A MUCH BIGGER CHALLENGE THIS TIME

EDU DDA Nov. 6, 2024

Summary: With the election quickly settled, attention now naturally turns to the biggest question facing the incoming administration: can Trump pull it off? However anyone might judge the first term, this second one facing even greater challenges. Making the comparisons you can easily see the difference. The new President and his government will definitely have its work cut out for it. Hopefully, Trump will look back on 2016 for the one thing that could really help this time around facing an entirely different cyclical environment.

Interest rates jumped again today as the “Trump” trade continued to grip parts of many markets. Some see this as a positive, nearly euphoric over what they reckon will be a radical departure from the economic circumstances of the past few years facing a vastly different fiscal approach (tax cuts and tariffs). Others look on those same proposals and foresee only deficits and recklessness, the cry of “too many Treasuries” about to be revived for repeated abuse.

However one wishes to view the partisan politics of the outcome, it is now the outcome regardless. From my own detached view as a macro and money observer, the partisanship itself bears nothing on the analysis. I’ve been on the record for many, many years saying it really doesn’t matter which president from whatever party.

They’ve all come up way short, as the evidence shows only too well. In point of fact, my greatest complaint about Mr. Trump’s first term is that he abandoned the one position that could have legitimately made all the difference. During his 2016 campaign against Ms. Clinton, Trump repeatedly referred to the unemployment rate as “fake” rankling all the right Economists and central bankers.

This was made controversial for the primary reason of how poorly saying the truth out loud reflected on all the major initiatives undertaken by those Economists and central bankers up to then, from the repeated failed QEs to the ineffectiveness of ZIRP (LOW RATES ARE NOT STIMULUS) not to mention the complete waste that was the ARRA.

All of those had been the reason why Trump was so successful in his line of attack in the first place.

Participation goes right to the heart of the economic question and how it all relates back to the Big Picture (which both Keynes and Bernanke, the scholar, had long ago identified). Yet, upon taking office President Trump abandoned his fight and embraced the U-3 as his own.

It was entirely understandable, after all, though regrettable anyway; every last politician who has ever politicked would have done the same as the flawed U-3 kept going lower and lower. The BLS creation was even used as “evidence” Trump’s economic policies were working very well (I know this from personal experience visiting the White House complex in 2018 to meet with a top administration Economist only to find him offputtingly cheerful about how well the economy was doing).

Past is past, whatever anyone thinks of the next President or his last stint in office, as in 2016 the challenge he faces is enormous. The question we need to ask is, can he pull it off?

Despite some superficial similarities, the task this time around is an order of magnitude more difficult. While it looks like the bond market is repeating its behavior from the last time around, raising growth and inflation expectations upon the election mandate, that wasn’t necessarily a full-blown embrace of Trump, either. Nor was it in ‘16.

After all, like a lot of other indications, bond yields were already rising for months before November 2016, having bottomed out on Euro$ #3 back in July of that year. Quite a few other key indications had turned around prior to the final stage of that presidential campaign and contest.

Copper-to-gold, for one, had been steadily driving into the ugly depths, reaching 0.0097% by early July, too. The ratio would equal that low a couple times, once in August 2016 then again in September before more thoroughly rebounding. It was already on the way up when the election results provided another spark and leg, surging through November and after.

Like bonds, the election result was a catalyst which combined several short run “tailwinds” already underway. One was the massive China “stimulus” which had been launched earlier in that year, several months prior (the biggest source for strength in copper and a whole lot more beside). Since so much of it consisted of actual spending (bubbly waste) in the real economy, the spillovers globally were substantial in that initial phase.

The bulk of it was delivered during the summertime.

This is the primary challenge Trump 47 faces compared to Trump 45. The economic cycle is different despite superficial similarities like recent Treasury bond trading. It was entering an upswing at the middle of 2016 and while it wouldn’t ever make past the reflation phase, that reflation was the reason for the bond selloff and rising copper-to-gold as much as anything.

When making these comparisons, what emerges is a clear picture of the categorically different difficulties this time around. Even China is vastly changed, including its intended “stimulus.” Unlike eight years ago, Beijing’s “bazooka” is focused instead on bailing out the past bubble mistakes which had been greatly amplified by that last round of Keynes rather than redoing them all over again.

From the get-go, China remains a headwind this time around.

Closer to home, the US economy is in worse shape despite the claims that it is and has been booming, quite strong and resilient – that much hasn’t really changed, either. Once again, Mr. Trump owes his latest electoral success as much to this disparity between the what the professional class says about the economic situation and how regular people see it (the economy has been the Number One issue for voters from the outset). The term “vibecession” perfectly encapsulates the disdain and the anger (from both sides, ironically).

But while the secular background (the economy sucked then and still does now) behind both periods is similar on those terms, the cyclical one this time around is not. As I wrote just above, the US and global economy was moving into a reflationary phase by the last months of 2016. Looking at the evidence, you can clearly see that here in 2024 not only does it remain on the downswing, that downturn appears to be worsening more of late.

Summer 2016 produced meaningful progress and improvement in key measures while Summer 2024 ended up with the opposite.

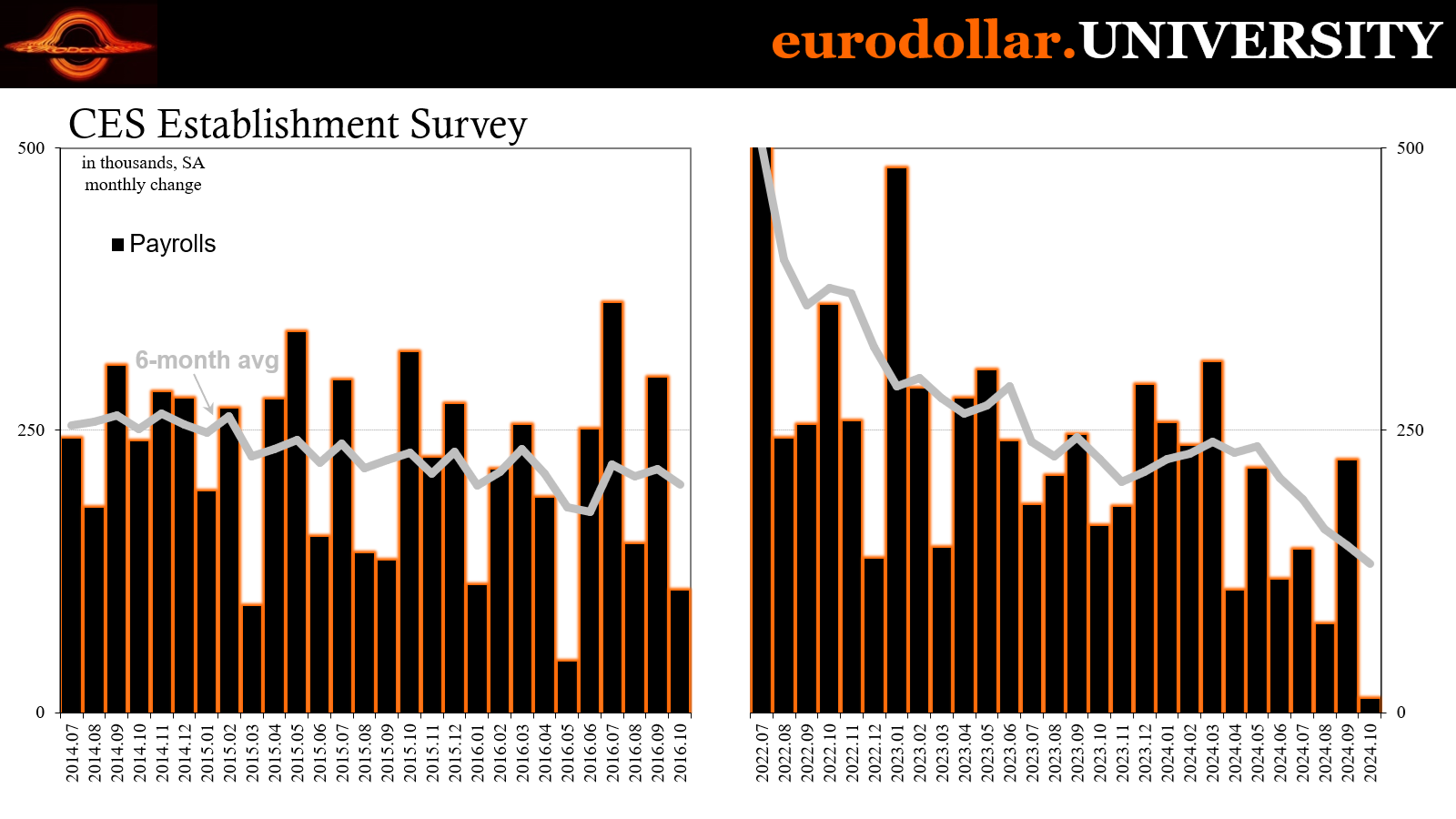

Let’s start with the labor market and the main payroll numbers (CES Establishment Survey). As you can see, from 2014 into 2015 then 2016, payroll growth had slowed down though only modestly (caveat: I’m using the current benchmark estimates rather than contemporary accounts). For example, in February 2015 the 6-month average change was +262,000 (following what had been described as the “best jobs market in decades”). By October 2016, the month prior to the election, that was down significantly enough though only to +202,000.

Contrast that with how this past summer has gone in payrolls. The rate of change had slowed to 205,000 (average) by last November then picked up earlier this year not unlike in early 2016 when the labor market (by current accounts) seemed to steady. However, unlike eight years ago employment stumbled badly after March (a month that comes up seemingly everywhere because of how widely corroborated this inflection is).

The current 6-month Establishment Survey average has dropped to 132,000 but more importantly the trend is obvious and obviously very different from 2016. The economy is going in the wrong direction here.

That’s also the verdict from the Household Survey. The CPS estimates show that employment shut off toward the end of last year and continues to – at best – flatline throughout this year up to the present. There is no sign of a pickup anywhere as the internals of the labor data are showing further deterioration, whether specifically other parts of CPS or related sources such as JOLTS.

Look at the difference in trend for the unemployment rate. The current U-3 is substantially less than it had been back in 2016, which anyone in the media or working for the Fed would say is an improvement then vs. now. Setting aside the even lower participation, the rate like actual unemployment is moving in the wrong direction. Again, the key difference is really cyclical.

Same view from the perspective of incomes. Nominal DPI (6-month rate of change) had slowed way down to nearly 1% last time though was already re-accelerating by the time election took place. This year, nominal incomes which had been growing at faster rates are only just now starting to trend downward.

The same goes for real incomes. In fact, Real Personal Income excluding Transfer Receipts had turned slightly negative on a 6-month basis by June 2016 – one recession signal – but was moving back higher heading into the fall. And all of that against a backdrop of sharply lower overall “inflation” rates.

In 2024, real incomes are only just now slowing down through the middle of the year right up to September (the latest estimates), consistent again with the labor data.

There were also several critical differences in market behavior and positions. Energy, for example, had turned around following the prior years’ (2014-15) dramatic crash. Oil and gasoline would bottom out in February 2016, stabilize then go higher heading toward the election buoyed by China “stimulus” while also increasingly steadied by the general reflation trend spreading around the rest of the world.

This time around, oil and gasoline are much higher being artificially held aloft by supply restrictions covering for weak and weakening demand. So, not only are energy prices relatively more painful right now, the only reason those might get better is because of what really is the early stage of this cyclical downswing. As I talked about on yesterday’s YT, lost amidst the election attention, the IEA just said diesel demand is likely to contract and leave the energy marketplace with an overhang of supply.

The last time that had happened outside of 2020 was, yes, 2016. But that was in the front part of the year not the back.

Finally, back to interest rates. As noted above, the 10s and 2s were moving higher from early July 2016 on improved cyclical (not long run) prospects, the initial selloff for what would become Reflation #3 (or globally synchronized growth). This was why the Fed was at the time slowly raising its benchmarks, shown by the track of the 3-month bill yield.

Low rates that then start to rise isn’t “restriction” in policy or market activity, those are positive signs (reflation). In 2024, we’re getting the opposite again here in position as well as direction. Yields are comparatively higher but now moving generally lower (including the latest gyration in LT yields), not good signs. The 3m rate is reflecting growing expectations for further and sustained rate cuts from the Fed which typically accompany a cyclical downturn.

There are many more datapoints along the same lines, too many to include here. The majority of them show that the circumstances in 2024 are decidedly more challenging when compared to 2016. The economy President Trump 45 faced wasn’t fantastic by any stretch, though it was at least favorable. Trump 47 has even bigger structural matters to overcome (incomes!!!) plus, as if that wasn’t bad enough, he also has the global economy still on the downside of the supply shock. From the labor data and perspective, that downswing is really starting to look like an accelerating slide, too.

Most of all, the government’s ability to solve all these or any one of the deficiencies is exceptionally limited (and I don’t just mean by the massive increased debt in between). We have been conditioned to look to central authority expecting them to surmount economic challenges. This is what was initially so positive and optimistic about Trump’s focus on the unemployment rate in 2016; implicit in his attack on it was recognizing how all the past “stimulus” didn’t work, government action hadn’t produced anything more than a false recovery (some would say that was the entire point, but I digress).

Altogether, when analyzing the potential for a Trump Administration II it has to start with the understanding there is a much larger hole to climb out of this time. The biggest obstacle is likely to be the different cyclical direction.