POWELL SAYS IT’S OK HE WAS WRONG ABOUT EVERYTHING

EDU DDA Aug. 23, 2024

Summary: Jay Powell at Jackson Hole, Wyoming, today turned out a speech unlike any other he has given before. That said, it wasn't actually something new either from a Fed chair or one in that same setting. Like Ben Bernanke a long time before, Powell started out by admitting the US is in serious trouble before then trying to sell the world he has a way to fix this. Sadly, it's also the same one Bernanke tried to sell.

I wrote just yesterday, “With recession increasingly staring down the world in every way, central banks are flipping from rate hikes (which didn’t seem to have much impact on consumer prices) to now rate cuts and the celebration over them has only been turned up to eleven. The Fed, the Swedes, the ECB, there’ll be cutting all around the world and soon to be a lot of it. “ Then Jay Powell today just confirmed it.

He did see with what was a true performance. Just reading the prepared text you could tell this one was different, everything from the language to its setup and outline. I don’t know if he changed speechwriters or plucked the best one from the Fed’s bullpen and gave them the specific assignment, the difference showed.

Same for his demeanor. Having read the address, I watched a replay to see if the delivery matched the words. It was still Powell, though you could clearly see the gravity that pulled through the text. This was as big as they came.

Typically, the Fed Chair is explaining; the dirty legacy of Ben Bernanke’s push toward unnecessary transparency. What the Fed does, how it is supposed to operate. Occasionally some background on the theories (however useless) guiding their, and therefore your, expectations.

This time Mr. Powell was clearly selling.

Everything else was the same.

He simply has no other choice but to sell having boxed himself in for too long. From that alone you can tell they clearly were confused about consumer prices which left policymakers flat-footed as the economy turned underneath them. The unemployment rate didn’t start rising last month, it’s been on the move for over a year with momentum swinging more and more decisively from way back around March.

Everyone downplayed the transition because Powell told them it was no big deal.

The Big Deal today was the entire Federal Reserve now admits it actually is a very big problem. He came right out and said the unemployment rate cannot go any farther and the Fed would unleash its full might to make sure it doesn’t. Just from that statement alone, you can understand why the emphasis on selling.

His performance, therefore, was directed to reassure the public and the markets (stocks) that though the entire economic message has changed, officials are on top of it. Gone is the “strong and resilient” labor market, replaced seemingly out of nowhere (for those who haven’t been paying closer attention to anything but the mainstream financial media) by a rate-cutting policy now necessary, according to Powell, because the entire labor market is already right at the edge of the precipice.

In order to really sell the message, Jay spent the majority of his time today taking credit for disinflation. Powell went from publicly not being confident on consumer prices to Hell Yeah We Did This! almost overnight. He quite painstakingly reviewed the entire supply shock era and with no fedspeak in this one, not even the usual bland brand practiced by Powell. The institution, he claimed, methodically and patiently did the work to see it all the way through.

Quite an accomplishment when just last month they weren’t even sure what “inflation” was doing.

No matter, they slay the beast so you can be confident in them as they now turn their attention 100% to the next dragon just last week Powell claimed was all a big nothing. We needn’t worry about unemployment because if they could the conquer the mighty consumer price spike the world just experienced then officials can certainly limit any damage in jobs.

They can’t so thoroughly pivot like this without selling the idea the pivot is actually a good thing.

Outside Economists (below), the media, and the stock market, few are buying it.

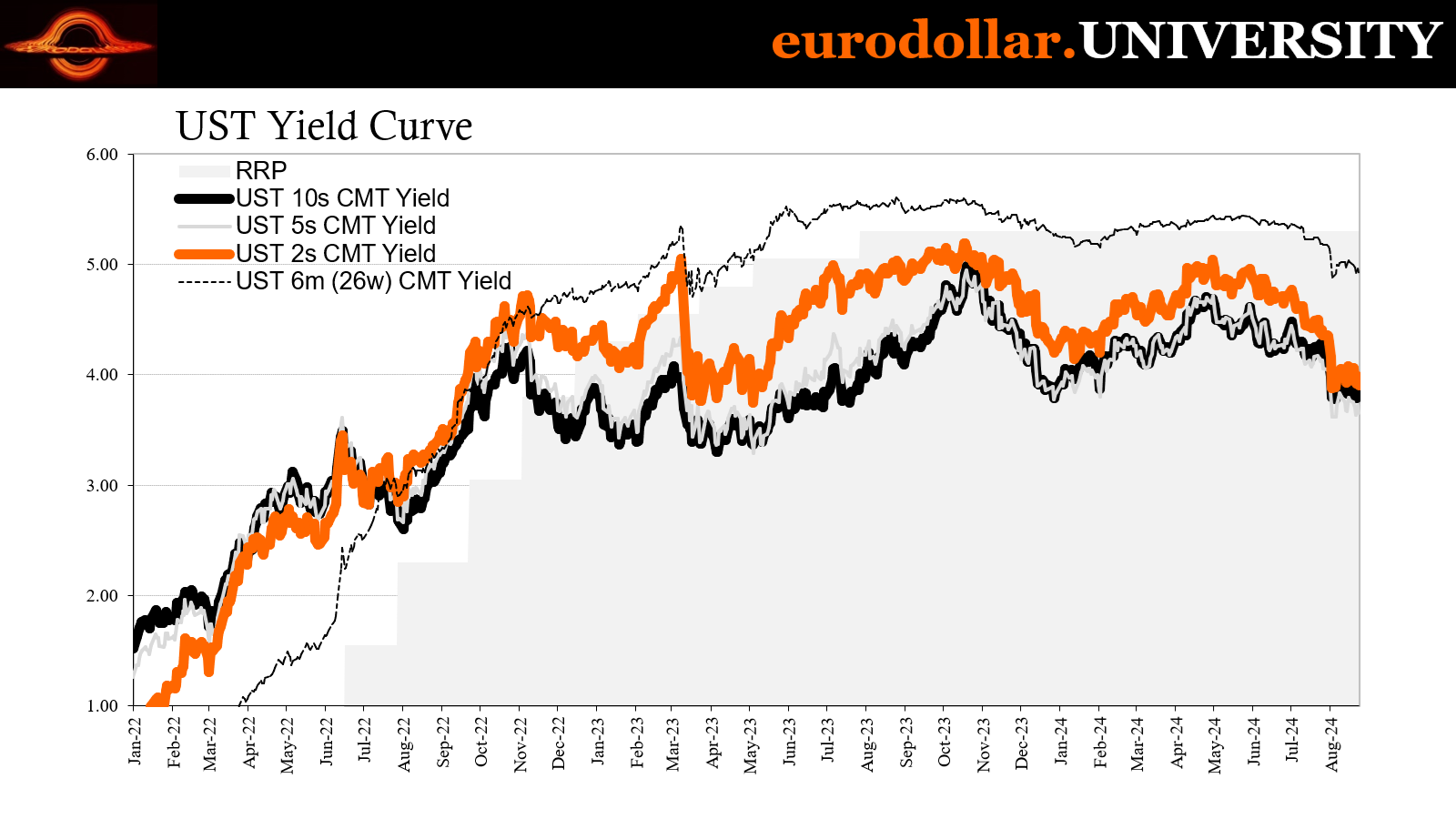

Implicit in this whole narrative is real economic weakness that wasn’t supposed to be there, serious enough that Powell also felt the need to bring up just how much “room” the Fed has to cut rates. Since the fed funds target is 5.25% (lower bound), that’s a lot of potential rate cuts – which the markets have already priced in. And as I wrote in yesterday’s DDA, it’s the announcement what’s supposed to really matter which is why central bankers don’t mind even fake rate cuts.

That’s why Treasury yields, for example, continue to move so much lower despite it being September (in market terms). Most understand that if there’s a recession then the Fed won’t be able to do much other than respond to rising unemployment with continuously-lower policy levels. And Powell just admitted even the Fed sees a high degree of recession risk.

And this assumes it isn’t already too late, a factor also implicit to a degree in the sales job. If it is too late, then be confident anyway because they reacted too late to “inflation” and that worked out just fine!

There wasn’t exactly euphoria in the stock market, though there was far more taken positively than reality warrants. The S&P 500 is a mere few dozen points off is record high as if nothing happened three weeks ago and the Fed’s pivot is exactly as Mr. Powell describes; the Big Bazooka wielded skillfully by the best and brightest in the face of the direst potential circumstances.

All of this should sound familiar, however. Though Powell tried his best to make it sound different, it isn’t right down to the setting and the overall way in which the argument, such that he made one, was laid out.

I don’t meant the most-cited example of October 2007, the record high for the 500 and DJIA mere weeks before the Great not-Recession began on the perceived strength of, yes, a fifty-bps September rate cut. No, Jackson Hole 2010.

Starting in late August of that year, share prices absolutely soared due to then-Chairman (the title was gendered back then) Ben Bernanke’s weirdly similar performance in Wyoming. The circumstances were slightly different, though no less severe. The US and global economy were not, in fact, recovering even after the contraction had ended a year before due mainly to the fact the monetary system continued to malfunction and cause widespread further economic and financial damage.

Clear to anyone watching, Bernanke basically confirmed another QE was coming just as Powell today says look out for those awesome rate cuts. Yet, there was absolutely no reason to have cheered what came to be known as QE2. To begin with, it was by any legitimate count the third QE already at that early date. The Fed had initially launched the program in December 2008 then barely three months later realized it wasn’t working quickly more than doubling the size.

Some claim this as the reason why the crisis ended and thus a case to be optimistic about more of it. The marketplace outside of stocks knew better (FAS 157 deserves the credit) especially since all the same deflationary symptoms were right back in place as early as November 2009! If QE had worked, first or second, then 2010 would have turned out very differently.

There would never have been a need for the third.

Because it was not different, following a May flash crash on Wall Street that “coincidentally” timed to major upset in global repo, Bernanke’s Fed watched the economy falter knowing they had to do something dramatic to keep hope (all the “central bank” really has) alive. His choice was not unlike Mr. Powell’s, to sell the world on an ability the Fed very clearly did not possess.

Like Powell, Bernanke began with what really was a sober, honest assessment:

Notwithstanding some important steps forward, however, as we return once again to Jackson Hole I think we would all agree that, for much of the world, the task of economic recovery and repair remains far from complete. In many countries, including the United States and most other advanced industrial nations, growth during the past year has been too slow and joblessness remains too high.

The only real difference is that unemployment had already exploded the year before and didn’t actually turn around however slowly until earlier in 2010. This actually made Bernanke’s job so much more difficult because he was speaking about the consequences of all those prior policies having failed at their primary task, clearing a credible path toward full recovery.

So, like Powell, Bernanke turned those failures into purported successes; it would have been worse if the Fed hadn’t the courage to act. Programs conducted during the crisis must have been successful and effective because the world didn’t end.

With that, the Chairman then told the audience the Fed still had several powerful tools left in its kit that it could come back to should conditions demand. While Bernanke used that conditional, his implicit wink and nod was immediately understood especially by stocks to mean he was going to use them. And the first one he listed was, of course, more asset purchasing, QE.

The third one.

Although what I have just described is, I believe, the most plausible outcome, macroeconomic projections are inherently uncertain, and the economy remains vulnerable to unexpected developments. The Federal Reserve is already supporting the economic recovery by maintaining an extraordinarily accommodative monetary policy, using multiple tools. Should further action prove necessary, policy options are available to provide additional stimulus

So, very much like Powell, he laid out the challenges in the economy and then sold everyone on…doing more of the same. Give the guy credit for that, it definitely worked on Wall Street and the media therefore the public if nowhere else in terms of actual economy and money.

The S&P 500 went vertical from there, a nearly unbroken 45-degree angle all the way from Bernanke’s speech on August 27 to February 2011 when the damage and setbacks in money and banking were beginning to show up more forcefully again. Plus, no recovery.

Indexes would fall then plunge in the middle of 2011 as Euro$ #2 erupted, and it would take an entire year to regain the same level proving a very harrowing experience after all.

And while the US did not experience a full recession that year or 2012 as Europe would, the consequences were even worse given their long run nature. Euro$ #2 ended any hope of recovery, period. The 2010s became the 2010s in 2011 despite three QEs and “ultra-accommodative” interest rates.

In light of all that, you can see what Bernanke was up to, what he was really trying to buy with his sales pitch – and that was nothing more than time. He needed some more if only because he thought that given enough space the recovery would eventually take off. The Fed’s QE got him that time if nothing else.

This explains why Powell put so much into the shape and delivery of his speech. It had to be all show because its substance is all-too-familiar. And he knew he could at least count on shares to help with the pitch even as everything about it was near enough the same old tired dogma: the same template for the speech; its same setting in Wyoming; what was being offered was the same; even the reason it was.

He could have just copied Bernanke from fourteen years ago.

Back then, Bernanke admitted the recovery wasn’t happening but then tried to sell the world on the Fed being able to fix it with the same stuff. Today, Powell admitted the US is at least on the cusp of recession as he tries his best to sell everyone another one of the same Fed fixes as always.

Gone is “strong and resilient” unceremoniously replaced with, yeah, but we can cut rates a lot. Powell’s updated version:

The time has come for policy to adjust. The direction of travel is clear…We will do everything we can to support a strong labor market as we make further progress toward price stability. With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market. The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions. [emphasis added]

There will be consequences to this pretty obviously flip, call it a pivot if you want. Jay Powell just conceded he was wrong about the labor market and the economy but that it was OK because rate cuts.

Over here in reality, he just walked right into the same market scenario we’ve been seeing from the market since the rally started last October. “Ample room” means lots of rate cuts and all due to rising unemployment. As I’ve been writing and saying forever, rate cuts don’t help except to tell you when it’s gotten serious enough even the central bankers can see it. From Wyoming, behind all the seeming extras, what Chair Powell really did was confirm it’s all happening.