0.2% in February and 3.3% over the past 12 months. The increase in goods prices was driven primarily by a 1.7% rise in food costs, particularly a 53.6% jump in chicken egg prices. However, energy prices fell by 1.2%, with gasoline down 4.7%. Meanwhile, final demand services declined by 0.2%, the sharpest drop since July 2024, led by a 1.0% decrease in trade services margins, particularly in machinery and vehicle wholesaling.

Interpretation

The February PPI report largely echoes the recent Consumer Price Index (CPI) data, with price expectations slowing in certain areas. The overall PPI remained flat for the month - the first time it hasn’t increased since 2023. This slight softening was largely driven by a decline in services prices. Core PPI, which excludes volatile components, slowed slightly, reinforcing the broader “disinflationary” trend.

The year-over-year PPI increase of 3.2% marks a deceleration from previous months, with the annual rate cooling for the first time since last summer. This suggests that producer-level price expectations pressures are easing, at least temporarily. However, goods prices have been rising steadily for four months, and with pending tariff adjustments, “inflationary” pressures could resurface before settling down again once those changes are absorbed.

The divergence between goods and services is particularly notable. The 0.3% increase in goods prices - particularly in food - suggests that supply-side constraints and seasonal factors are still at play. The 53.6% surge in chicken egg prices is a major outlier, distorting the overall trend, but other food categories also saw price increases. While the egg-pocalypse is already reversing owing to demand destruction, energy prices also declined, with gasoline falling 4.7%, providing some relief.

On the services side, the 0.2% decline represents a significant shift. Margins in trade services saw a sharp 1.0% drop, indicating that retailers and wholesalers are struggling with pricing power. This aligns with a broader slowdown in consumer demand, as businesses face pressure to lower prices in response to weakening spending and is likely the most important takeaway from the PPI report.

Looking ahead, PPI suggests a cooling in “inflationary” pressures. Rising goods prices, especially if tariff adjustments come into play, could push price expectations back up temporarily. However, if services price expectations continue to slow and trade services margins remain compressed, it could reinforce a broader “disinflationary” trend. The Federal Reserve will likely take this mixed picture into account when assessing future policy moves.