COME ON NAIRU

EDU DDA Jan. 10, 2025

Summary: Why can’t Jay Powell and the FOMC seem to get a fix on “inflation.” Their entire recent hawkish stance is built on a single theory with an atrocious track record - even in Powell’s own experience. Today’s payroll report came in “hot”, yet, in truth, the labor market is under significant stress which is ironically illuminated by the very way in which the Fed considers it potentially inflationary. This whole discussion explains exactly why central bankers are doing what they’re doing, unable to make a determination on “inflation” pressures. Or labor strength. What’s the right comparison to make?

December’s payroll estimate was another head-scratching one. It was way above every expectation for reasons that aren’t clear. Maybe there is Trump bump underway, yet it isn’t showing up anywhere else. One thing for sure, the Fed is likely to take it very seriously especially in the context of what the CPI has been up to lately.

To understand why, and why it’s bonkers, you have to consider and appreciate something called NAIRU. For a rundown of what the BLS published today, including the HH Survey and unemployment results, it’s all in our Daily Briefing.

Economists have theorized that there is a level of unemployment which defines the boundary between full employment and inflation. The concept of the non-accelerated inflation rate of unemployment (NAIRU) grew out of the Keynesian pursuit of the Phillips Curve, and their hoping for an exploitable one.

Owing largely to Economists Paul Samuelson and Roger Solow, the pair had proposed governments could actively raise the level of employment by engaging in a trade-off with inflation. AW Phillips had observed in the UK consumer price rates tended to behave according to pay levels. He surmised the degree of competition for workers must’ve explained the relationship as the way through which consumer prices resulted.

It appears to make sense, on the surface. Samuelson and Solow took it a step further, hoping to take advantage of this. Their original 1960 paper published in American Economic Review contained the following now-infamous passage:

In order to achieve the nonperfectionist’s goal of high enough output to give us no more than 3 percent unemployment, the price index might have to rise by as much as 4 to 5 percent per year. That much price rise would seem to be the necessary cost of high employment and production in the years immediately ahead.

It sure sounds like the Economists are arguing for governments to intervene directly in the economy so as to achieve as high a maximum for employment as possible. If that meant tolerating slightly higher inflation, so be it.

Aside: the idea that governments are the marginal force in the real economy is one the big theoretical as well as real world problems in everything. Maybe governments don’t matter all that much, the private economy does. Looking at you China.

In fact, Solow recounted later in 1978 a late fifties conversation he had with Samuelson whereby both of them agreed that’s exactly what they would pursue upon seeing for the first time what Phillips had published:

I remember that Paul Samuelson asked me when we were looking at those diagrams for the first time, ‘Does that look like a reversible relation to you?’ What he meant was ‘Do you really think the economy can move back and forth along a curve like that?’ And I answered ‘Yeah, I’m inclined to believe it’ and Paul said ‘Me too.’

The theory was almost immediately criticized by the likes of Milton Friedman, Robert Lucas, and even Edmund Phelps, the heavyweight non-Keynesians of the time. In fact, for a long time (as I understand it) the joke was Samuelson and Solow’s poor theory was the basis for more Nobel Prizes than any other in history – just not for them.

What Friedman and Lucas instead proposed was that below a certain threshold unemployment wouldn’t create some stable level of inflation, on the contrary it would lead to accelerating price increases. They and others reasoned that there was always some minimum degree of unemployment, a structural level which meant you couldn’t ever get any lower without triggering wage pressures at minimum.

Should the level of unemployment find itself below it then inflation couldn’t remain constant, it would continuously accelerate, therefore the name non-accelerated inflation rate of unemployment. This is the point where slack in the economy remains sufficient it won’t spark that kind of inflationary spiral. It’s where every central banker is targeting.

NAIRU followed, first, some flirtation with NRU, or a generally natural rate of unemployment which differs from the former in ways that aren’t important here. Economists even today generally stick to one of the other as a guide for that elusive inflation/employment trade-off.

But one of the primary innovations coming out of the 1970’s, by cascade of global monetary mistakes, was that there may be no single Phillips Curve equilibrium. That was Milton Friedman’s whole point, as he came up with a more dynamic “natural” employment rate (to be clear, Friedman used the word “natural” to simply mean non-policy).

Structural factors change what became known as the “inflation barrier”, the actual cross where if the unemployment rate falls below inflation starts to rise precipitously. Almost all of the post-Great Inflation academic world has been dedicated to using theories about the 1930’s in order to make sure whichever economy does not run afoul of this natural obstruction.

NAIRU has been refined over the decades to better reflect the possibilities for structural economic shifts, both positive and negative. The more modern version, TV-NAIRU (for Time-Varying), introduced the concept of the “Triangle Model” incorporating both supply and demand as well as what Robert Gordon called in his 1996 paper “inertia.”

The inflation process in the United States is one of the most important macroeconomic phenomena in the world, but it is also one of the best understood. In contrast to the wild gyrations of inflation in many other countries, the U. S. inflation process is dominated by inertia. Inflation changes little from year to year, and any deviation of the actual unemployment rate from the NAIRU has extremely small consequences in the short run.

In other words, you might be forgiven if the unemployment rate drops below NAIRU for a short time. Should it remain there, all bets are off; or should be. You might already see where I’m going with this.

There is no way to observe the point at which the magical Phillips trade-off occurs, whichever flavor of NAIRU or NRU you might prefer. This never stops Economists from trying to find and define it. We do have estimates for the former that are produced by the Congressional Budget Office (CBO) and made available for public inspection and analysis (unlike the Fed’s models kept in secret; though there likely isn’t any meaningful difference in either theory or results between the Fed and CBO).

In fact, the CBO uses NAIRU when piecing together its long run estimates on economic potential.

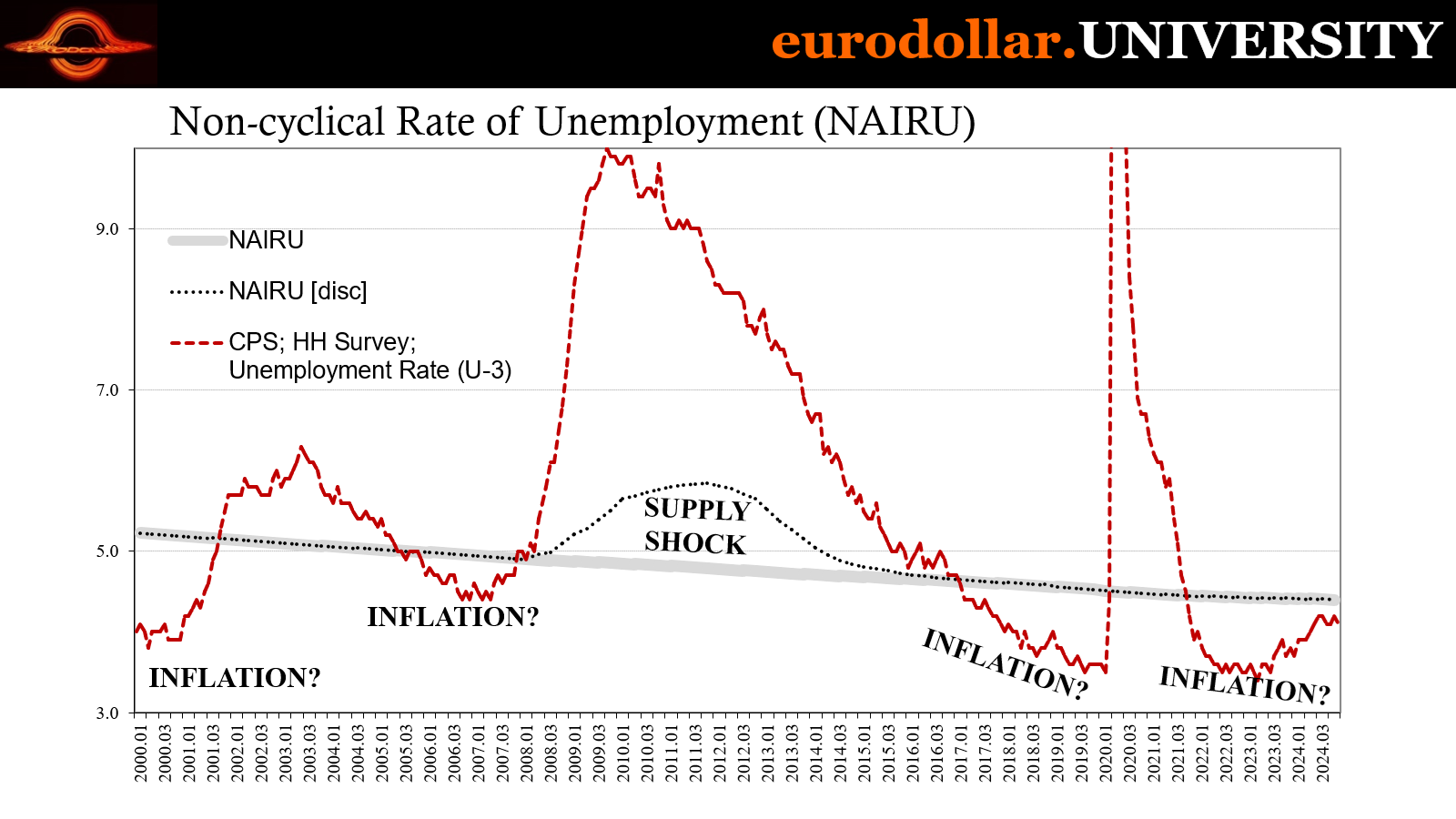

A quick scan of those estimates plotted against the actual unemployment rate is revealing. First, it pretty much tells you exactly when the Federal Reserve will be “hawkish”, itching to raise rates so as not to run afoul of accelerating Phillips.

In the late nineties and 2000, for example, Alan Greenspan nervously began hiking the fed funds target since the unemployment rate had gone well under modeled NAIRU. Because it was so far underneath, Gordon’s “inertia” risked coming to life, a sufficient push to really get the price acceleration going.

Never did, though.

Similar developments in the middle 2000s. By the middle of 2005, the U-3 was once again “too low” yet no inflation. Instead, not long later, deflation. In between, though, a bout of oil-soaked consumer prices which had officials unsure of where to turn (more on this below).

Why did Janet Yellen start becoming “hawkish” in 2017 after being ultra-careful about rate hikes in 2015 and 2016? Again, the official unemployment rate had dropped under our friend NAIRU. The further below it tracked, the more worried about “inflation” the FOMC became. This is exactly why in the early months of his tenure, Jay Powell seemed like he was in a rush to get on top of the “labor shortage.”

In truth, the whole idea of the labor shortage was itself NAIRU.

Like before, though, lots of talk, tons of expectations, loads of speculation, zero inflation.

Furthermore, we’re using a newer version which had erased a very revealing not to mention relevant prior calculation. Notice (hard not to) the sudden hump in the old one starting during 2008, rising still in 2009 (the worst of the not-recession) through all of 2010 all the way to the end of 2011. That was the model’s way to try to account for why consumer prices (not inflation) had soared, first in 2008 while the meltdown was in progress spiking unemployment.

Then, in the aftermath, consumer prices accelerated again even though the unemployment rate was still enormously, painfully high. How could “inflation” accelerate when that was the case in the labor market? By the theory, only if the threshold for acceleration was so much higher than before! Yes, they reverse engineer NAIRU to make the model fit the data.

You can see the CBO’s and presumably other Economists’ solution to the problem: they simply ignored it, erasing the entire episode out of the history.

Where did that burst of “inflation” come from, and why was it transitory? In reality, prices had soared first in 2008 because of a global oil supply shock. Then in the aftermath of the Great not-Recession, demand partially recovered faster than general supply could (companies preoccupied with liquidity and cash flow rather than recovery risk-taking). Yep, both were supply shocks of varying degrees and reach and it should sound very familiar.

No rate hikes were required to quell either one.

The idea of a “hot” labor market creating headaches for Jay Powell here in 2025 stands on less than nothing. Not only do we have those previous supply shocks which were proven to have been completely unrelated to the labor market or any “tightness” which didn’t exist, moreover the unemployment rate has remained under everyone’s NAIRU since the end of 2021. Three years is obviously more than enough time to overcome “inertia”, too.

Yet, you’ll also have noticed, “inflation” is not accelerating. The CPI might be in short run in small bursts, those aren’t near what we’re talking about here.

Officials and the media may make some conjecture about “stickiness”, whatever is happening with consumer prices they are decelerating even though the unemployment rate, even after rising the last year and a half, remains “too low” by the judgement of NAIRU. This is also why the Fed keeps estimating the unemployment rate will plateau right around 4.2 to 4.4%, because their models have to be assuming that’s where the threshold is, same as the CBO.

Therefore, the entire purpose of their current interest rate policy is to push the unemployment rate up above NAIRU. Officials at the Fed thought they had a few months ago, then the CPI accelerated again (as it has repeatedly for reasons having nothing do with the labor market) forcing their current reconsideration.

And it is ultimately meaningless. The 2018-19 experience is relevant here. Consumer prices never accelerated all that much let alone in a way that indicated some accelerating phenomenon. Despite the ubiquitous “labor shortage” references, wage rates didn’t accelerate, either – this is the point of contention, not inflation.

Wages right now should be soaring given NAIRU.

A truly “tight” labor market wouldn’t necessarily create legit inflation, only money can. It would, however, create the competition for workers therefore higher and accelerating wages. No matter how you feel on the Phillips Curve tradeoff, the point is the economy and labor market never even got the wage part anyway.

The reason was the labor market was never “tight” at any point no matter what the unemployment rate might have indicated. There was more “slack” in it than suggested by the official rate which discounted and ignored labor force dropouts – a lesson Economists should have learned from the entire 2010s. But in econometrics the models are always treated as “more real” than reality.

What that means is the labor market is far weaker than appreciated at either the Fed or in public. Slack is actually enormous and rising, with NAIRU ironically helping confirm it.

We need only to plot some more baselines, in this case just using those from the 2010s is more than sufficient. The payroll estimates for 2024 are so far behind theirs there is no chance of a “tight labor” market and the only reason why wage rates had gone up so far in 2021-22 was because of how the pandemic/lockdown supply shock had created a mismatch between, again, demand and supply, this time of workers.

Once those two came into better balance – not because of rate hikes – wage rates slowed. By then, the labor market itself was already in serious distress, the level of which was clouded by this mainstream obsession with NAIRU. The job market had to be “hot” since the unemployment rate was below the threshold, therefore everyone ignored all the evidence showing why it wasn’t.

NAIRU said they should be doing the exact opposite.

Jay Powell and the FOMC are freaking out over every single short run acceleration in the CPI because with the unemployment rate still below NAIRU they can’t be sure the CPI speeding up in these short run bursts isn’t that dreaded acceleration in underlying inflation pressures. Chasing ghosts.

The actual state of the labor market is very different, as even today’s ridiculous report shows. The proper way to characterize the December estimate isn’t that it gained 257,000 from November, rather it failed to narrow the gap to the baseline by more than a rounding error. The wildly overstated CES payrolls have been falling further and further behind the minimum level of jobs (the 2010s baseline is the absolute minimum) rather than being somewhere above an inflation point that doesn’t exist.

In other words, using these heavily flawed numbers and theories, the Fed thereby the public are pulled into believing a weak and troubling labor market is somehow strong and resilient if not borderline inflationary! Night and day different from reality.

When you look at the stats outside this absurd framework, such as when using nothing more than calendar year changes, that trouble is much easier to appreciate. Considering first the gap to the baseline then the clear deceleration in job recovery (not growth), a recovery that completely stopped in the HH Survey, it’s therefore very clear where the risks to the entire world lie.

Not only does NAIRU explain what the Fed is doing and why, it also helpfully shows why it’s all wrong.